How to Calculate Your Home Insurance Rate

Your home insurance rate depends on dozens of factors-some you control, others you don’t. Understanding what goes into the calculation helps you spot savings opportunities and avoid overpaying.

At Direct Insurance Services, we’ve helped thousands of homeowners calculate their home insurance rates and find better deals. This guide walks you through exactly how insurers price your coverage and what you can do about it.

What Actually Drives Your Home Insurance Rate

Location Sets Your Premium Foundation

Your postal code matters more than you think. Insurance Bureau of Canada data shows that location ranks among the top three factors determining your premium, and the differences are dramatic. If you live in an area with frequent severe weather, higher crime rates, or poor fire protection, you’ll pay significantly more than someone in a low-risk neighborhood. Proximity to a fire station or hydrant lowers your premium because faster response reduces the risk of total loss. In 2024, Canada experienced severe weather-related insured losses surpassing $8 billion, setting a record that insurers are now pricing into premiums across affected regions.

Home Age and Construction Type Impact Your Rate

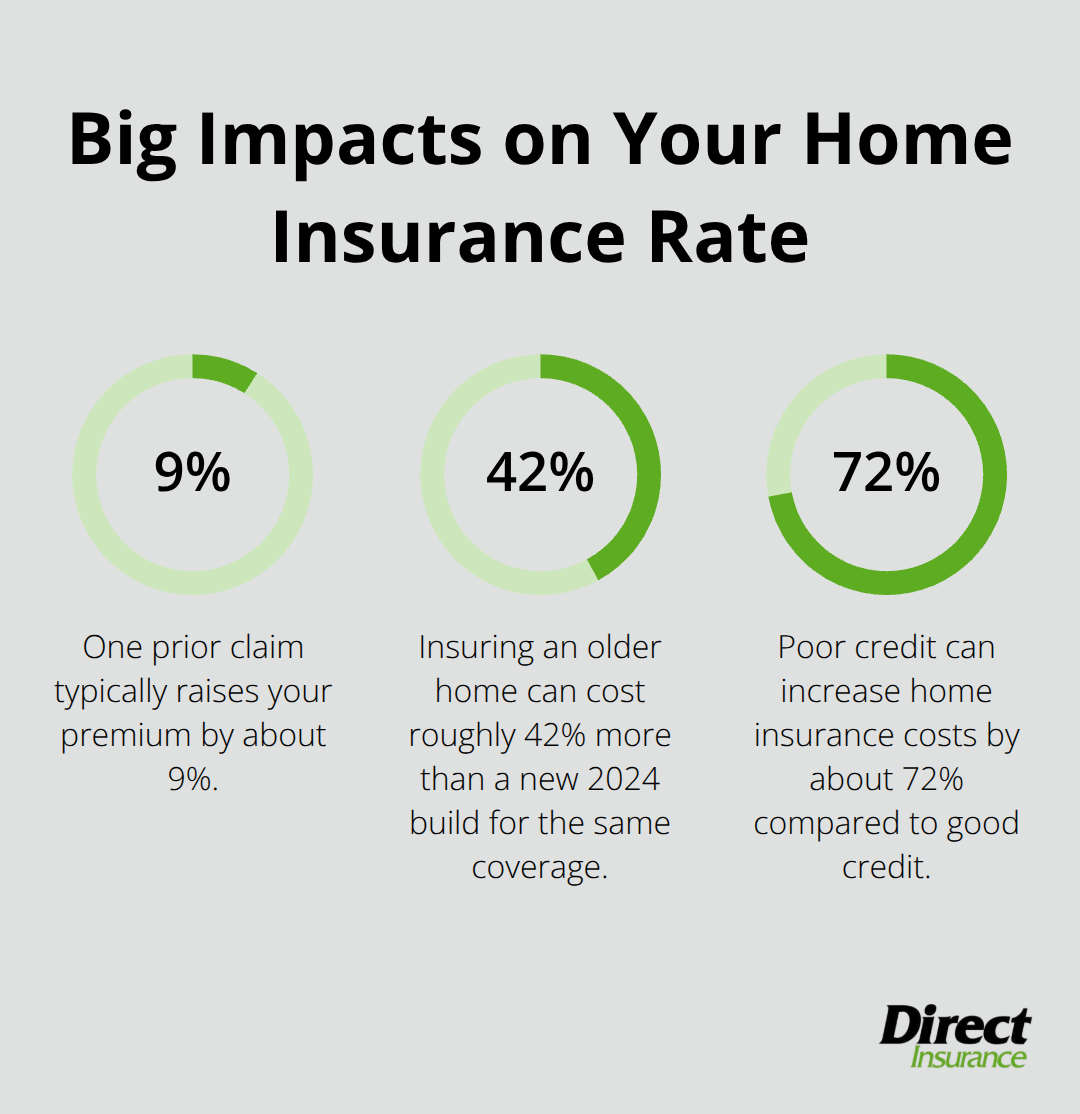

A house built in 1955 or 1984 typically costs around 2,110 dollars annually to insure, while a newer 2024 build averages about 1,220 dollars-that’s a 42 percent difference for the same coverage. Older homes carry higher risk because aging electrical systems, plumbing, and roofing increase the likelihood of claims. If your roof is over 20 years old, many insurers will either charge you more or require an inspection before covering you. Wood-frame houses cost more to insure than brick or stone construction because they burn faster. A home’s square footage also affects your rate-larger homes mean higher replacement costs, so a 3,000-square-foot house will cost more to insure than a 2,000-square-foot one.

Your Claims History and Credit Score Hit Hard

One previous claim raises your premium by roughly 9 percent compared to a clean record. Two claims within five years can push your rate up 20 to 30 percent. Insurers view you as higher risk if you’ve filed claims, even for events outside your control like weather damage. Some companies will drop you after three claims in five years, leaving you scrambling for coverage. Your credit score influences pricing in most provinces and states, though some jurisdictions prohibit it. A homeowner with good credit pays around 2,110 dollars annually, while someone with poor credit pays roughly 3,620 dollars for identical coverage-that’s a 72 percent difference. If your insurer uses credit scoring and your rate seems high, request an explanation and check your credit report for errors with Equifax or TransUnion. Correcting inaccuracies can lower your premium.

Home Improvements Lower What You Pay

The age and type of upgrades you’ve made matter significantly. A new roof, updated electrical panel, or modern plumbing system reduces your rate because these improvements lower claim risk. If you’ve installed centrally monitored fire, water, or burglar alarms, you qualify for additional discounts that can cut 5 to 15 percent off your premium. These tangible improvements signal to insurers that you take property maintenance seriously, and they reward that commitment with lower rates. Understanding these specific factors helps you identify which ones you can control and which ones shape your baseline rate.

How Insurers Price Your Coverage

Replacement Cost Sets Your Dwelling Coverage

Insurers don’t pull premium numbers from thin air-they calculate them using three concrete steps that directly impact what you pay. First, they assess your home’s replacement cost, which differs fundamentally from what you paid for it or what it would sell for today. A house purchased for $256,000 might cost $180,000 to rebuild due to land value, or it could cost $320,000 if materials and labor are expensive in your region. This is why two homes on the same street can have wildly different dwelling coverage amounts and premiums.

If your agent quotes $297,000 in dwelling coverage for a home you bought at $256,000, that’s not necessarily inflated-it reflects actual rebuild costs in your area. The replacement cost approach protects you from underinsurance, which leaves you vulnerable if a total loss occurs. Inflation and supply chain disruptions continue to push rebuild costs higher, so your coverage amount should reflect current conditions rather than your original purchase price.

Risk Evaluation Examines Your Specific Hazards

The second step involves risk evaluation. Insurers analyze your specific hazards and exposure by examining local fire protection ratings, crime statistics, weather patterns, and your property’s individual vulnerabilities. A home near a fire station qualifies for better rates than one ten miles away because response time directly affects loss severity. Your personal risk factors matter too: a trampoline, pool, or aggressive dog breed can increase your liability exposure and raise premiums by 10 to 25 percent depending on the carrier.

These hazard assessments happen at both the neighborhood and property level. Insurers pull data on local claim history, natural disaster frequency, and infrastructure quality to establish baseline risk. Then they layer in your home’s specific features-roof condition, security systems, and maintenance history-to calculate your individual premium.

Comparison Shopping Reveals Substantial Savings

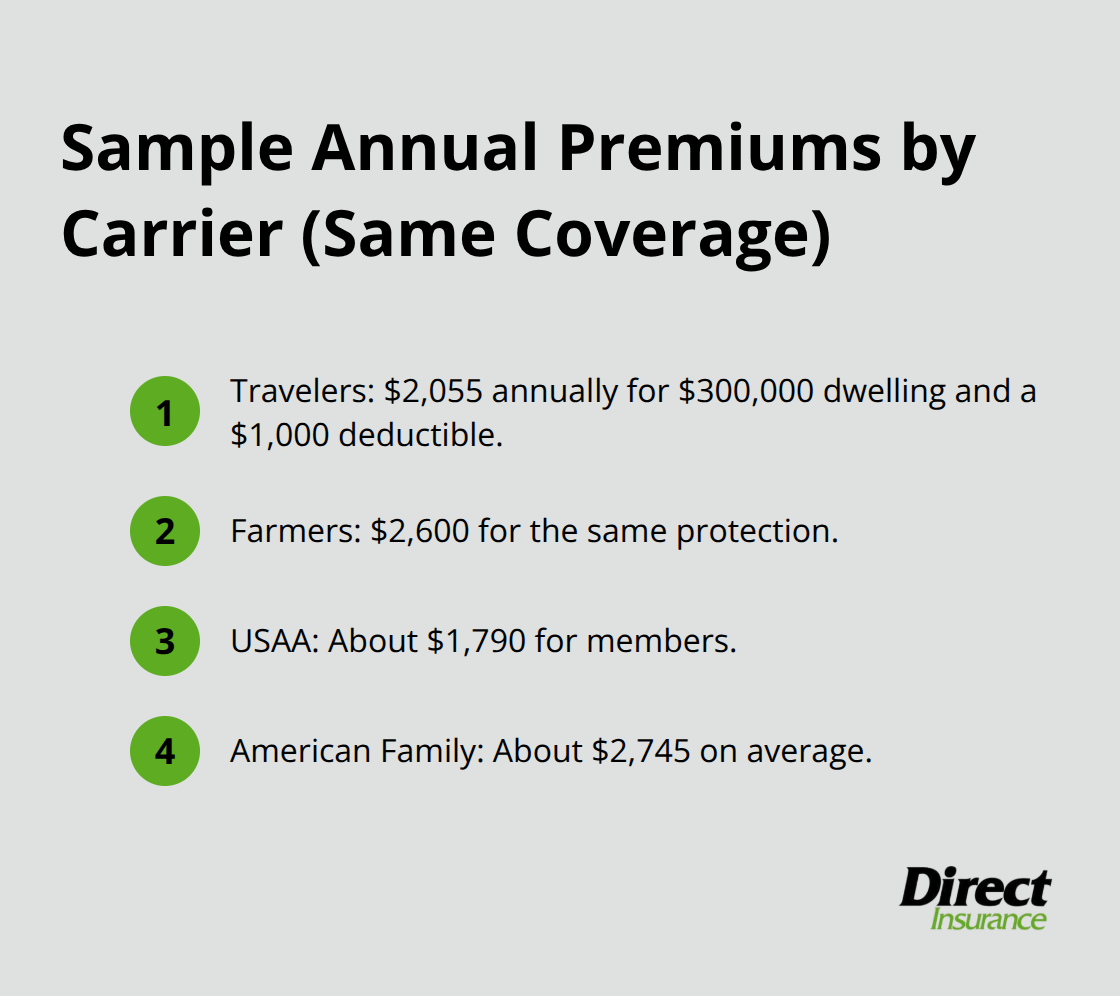

The third step is comparison shopping, which most homeowners skip entirely-and that’s a costly mistake. Premium variation between carriers for identical coverage is substantial. For a standard policy with $300,000 dwelling coverage and a $1,000 deductible, national averages show Travelers at $2,055 annually while Farmers charges $2,600 for the same protection. USAA members pay roughly $1,790, and American Family averages $2,745. That’s a $955 difference between the cheapest and most expensive option, or 46 percent.

Location amplifies these differences dramatically. Houston averages $6,370 annually across major insurers, while San Jose averages $1,090 for comparable policies. Getting quotes from at least three carriers reveals where you stand and identifies which company values your specific risk profile most favorably. Many homeowners accept their first quote without realizing they could save hundreds annually by switching to a carrier that better matches their situation.

As an independent agency serving Utah, we work with multiple top-rated carriers to show you these differences side by side. This approach makes it simple to see which option truly fits your needs and budget without pressure toward any single company. The next section walks you through the specific actions that lower your rate, starting with the deductible choice that affects your premium most directly.

Cut Your Premium Without Cutting Coverage

Raise Your Deductible to Lower Annual Costs

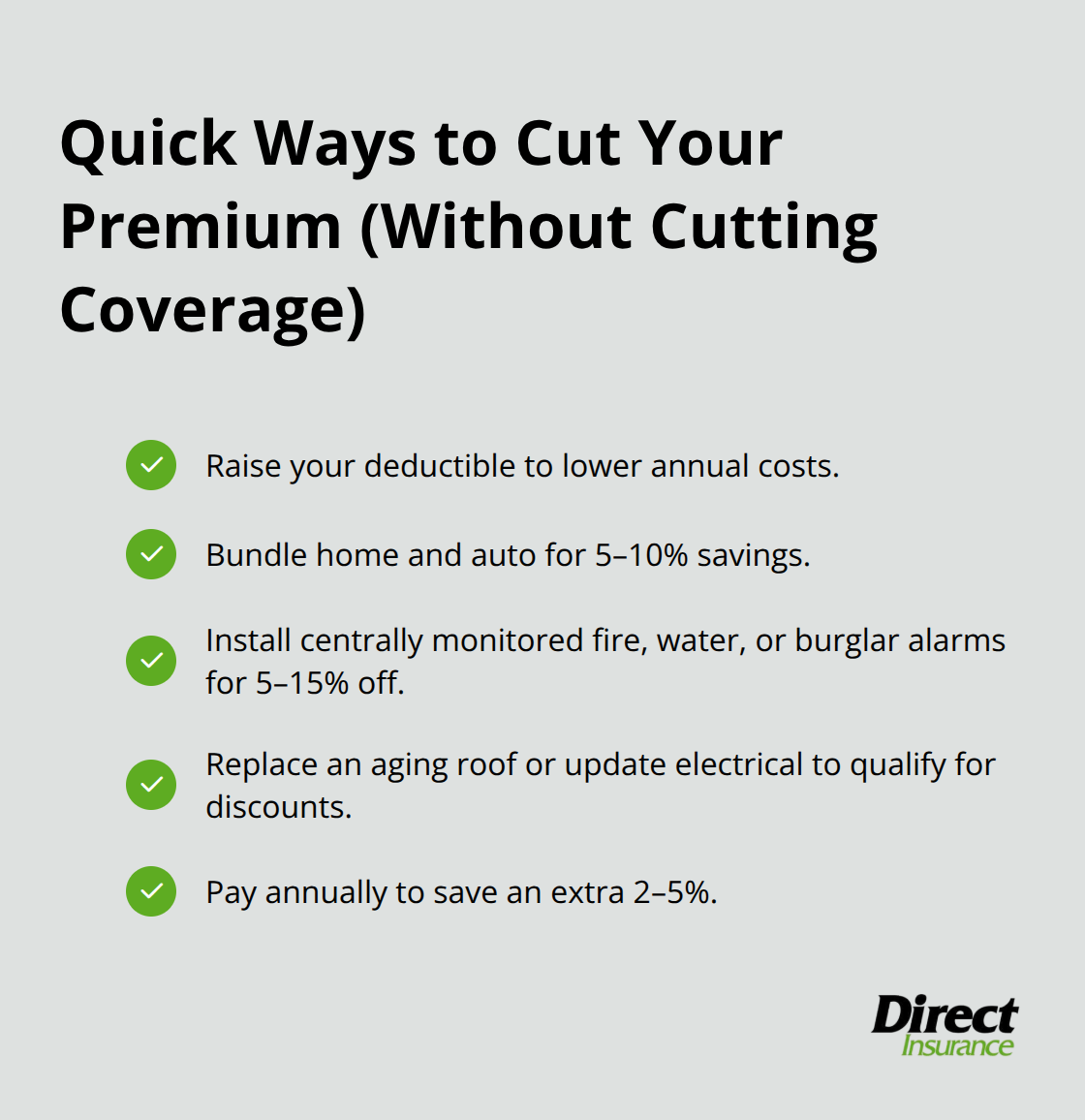

Increasing your deductible from $1,000 to $2,500 cuts your average premium, making it the fastest way to lower your bill immediately. You agree to pay more out of pocket when a claim happens, so insurers reward that choice with lower annual costs. If you increase your deductible to $2,500, your premiums might drop to $2,250 a year-saving you $250 annually. The key is selecting a deductible you can actually afford to pay if disaster strikes. If you have $2,500 in emergency savings, a $2,500 deductible makes sense. If you don’t, stick with $1,000 or $1,500. Many homeowners jump to $2,500 or higher without considering whether they could cover it, which defeats the purpose of insurance. Try the math on what your emergency fund can handle, then select the deductible that maximizes savings without creating financial stress.

Bundle Policies and Claim Available Discounts

Combining your home and auto policies with the same insurer delivers a multi-policy discount that typically saves 5 to 10 percent on your total bill. If you pay $2,110 for home insurance and $1,500 for auto, bundling could save $175 to $360 annually across both policies. Ask your insurer about loss-prevention discounts beyond bundling.

Centrally monitored fire, water, or burglar alarms cut your premium by 5 to 15 percent because they directly reduce claim severity. A new roof or updated electrical system can also qualify for discounts in some cases, though upgrading purely for a discount rarely pays back financially unless the improvement was needed anyway. Paying your annual premium upfront instead of monthly sometimes yields an additional 2 to 5 percent discount.

Invest in Home Improvements That Reduce Risk

Home improvements matter most when they address genuine risk rather than chasing discounts. A 30-year-old roof that’s failing costs more to insure than a 10-year-old roof, and replacing it brings your rate down while protecting your home. Maintenance consistency signals to insurers that you take property care seriously, which can help you stay in a lower rating tier at renewal. When you upgrade your roof, electrical system, or plumbing, you reduce the likelihood of claims, and insurers recognize that reduction through better rates. These tangible improvements demonstrate commitment to property safety, and carriers reward that commitment with lower premiums.

Final Thoughts

Your home insurance rate reflects dozens of interconnected factors, but the core drivers remain consistent: location risk, property characteristics, claims history, and the coverage limits you select. Location sets your baseline because fire protection, crime rates, and weather patterns directly influence claim frequency and loss severity. Home age and construction type determine replacement costs, which anchor your dwelling coverage amount and shape your premium tier.

When you calculate your home insurance rate yourself, focus on three concrete steps that reveal your actual costs. First, determine your actual replacement cost rather than relying on purchase price or market value. Second, assess your specific hazards honestly, including property features and maintenance condition, then get quotes from multiple carriers to see how different companies value your risk profile.

Taking action now pays dividends immediately and over time. Raising your deductible to a level you can afford cuts your annual premium without reducing protection when you need it most, while bundling home and auto policies saves 5 to 10 percent. At Direct Insurance Services, we help Utah homeowners navigate these decisions by comparing quotes from top-rated carriers side by side, removing pressure and revealing your best options.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation