Home Insurance for Rentals: Guarding Your Investment

Rental property owners face a critical gap that most don’t realize until it’s too late. Your standard homeowners policy won’t cover a property you’re renting out to tenants, leaving your investment exposed to significant financial risk.

At Direct Insurance Services, we’ve seen countless landlords scramble to find proper coverage after discovering their existing policy is worthless. Home insurance for rentals works differently than personal coverage, with higher liability limits and specific protections for loss of rental income.

Why Your Homeowners Policy Won’t Protect a Rental

Standard homeowners policies explicitly exclude rental properties, and this isn’t a gray area or a technicality you can work around. When you rent out your home or purchase a property specifically to lease it, your HO policy becomes void the moment a tenant moves in. Insurance companies view owner-occupied and rental properties as fundamentally different risk profiles. An owner protecting their primary residence faces different hazards than a landlord managing tenant behavior, guest injuries, and income disruption. If you file a claim on a rental property while carrying a homeowners policy, the insurer will deny it outright. Landlords lose tens of thousands in repair costs when they fail to switch to proper coverage.

The data backs this up: from 2019 to 2023, homeowners filed an average of 5.64 claims per 100 house-years, according to ISO data cited by the Insurance Information Institute. Those claims averaged $17,059 each.

Higher Liability Exposure with Tenants

For rental properties, the stakes rise because you face liability not just for your own injuries but for anyone on the property, including tenants and their guests. A tenant’s guest slips on your icy walkway and breaks their leg. Your homeowners policy won’t cover their medical bills or any lawsuit that follows. Liability coverage in rental situations typically starts around $300,000 to $1,000,000, compared to the standard $100,000 to $300,000 in homeowners policies. This difference exists because tenant-occupied properties attract more foot traffic, longer occupancy periods, and greater exposure to injury claims. Landlord policies protect you against these elevated risks with adequate liability limits from the start.

The Income Loss You’re Not Prepared For

Property damage hits differently when you depend on rental income. If a fire damages your rental property and it becomes uninhabitable for three months during repairs, a homeowners policy won’t reimburse you for the lost rent. Landlord insurance includes loss of rent coverage, which replaces your income while the property undergoes restoration. This matters tremendously: the median monthly rent varies by location, but losing three months of income on a $1,500 monthly rental means $4,500 in unrecovered losses. Wind and hail cause roughly 38 to 43 percent of homeowners losses annually, according to ISO data, and water damage accounts for approximately 22 to 23 percent. Both scenarios can force tenants out temporarily.

Without loss of rent protection, you absorb the full financial hit while paying for repairs. Landlord policies also handle tenant-caused damage differently. If a tenant punches a hole in drywall, breaks appliances, or causes intentional harm, a homeowners policy treats this as outside its scope. Landlord policies can include tenant damage coverage as an add-on, which protects you against repair costs from tenant negligence or intentional harm. This distinction matters because tenant damage claims happen regularly, and the costs add up fast when you manage multiple units or frequent turnover.

What Landlord Insurance Actually Covers

Landlord insurance fills the gaps that homeowners policies leave wide open. The policy covers the dwelling structure itself, liability protection for injuries on the property, and loss of rent during covered losses. Some policies also cover other structures on the property (like detached garages or sheds) and provide medical payments coverage for guest injuries. You can add endorsements for appliance breakdown, water backup, or vandalism protection depending on your property’s specific needs. The right landlord policy transforms your rental from a financial liability into a protected investment, allowing you to move forward with confidence toward selecting the specific coverage limits and endorsements that match your property’s profile.

What Landlord Insurance Actually Protects

Core Coverage Categories for Rental Properties

Landlord insurance divides into distinct coverage categories, each addressing specific rental risks that homeowners policies ignore entirely. Dwelling coverage protects the structure itself against fire, storms, vandalism, and other named perils, typically covering replacement cost rather than depreciated value. This matters because rebuilding costs have climbed significantly. Other structures coverage extends to detached garages, sheds, or fences on your property. Loss of rent coverage reimburses your monthly rental income while the property undergoes repairs after a covered loss, addressing the exact income gap that homeowners policies leave exposed.

Liability and Medical Payments Protection

Liability coverage starts at $300,000 to $1,000,000 depending on your policy, protecting you when a tenant or their guest suffers an injury on the property and names you in a lawsuit. Medical payments coverage handles smaller injury claims without requiring a lawsuit, paying directly for treatment up to your policy limit. Tenant damage coverage, available as an add-on, protects against holes in walls, broken fixtures, or intentional destruction caused by occupants-damage that occurs regularly in rental situations and costs thousands to repair.

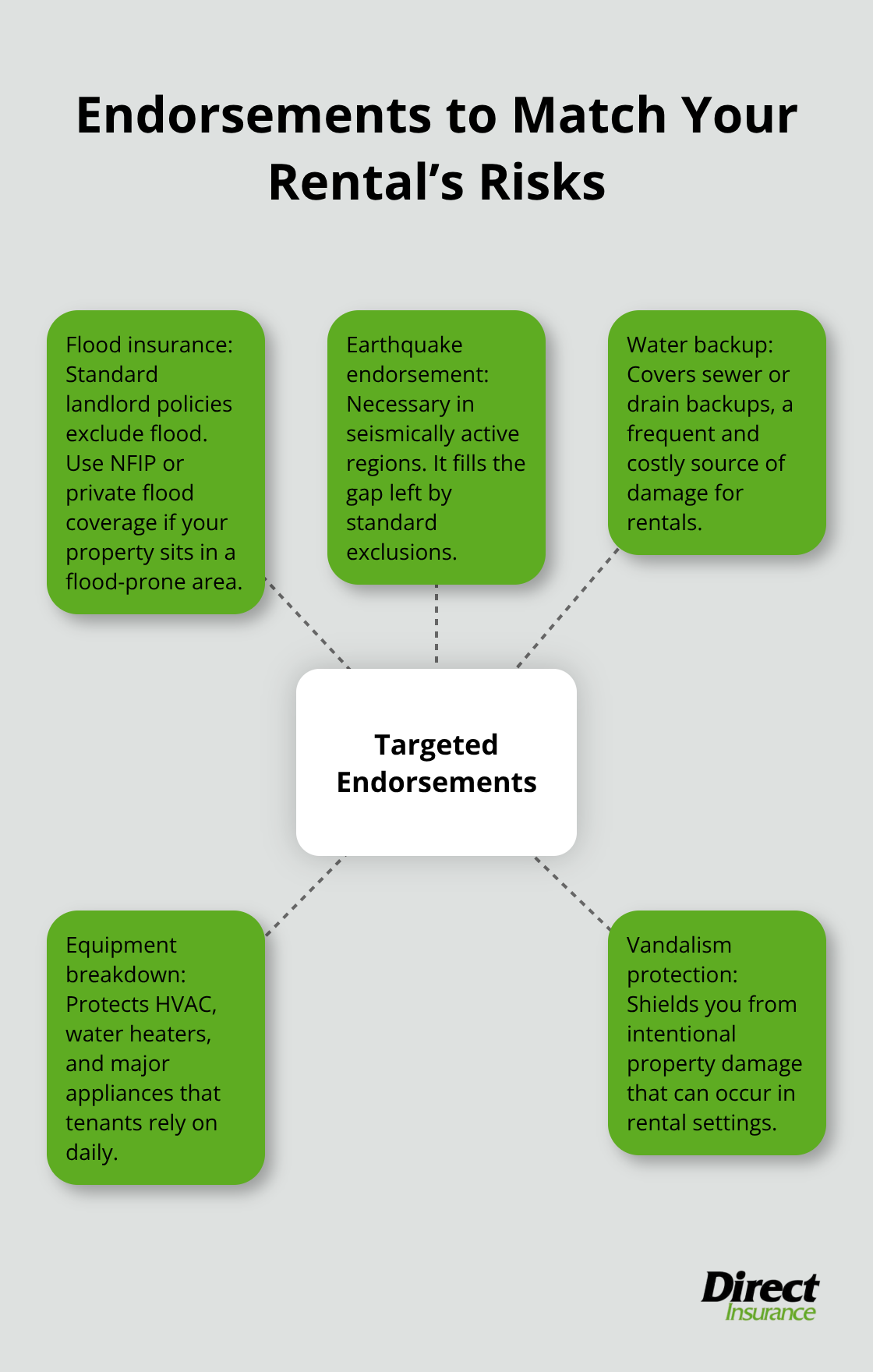

Endorsements That Match Your Property’s Actual Risks

The key distinction separating adequate landlord insurance from inadequate coverage lies in how you customize endorsements to match your property’s actual risks. If your rental sits in a flood-prone area, standard landlord policies exclude flood damage, requiring a separate National Flood Insurance Program policy or private flood insurance rider. Earthquake coverage requires its own endorsement in seismically active regions like Utah. Water backup endorsements cover damage from sewer or drain backups, addressing one of the most expensive repair scenarios landlords face. Equipment breakdown coverage protects mechanical systems like HVAC units, water heaters, and appliances-critical for rental properties where tenant complaints about broken systems lead to costly emergency repairs.

Vacancy Rules and Tenant Insurance Requirements

Vacancy endorsements matter tremendously because most landlord policies limit or void coverage when a property sits empty for 30, 60, or 90 days depending on the carrier. If you’re renovating between tenants or managing a seasonal rental, verify your policy’s vacancy rules upfront to avoid discovering coverage gaps mid-project. Requiring tenants to carry renters insurance reduces your exposure significantly, as their policy covers their personal belongings and liability while your landlord policy covers only the structure and your liability as the property owner.

Shopping for the Right Policy Details

When shopping for quotes, request specific details on deductibles, coverage limits for dwelling and liability, and which endorsements are standard versus optional-this information drives both premium cost and claim outcomes substantially. Different carriers structure their policies differently, meaning one insurer’s standard package may exclude protections that another includes automatically. The comparison process reveals which carriers align with your property’s profile and which ones leave gaps you’d need to fill with expensive add-ons. Once you understand what each policy actually covers, you can move forward with confidence toward selecting the specific limits and endorsements that protect your investment from the ground up.

Selecting the Right Coverage Limits for Your Rental

Calculate Your Property’s True Replacement Cost

Start with your property’s actual replacement cost, not its market value. Market value and replacement cost diverge significantly, especially in competitive real estate markets. If your rental property sells for $400,000 but reconstruction from the ground up costs $550,000 after a total loss, your coverage limit must reflect the rebuild figure.

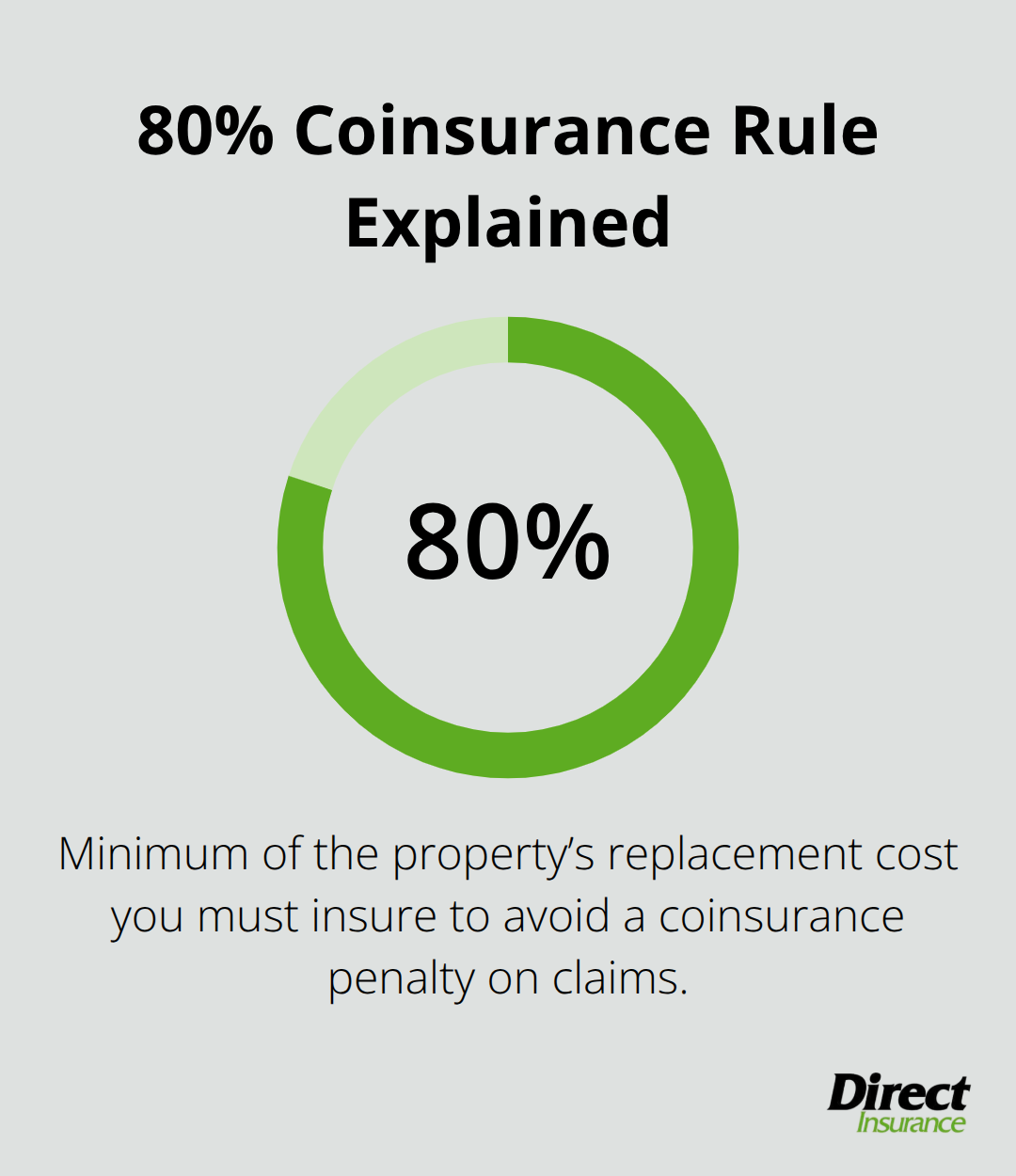

Insurance companies apply the 80% coinsurance rule-you need to insure at least 80% of replacement cost to avoid penalties on claims. Underinsure with only $300,000 in dwelling coverage when replacement cost reaches $550,000, and the insurer reduces your claim payout proportionally. This isn’t theoretical; it’s how claims actually settle. The Insurance Information Institute reports that from 2019 to 2023, average homeowners claims cost $17,059 each, but fire losses alone averaged $99,613 to $173,111 per claim during 2020 to 2024. Your dwelling coverage must handle total reconstruction, not partial repairs.

Set Liability Limits Based on Your Property’s Risk Profile

For liability coverage, $300,000 represents the bare minimum for a single-family rental, but $500,000 to $1,000,000 proves more appropriate if your property attracts multiple guests, sits in a densely populated area, or features a pool or trampoline that increases injury risk. A tenant’s guest slips on your icy walkway and breaks their leg-your liability coverage protects you when they file a lawsuit. Higher limits cost more upfront but shield you from catastrophic financial exposure that could exceed your property’s value. Umbrella policies offer additional protection when standard liability limits prove insufficient for your asset portfolio.

Determine Loss of Rent Coverage That Matches Your Income

Loss of rent coverage should replace your actual monthly rental income for at least six months of vacancy. Calculate your annual rent divided by 12, then multiply by six. If you collect $1,800 monthly, you need $10,800 in loss of rent coverage minimum. Most carriers allow you to adjust this limit based on your specific income needs, so tailor the amount to your actual financial situation rather than accepting a standard default.

Compare Quotes with Identical Coverage Across Multiple Carriers

Compare quotes from at least three carriers simultaneously, requesting identical coverage limits and deductibles across all quotes so you can see actual price differences rather than policy structure differences. When USAA, State Farm, Allstate, and regional carriers all quote the same $500,000 dwelling limit with $500,000 liability and $10,000 loss of rent, you’ll spot which company genuinely offers better rates versus which one simply structured a cheaper-looking policy with lower limits. Request quotes with both $500 and $1,000 deductibles to understand how deductible selection impacts your premium-sometimes the savings don’t justify the higher out-of-pocket exposure.

Verify Endorsements, Exclusions, and Lender Requirements

Ask each carrier specifically which endorsements come standard and which cost extra. Water backup coverage might be included by one insurer but cost $150 annually from another. Equipment breakdown protection might be standard at Company A but optional at Company B. These differences compound across your policy’s lifespan. Review the policy documents themselves, not just the quote summary, because exclusions hide in the fine print. Most landlord policies exclude flood, earthquake, and wear-and-tear damage automatically. If your property sits in a flood zone according to FEMA maps, you’ll need separate flood insurance through the National Flood Insurance Program or a private flood insurer. Seismically active regions like Utah require earthquake endorsements that standard policies exclude. Verify your lender’s specific requirements too-mortgage lenders often mandate minimum coverage amounts, specific deductible limits, and replacement cost valuation rather than actual cash value. Failing to meet lender requirements can trigger a force-placed policy that costs significantly more and provides minimal coverage.

Final Thoughts

Protecting your rental investment requires moving beyond standard homeowners coverage and committing to landlord insurance that addresses the specific risks you face. Your dwelling coverage must reflect true replacement cost, your liability limits should match your property’s risk profile, and your loss of rent protection needs to cover your actual monthly income for at least six months. Verify that your policy includes the endorsements your property requires, whether that’s water backup coverage, equipment breakdown protection, or flood insurance through a separate carrier.

Getting quotes from multiple carriers reveals the real price differences in the market. Request identical coverage limits across all quotes so you’re comparing apples to apples, not just looking at premium numbers that reflect different policy structures. The comparison process takes time, but it directly impacts how much you’ll pay annually and whether your home insurance for rentals actually protects you when a claim occurs.

Contact Direct Insurance Services to get quotes from carriers that understand rental property risks. We work with top-rated carriers to help you find coverage that fits your specific situation and budget. The investment in proper coverage today prevents financial devastation tomorrow.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation