Should Landlords Require Renters Insurance?

The question of whether landlords should require renters insurance comes up constantly in property management. Most landlords focus on protecting their buildings, but they often overlook how tenant coverage protects everyone involved.

At Direct Insurance Services, we’ve seen firsthand how this simple requirement reduces disputes, cuts liability exposure, and gives tenants real financial protection. This guide breaks down why it matters for both sides of the rental agreement.

Why Landlords Must Require Renters Insurance

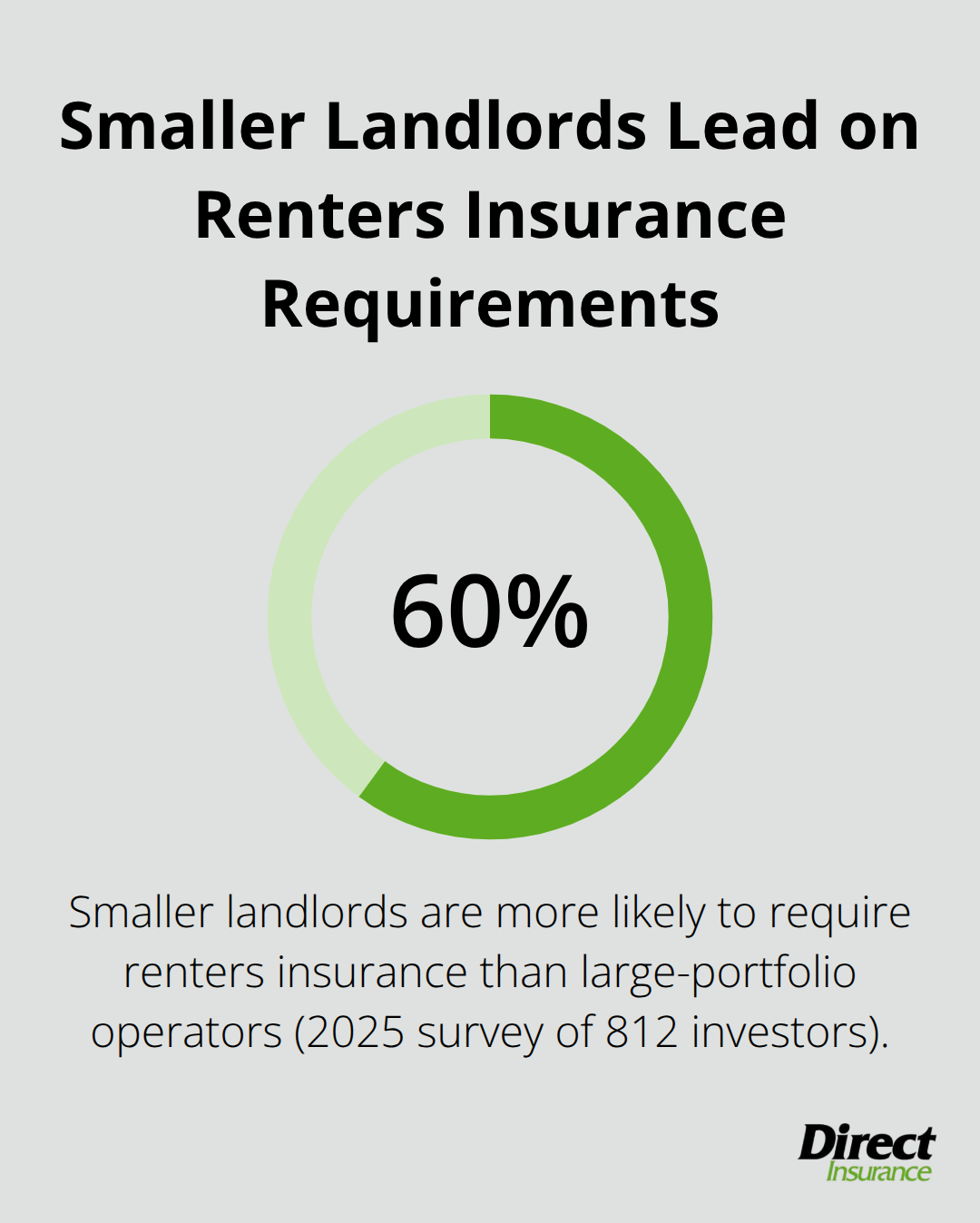

Requiring renters insurance isn’t optional if you want to run a professional rental operation. A 2025 RentRedi and BiggerPockets survey of 812 real estate investors found that smaller landlords with fewer properties are 60% more likely to require renters insurance than those managing large portfolios. This matters because it shows the difference between landlords who protect themselves and those who ignore real financial exposure. When a tenant’s belongings catch fire, get stolen, or sustain water damage, your building insurance covers the structure only.

The tenant’s personal property-furniture, electronics, clothing, artwork-sits completely unprotected without renters insurance. This creates a liability trap. Tenants without coverage often blame landlords for losses that weren’t the landlord’s responsibility, leading to disputes, potential lawsuits, and damaged relationships. Requiring renters insurance from day one eliminates this friction entirely.

The Liability Protection You Actually Need

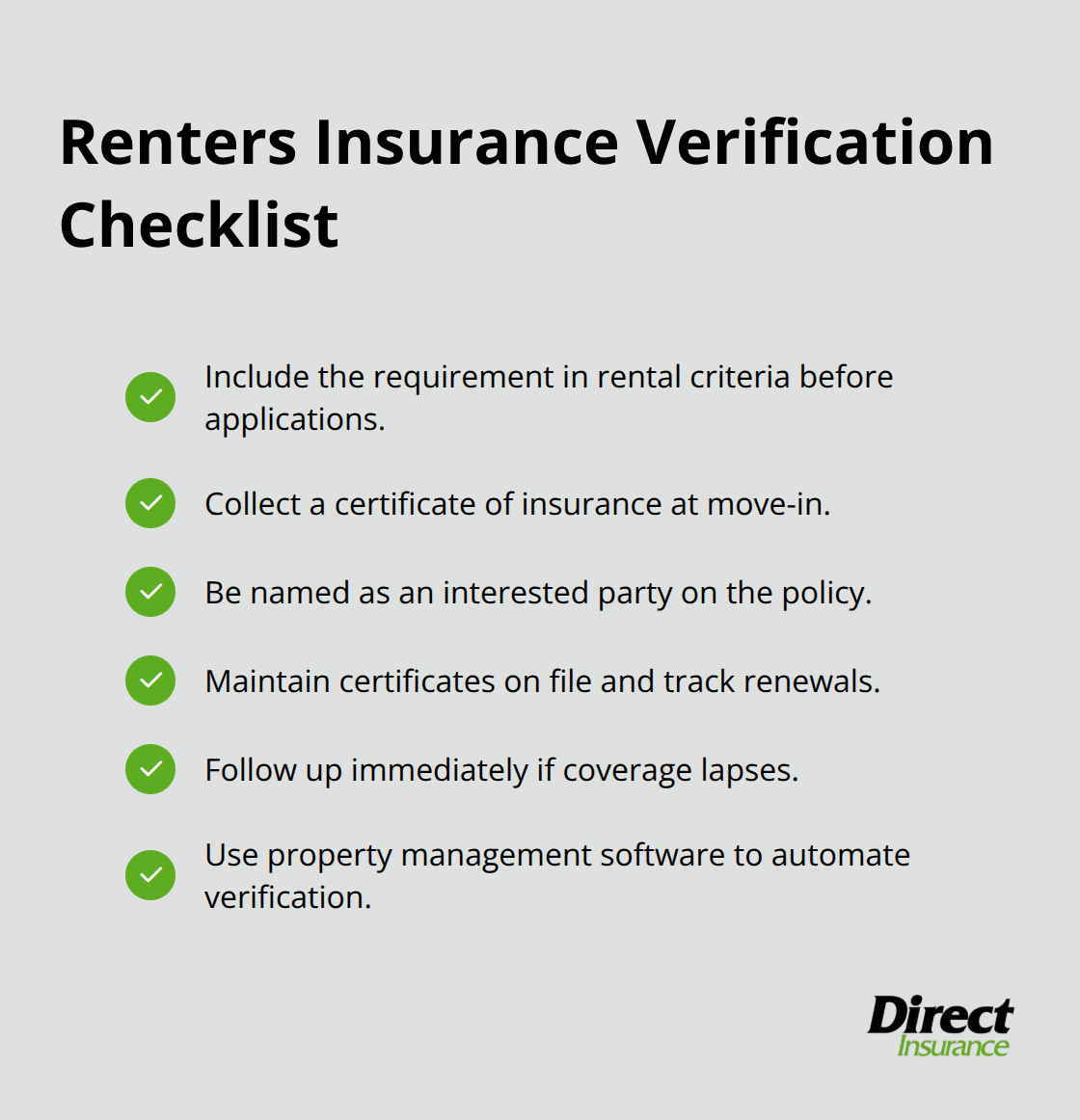

Renters insurance includes personal liability coverage, which protects you if a tenant injures someone or damages someone else’s property while renting from you. Without this coverage, the injured party might pursue claims against your landlord policy, raising your premiums or creating coverage gaps. A tenant with adequate liability coverage handles these claims through their own insurer, keeping your exposure contained. In Virginia, renters insurance costs around $127 per year-roughly $11 monthly-making it affordable enough that price resistance from tenants signals other screening concerns. Additionally, requiring insurance acts as a financial responsibility filter during tenant screening. Applicants who carry coverage demonstrate they take their rental obligations seriously. This simple requirement weeds out applicants who cut corners elsewhere. The verification process matters equally. The same 2025 survey found that few landlords actually verify coverage after requiring it, creating a false sense of security. Request a certificate of insurance at move-in and maintain it on file throughout the tenancy. Most renters policies allow you to be named as an interested party, giving you direct notification if coverage lapses.

Protecting Your Income and Assets

When a covered disaster displaces a tenant, renters insurance includes loss-of-use coverage that pays for temporary housing and living expenses. This prevents you from absorbing relocation costs while the property undergoes repairs. It also keeps tenants from defaulting on rent during extended vacancies caused by fires, floods, or other major damage. A tenant with adequate coverage moves faster, returns faster, and causes fewer complications for your recovery timeline. Beyond individual claims, requiring renters insurance reduces your own landlord insurance costs. Insurers view properties with systematically insured tenants as lower-risk, and this can translate to better rates at renewal. You signal to underwriters that you manage risk professionally, not reactively. For landlords managing multiple properties, implementing a consistent renters insurance requirement and verification workflow through property management software eliminates manual tracking and reduces compliance gaps. The financial return-lower premiums, fewer disputes, faster claims resolution-justifies the small administrative effort required to enforce the requirement consistently.

Making the Requirement Stick

Stating the requirement in your lease means nothing without enforcement. Include renters insurance in your rental criteria before applicants submit applications, so they understand the expectation upfront. This approach prevents last-minute negotiations and sets a professional tone for the entire tenancy. When you collect the certificate of insurance at move-in, you’ve already established that this requirement matters. Consistency across all tenants protects you from discrimination claims and demonstrates fair management practices. If a tenant’s coverage lapses mid-lease, your notification as an interested party alerts you immediately, allowing you to address the gap before problems arise. Property management software can automate much of this tracking, sending renewal reminders and flagging expired policies without manual intervention. The effort you invest in verification pays dividends when a loss occurs and the tenant’s insurer handles the claim instead of your policy absorbing the hit.

Now that you understand why renters insurance protects your bottom line, the next section examines what’s actually happening in the market and how landlord practices are shifting across different regions.

Current Trends in Renters Insurance Requirements

The Reality Gap Between Best Practice and Actual Enforcement

The gap between what landlords should do and what they actually do remains surprisingly wide. According to the 2025 RentRedi and BiggerPockets survey of 812 real estate investors, smaller landlords with fewer properties are significantly more likely to require renters insurance than those managing large portfolios. This creates a paradox: the landlords who need protection most often skip the requirement entirely. Large portfolio operators manage complexity through systems and software, yet they are the ones least likely to enforce renters insurance. Smaller landlords, despite lacking sophisticated property management tools, recognize the value of the requirement and implement it consistently. This suggests that requiring coverage is not a technology problem or a knowledge problem-it is an execution problem. Landlords who treat renters insurance as non-negotiable see fewer disputes and lower claims. Those who treat it as optional or let it slide after initial lease signing expose themselves unnecessarily.

The verification gap makes this worse. Few landlords actually verify that coverage exists after requiring it, creating a false sense of security. A tenant could let their policy lapse mid-lease, and without active verification, the landlord would not know until a loss occurred. Requesting a certificate of insurance at move-in and maintaining it throughout the tenancy transforms the requirement from a paper exercise into genuine risk management.

State Regulations and Landlord Discretion

State and local regulations rarely mandate renters insurance, which means the requirement falls entirely on individual landlords to enforce. Virginia law permits landlords to require renters insurance as a lease condition under the Virginia Residential Landlord and Tenant Act, but does not require it. This gives landlords complete discretion to set the standard for their properties. The trend moving forward is not toward government mandates-it is toward market differentiation. Landlords who systematically require and verify coverage attract better tenants and experience fewer claims. This competitive advantage will likely push more property owners to adopt the practice, not because of regulation, but because of bottom-line results.

Tenant Screening and Market Shift

Tenant screening is shifting toward stricter standards across the board, and renters insurance requirements fit naturally into that evolution. A tenant who carries coverage demonstrates financial responsibility and commitment to their rental obligations. This screening signal matters increasingly as landlords compete for reliable tenants in tight rental markets. When you require renters insurance alongside credit checks and background screening, you assemble a more complete picture of tenant quality. The affordability of renters insurance-typically $127 annually in Virginia-removes price as a legitimate barrier. Tenants who balk at this requirement often signal other concerns worth investigating during the screening process.

Technology and Systematic Adoption

The market is moving toward landlords who treat insurance requirements as standard practice, not exceptions. Properties managed through professional property management software that automates verification and renewal tracking will increasingly outperform those managed manually. This technological shift will accelerate adoption rates as more landlords recognize that enforcement does not require additional labor when systems handle the tracking automatically. As more landlords implement these systematic approaches, the competitive pressure on property owners who ignore the requirement will intensify. Those who fail to adopt renters insurance requirements will find themselves managing higher-risk tenant pools and absorbing preventable losses.

Why Tenants Need Renters Insurance Now

Renters insurance is not a luxury or something to consider eventually. It is essential protection that costs far less than most tenants think. In Virginia, renters insurance averages $194 to $295 annually depending on location and coverage limits, which makes the decision straightforward: the cost of coverage is negligible compared to the financial devastation of losing personal property without insurance.

What Your Belongings Actually Cost to Replace

Most tenants underestimate the value of their belongings until a fire, theft, or water damage forces a reckoning. When you inventory your apartment or rental home, the replacement cost adds up fast. A laptop costs $1,200, a bedroom set runs $3,000, clothing and shoes total $2,000, and electronics and appliances add another $2,500. A single loss can easily exceed $10,000 in personal property damage. Without renters insurance, you absorb this entire loss out of pocket.

Your landlord’s building insurance covers the structure, not your possessions. This gap exists by design and by law. The National Association of Insurance Commissioners confirms that landlord policies explicitly exclude tenant personal property. Renters insurance fills this gap directly.

Choosing the Right Coverage Limits and Forms

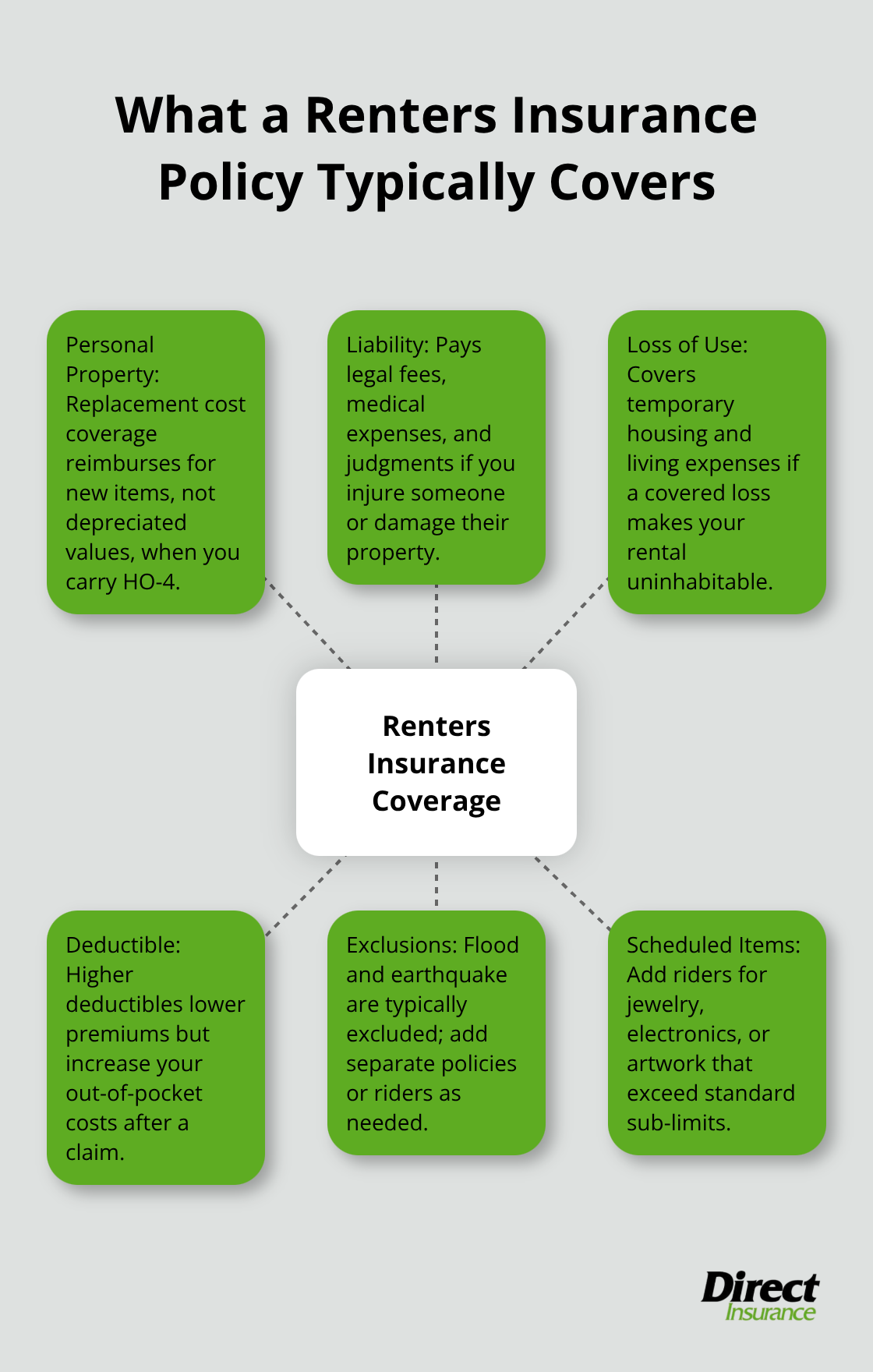

The standard policy form, known as HO-4, provides replacement cost coverage for your belongings, meaning the insurer reimburses you for new items, not depreciated values. This distinction matters enormously. Actual cash value coverage would reduce your reimbursement by depreciation, leaving you significantly underinsured after a loss.

When you calculate the replacement cost of everything you own, most renters need between $15,000 and $30,000 in personal property coverage, though higher-value tenants may require more. High-value items like jewelry, electronics, or artwork often hit policy limits, so adding scheduled personal property riders ensures adequate protection for those specific items.

Liability Protection Extends Beyond Your Home

Liability protection is where renters insurance becomes genuinely valuable beyond property coverage. If you accidentally injure someone in your rental or damage someone else’s property, your personal liability coverage pays legal fees, medical expenses, and court judgments. Experts recommend minimum liability limits of $100,000, though $300,000 or higher makes sense if you have significant assets to protect.

This coverage applies even when you are away from home. If your dog bites someone at a park, or you accidentally damage a neighbor’s car, your renters policy handles it. Loss-of-use coverage rounds out the protection by paying for temporary housing, meals, and living expenses if a covered loss makes your rental uninhabitable. If a fire forces you out for three months during repairs, this coverage pays for hotel stays and meals while the landlord’s contractor restores the unit. This protection prevents you from defaulting on rent while displaced and keeps your finances intact during a crisis.

Deductibles, Exclusions, and Smart Shopping Strategies

When you shop for policies, focus on three variables: coverage limits, deductibles, and exclusions. Higher deductibles lower your monthly premium but increase out-of-pocket costs after a claim. A $1,000 deductible typically costs less than a $500 deductible, so choose the deductible you can actually afford if a loss occurs.

Exclusions matter equally. Standard policies do not cover flood damage; you must purchase flood insurance separately through FEMA’s National Flood Insurance Program or private carriers. Earthquake coverage also requires a separate rider in most states. Bundle renters insurance with auto insurance to capture multi-policy discounts, typically saving 10-25% on your total premium.

Build a detailed home inventory with photos and receipts before a loss occurs. This documentation speeds claims processing and ensures you receive full reimbursement rather than settling for less because you cannot prove what you owned. Most insurers offer 24/7 claims support and process claims rapidly when documentation is complete.

Final Thoughts

The evidence is clear: landlords should require renters insurance, and tenants should carry it without hesitation. This requirement protects both parties from preventable financial damage and eliminates disputes that damage landlord-tenant relationships. For landlords, the benefits are concrete-you reduce liability exposure, lower your own insurance costs, and filter out tenants who resist basic financial responsibility. You also accelerate recovery after disasters by ensuring tenants have coverage for temporary housing and living expenses.

For tenants, renters insurance costs roughly $11 monthly in Virginia yet protects against losses exceeding $10,000 or more. The liability coverage alone justifies the expense, covering medical bills and legal fees if someone is injured in your rental or if you accidentally damage someone else’s property. Implementing this requirement successfully means including renters insurance in your rental criteria before applicants apply, collecting a certificate of insurance at move-in, and requesting to be named as an interested party on the policy.

Property management software can automate much of this tracking, eliminating manual work while ensuring nothing falls through the cracks. The rental market is shifting toward stricter tenant screening standards, and renters insurance requirements fit naturally into that evolution. If you need guidance on structuring your renters insurance requirement or want to review your own coverage, Direct Insurance Services offers personalized solutions tailored to your specific situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation