Home Insurance Policy Guide: What Every Homeowner Should Know

Homeownership comes with real financial responsibility. Your house is likely your biggest asset, and protecting it properly matters more than most people realize.

At Direct Insurance Services, we’ve helped thousands of homeowners navigate their coverage options. This home insurance policy guide walks you through the essentials so you can make informed decisions about your protection.

Understanding Home Insurance Coverage Types

Your homeowners policy isn’t one monolithic protection. It’s built from distinct coverage types, and understanding what each one actually covers-and what it doesn’t-separates homeowners who are truly protected from those who face gaps when they need help most.

Dwelling Coverage Protects Your Home Structure

Dwelling coverage forms your foundation. This covers the structure of your home itself: the walls, roof, floors, built-in appliances, and permanent fixtures. If a fire damages your kitchen or a storm tears off your roof, dwelling coverage pays for repairs or rebuilding up to your policy limit.

Most lenders require you to insure your home for at least 80 percent of its replacement cost. This threshold matters because if you underinsure, insurers apply a coinsurance penalty that reduces what you actually receive. For example, if your home costs $200,000 to replace but you only insure it for $150,000, a $40,000 loss might only pay out $30,000.

Get a professional replacement cost estimate before you buy. Don’t rely on your home’s market value or what you paid for it years ago-construction costs have shifted significantly.

Personal Property Covers Your Belongings Separately

Personal property coverage operates as your second layer, independent from dwelling coverage. This protects your furniture, electronics, clothing, and other movable items inside your home. Standard policies typically limit personal property to 50 to 70 percent of your dwelling limit according to the Insurance Information Institute.

So if you insure your dwelling for $200,000, personal property might max out around $100,000 to $140,000. This limit often isn’t enough for high-value items. Jewelry, fine art, antiques, and electronics may need scheduled personal property endorsements that list each item separately with its own coverage limit.

Without scheduling, you receive actual cash value minus depreciation, which means a five-year-old laptop worth $800 new could be valued at $200 when you file a claim. Scheduled items typically pay replacement cost without depreciation, which is why they matter if you own valuable possessions.

Liability Coverage Protects Your Financial Future

Liability coverage is where most homeowners are dangerously underinsured. This protects you when someone is injured on your property or when you accidentally damage someone else’s property, and they sue you. Standard policies often include $100,000 in personal liability coverage, which sounds substantial until you realize a serious injury lawsuit can easily exceed $500,000.

Medical expenses for a guest who slips on your icy driveway can spiral quickly, and if they pursue legal action, your homeowners policy stands between your home and a judgment against you. Umbrella liability insurance adds an extra layer of protection, typically starting at $1 million in coverage for a modest additional premium.

If you have significant assets or host gatherings regularly, umbrella coverage is practical insurance, not optional luxury. The next section walks you through the specific factors that insurers use to calculate your premium-and why some of these factors matter far more than homeowners typically realize.

Factors That Affect Your Home Insurance Premiums

Location Determines Your Base Rate

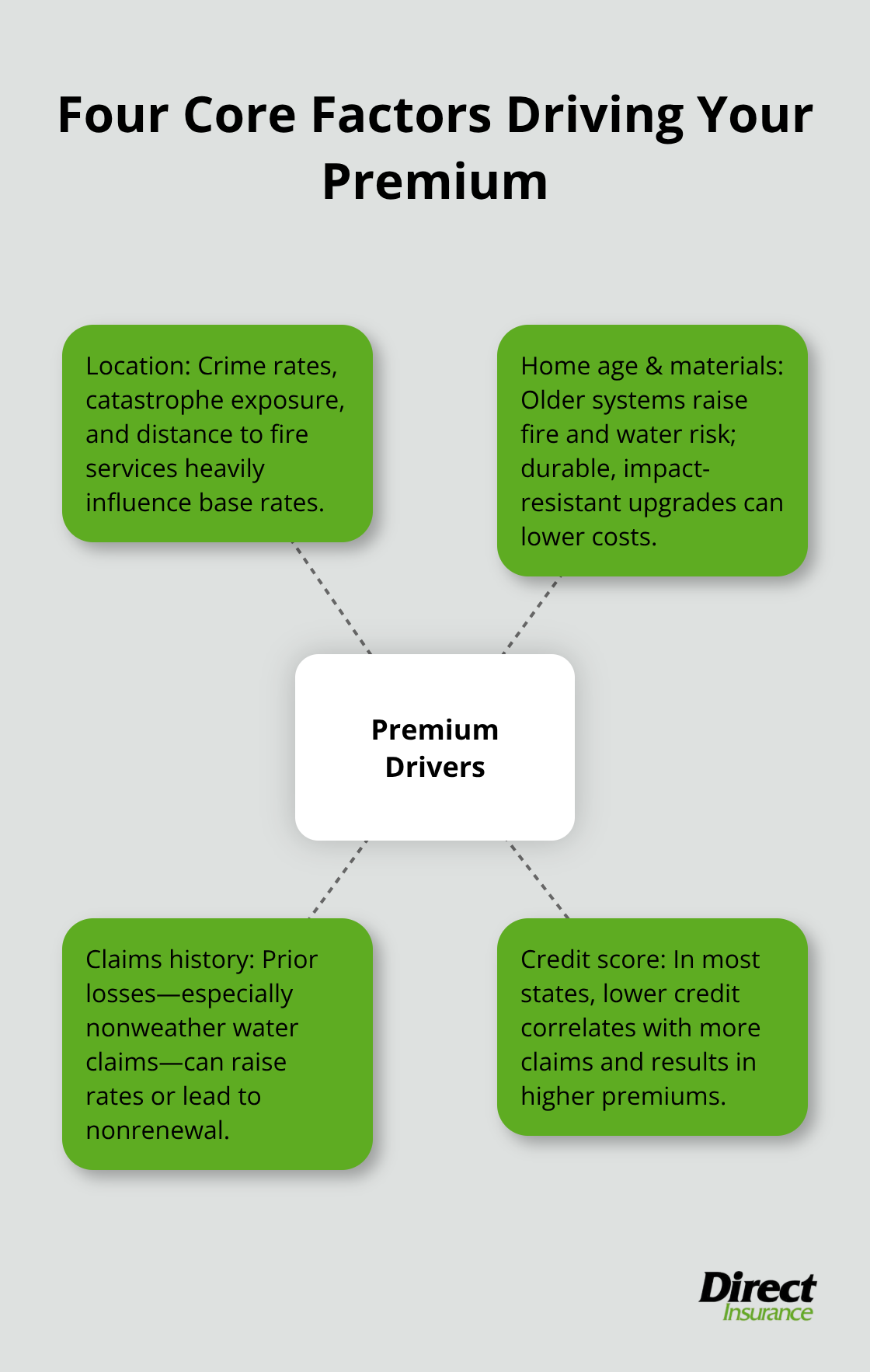

Insurers don’t calculate your premium by throwing darts. They assign rates based on measurable risk factors, and understanding which ones matter most helps you identify where you can actually save money and where you genuinely cannot. Location carries the heaviest weight in this calculation. If your home sits in a high-crime neighborhood, your premium rises. If it stands near the coast where hurricane risk is real, your premium rises further. Texas Department of Insurance guidance confirms that distance to the nearest fire department or water source directly affects your rate, which is why rural homes often cost more to insure than urban ones despite lower crime. You cannot change your location, but you can obtain a replacement cost estimate specific to your area since construction costs vary dramatically by region. A contractor in California faces different material and labor costs than one in rural Montana, and your insurer knows this.

Home Age and Construction Materials Shape Your Costs

Home age and construction materials form your second major factor, and here you have limited but real leverage. Homes built before 1980 typically cost more to insure because older wiring, plumbing, and roofing systems present higher fire and water damage risk. If your roof exceeds 20 years old, many insurers will demand a professional inspection or refuse coverage altogether. Upgrading to impact-resistant roofing in storm-prone areas can lower your premium by a meaningful amount. Construction type matters too: a home framed in wood costs more to insure than one with cement or steel framing because wood burns faster. You cannot change what your house is made of without major renovation, but if you are renovating, this is worth factoring into your decisions.

Your Claims History Follows You for Seven Years

Your claims history is where insurers show their true bias, and it stings. A home insurer claims history tracking report shows the claims filed for any house for the past seven years. A single water damage claim can raise your rates for years, and three or more nonweather-related claims in three years can trigger nonrenewal. This means filing a small claim on your homeowners policy can cost you far more in higher premiums over time than simply paying out of pocket. Get a free copy of your CLUE report annually from LexisNexis and challenge any incorrect information immediately.

Credit Score Affects Rates More Than You’d Expect

Credit score also affects your rate in most states, which feels unfair but reflects actuarial data: people with lower credit scores file more claims. You have no quick fix here, but understanding that paying bills on time indirectly lowers your insurance costs might motivate you to manage credit more aggressively. These four factors-location, home age, claims history, and credit-form the foundation of your premium calculation. The next section shows you how to use this knowledge when comparing policies and selecting coverage limits that actually match your situation.

How to Choose the Right Home Insurance Policy

Get an Accurate Replacement Cost Estimate

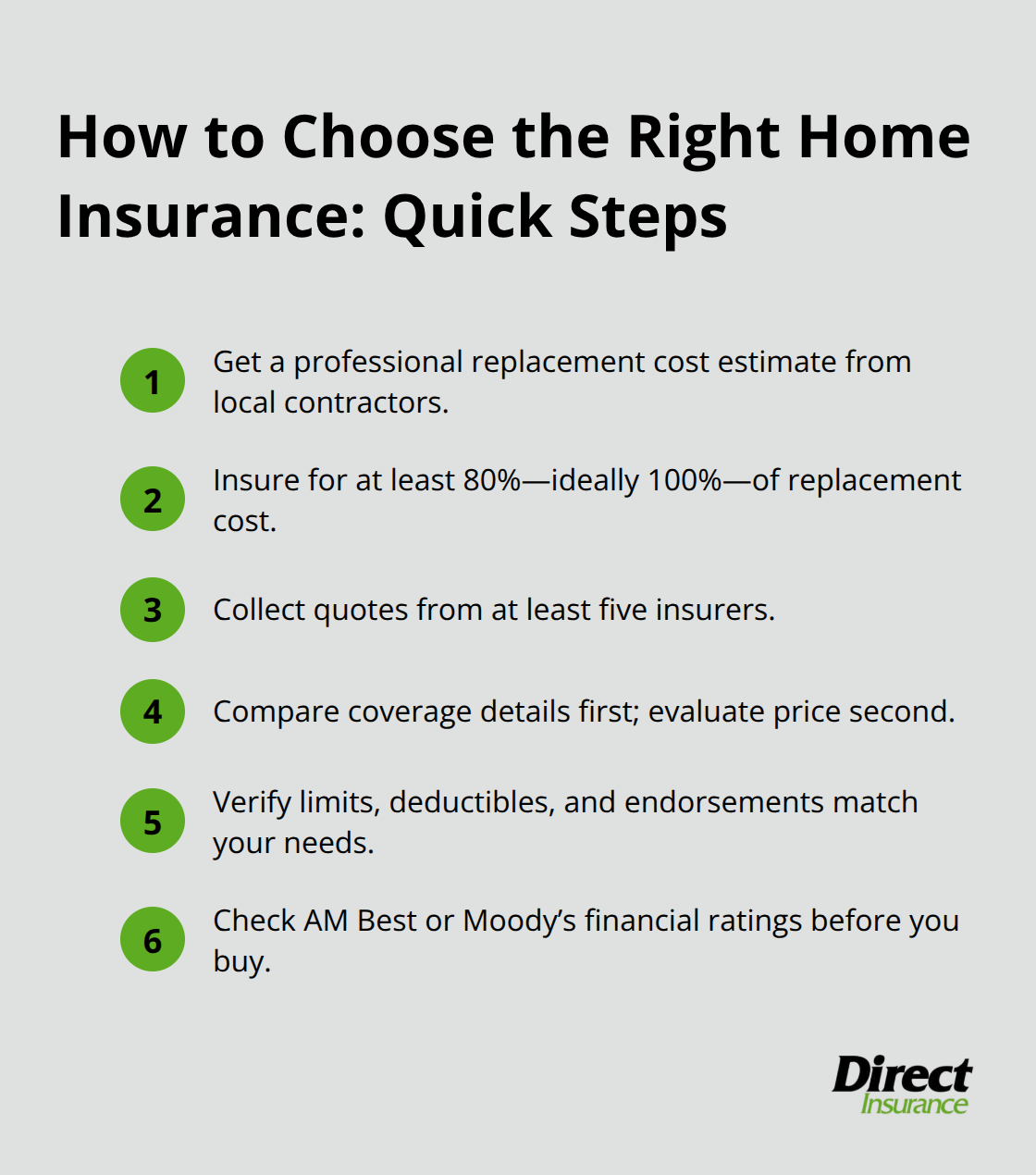

The single most important decision you make when shopping for homeowners insurance is getting your replacement cost estimate right, and most homeowners fail at this step. You need a professional replacement cost appraisal, not a guess based on what you paid for the house or what it would sell for today. A replacement cost estimate is what it may cost to rebuild your home at today’s construction prices. Regional variation is extreme, and a contractor in Salt Lake City charges different rates than one in a rural Utah county.

Contact three local contractors and request a detailed replacement cost estimate that accounts for current labor and material prices in your area. This number becomes your baseline for all future decisions. If your estimate says $250,000 to rebuild but you insure for only $200,000, the coinsurance penalty reduces your claim payout proportionally. Insure for at least 80 percent of replacement cost, and try for 100 percent if your budget allows. Obtain that estimate before you contact insurers, not after, because it fundamentally changes how you evaluate quotes.

Compare Quotes from Multiple Carriers

Obtain quotes from at least five different insurers. Do not settle for three quotes or call your bank’s preferred provider and assume that’s competitive. Insurance premiums vary wildly between carriers for identical homes and coverage. One insurer might quote $1,200 annually while another quotes $1,600 for the same dwelling limit and deductible, and neither quote is wrong. The difference reflects how each carrier weights risk factors and how aggressively they price in your market.

When you compare quotes, ignore the premium amount initially and focus on what each quote actually covers. One policy might include extended replacement cost coverage as standard while another charges extra. One might limit personal property to 50 percent of dwelling coverage while another defaults to 70 percent. Read the declarations page on each quote carefully. This page is a concise summary of your coverages, dollar limits, and deductibles according to Texas Department of Insurance guidance.

Verify Coverage Details Match Your Needs

Verify that dwelling limit, personal property limit, liability limit, and deductible match what you intended to purchase. After you confirm coverage is identical across quotes, then compare premiums and select based on price and insurer reputation. Check financial stability ratings through AM Best or Moody’s so you know the company can actually pay claims when disaster strikes. A slightly higher premium from a financially stable insurer beats a bargain rate from a carrier that might struggle to pay large claims (and many carriers do struggle after major disasters).

Final Thoughts

You now understand the core components of a home insurance policy guide: dwelling coverage protects your structure, personal property coverage protects your belongings, and liability coverage protects your financial future. Location, home age, claims history, and credit score drive your premiums in measurable ways. Replacement cost estimates matter far more than market value, and comparing quotes from multiple carriers reveals real savings opportunities.

The gap between adequate protection and genuine vulnerability often comes down to one decision: whether you act or delay. Most homeowners know they need insurance but never verify their coverage limits match their actual replacement costs. They accept the first quote without comparison, and they ignore their CLUE report, missing opportunities to challenge inaccurate claims history.

Your next step is straightforward: obtain a professional replacement cost estimate from local contractors, then contact at least five insurers for quotes using that estimate as your baseline. Review the declarations page on each quote to confirm coverage details match your needs, and check financial stability ratings so you know your carrier can actually pay when disaster strikes. If this process feels overwhelming, Direct Insurance Services works with top-rated carriers to help you navigate these decisions without pressure or one-size-fits-all solutions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation