How to Get Landlord Insurance for Tenant Damage

Tenant damage can wipe out your rental income and leave you facing unexpected repair bills. At Direct Insurance Services, we know that landlord insurance is the financial shield every property owner needs.

This guide walks you through the coverage types available and how to find the right policy for your Utah rental property.

What Landlord Insurance Actually Protects

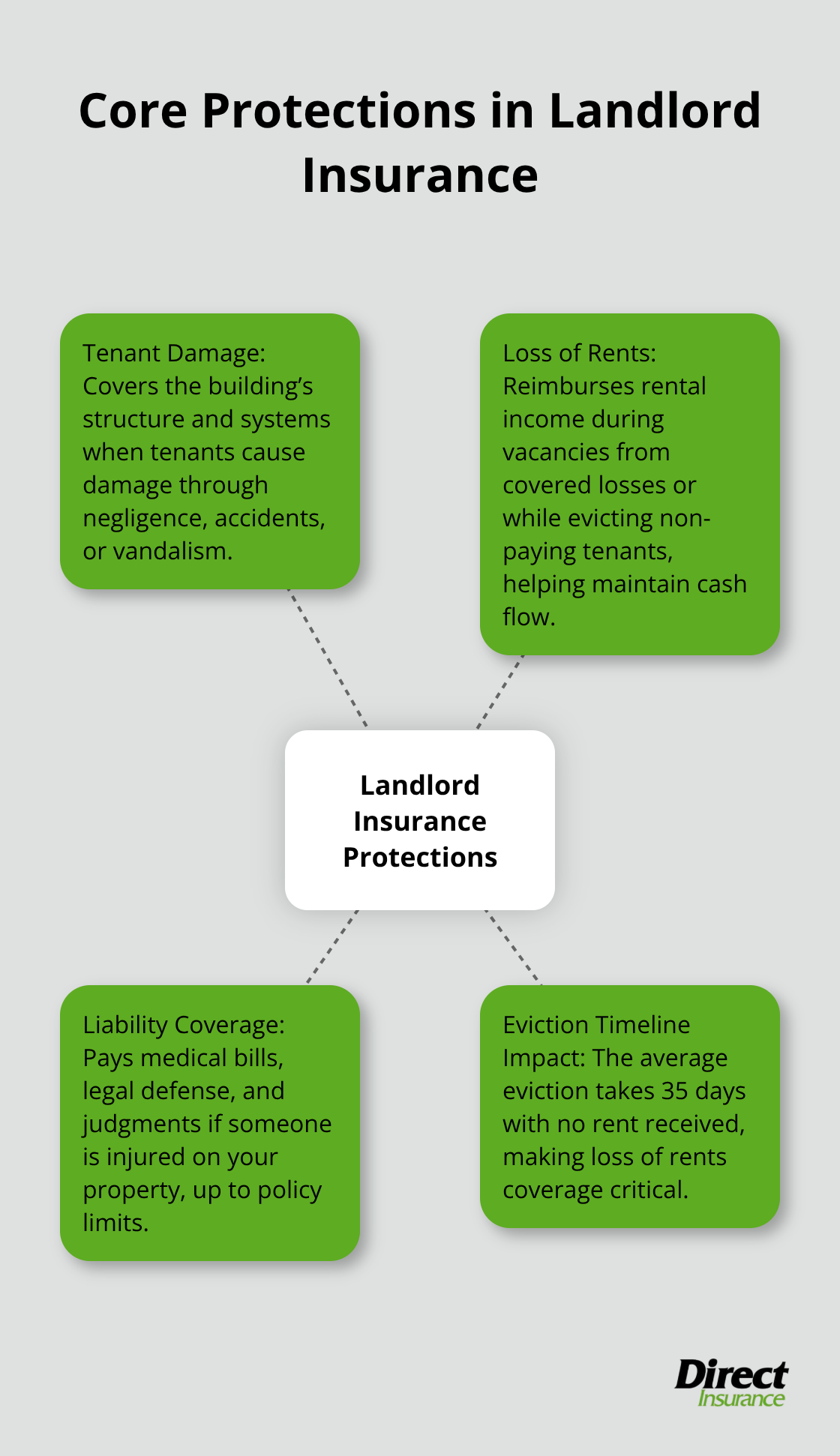

Landlord insurance protects your rental property and income in ways that standard homeowners policies exclude rental properties entirely, leaving you exposed to significant financial risk. When a tenant damages your property-whether through negligence, accidents, or deliberate destruction-your standard homeowners policy won’t pay for repairs. A tenant might punch a hole in drywall, break fixtures, or damage flooring, and you’re left paying thousands out of pocket. Landlord insurance specifically covers these tenant-caused damages to the building structure and systems.

Beyond physical damage, landlord policies protect your rental income when tenants stop paying rent or skip out entirely. According to the National Apartment Association, the average eviction process takes 35 days, during which you receive no rental income while still covering mortgage payments, property taxes, and maintenance costs. Loss of rents coverage reimburses you for this lost income during vacancies or while you evict a non-paying tenant. Additionally, landlord liability insurance covers you if someone is injured on your property and sues you for damages.

If a tenant’s guest slips on your stairs and claims you failed to maintain safe conditions, liability coverage pays their medical bills and legal fees up to your policy limits, protecting your personal assets from being seized to satisfy a judgment.

Why Standard Homeowners Insurance Falls Short

Your homeowners policy covers your primary residence, not income-producing properties. Insurers view rental properties as commercial ventures with higher risk profiles and different coverage needs. If you file a claim on a homeowners policy for tenant damage, the insurer may deny it outright or cancel your coverage for misrepresenting your property use. Landlord insurance is specifically underwritten for the realities of renting-tenant turnover, income loss, and liability exposure from multiple occupants. The distinction matters because coverage gaps can cost you thousands in a single incident.

Protection That Covers Your Real Losses

Landlord policies reimburse actual repair costs for tenant damage, not depreciated value. If a tenant destroys kitchen cabinets worth $3,000, your policy pays to replace them at current market rates. You also receive coverage for lost rent during repairs if damage makes the unit uninhabitable. If a pipe bursts due to tenant negligence and forces you to close the unit for two months while repairs happen, loss of rents coverage compensates you for those two months of income. This is where landlord insurance becomes genuinely valuable-it protects the cash flow that makes your rental business viable.

What Comes Next

Understanding what landlord insurance covers is only half the battle. The real challenge lies in selecting the right coverage types for your specific property and situation.

Coverage Types That Actually Matter

Dwelling Fire Policies Form Your Foundation

Dwelling fire policies cover the physical structure of your rental property against fire, wind, hail, theft, and vandalism. Most lenders require this coverage before funding your mortgage. The dwelling policy pays to repair or rebuild the actual building, not the contents tenants bring inside. If a tenant leaves a stove on and causes a fire that damages the roof and walls, your dwelling policy covers those structural repairs.

You must match your coverage limit to your property’s replacement cost, not its market value. A Utah property worth $400,000 might cost $350,000 to rebuild depending on construction materials and labor. Underestimating this figure leaves you personally liable for the gap.

Liability Insurance Protects You from Injury Claims

Landlord liability insurance protects you when someone gets injured on your property and sues. A tenant’s guest falls down exterior stairs and claims you failed to maintain the treads properly. A delivery person trips on a broken sidewalk. These incidents generate medical bills, legal defense costs, and potential judgments that can reach $100,000 or more.

Liability coverage typically includes $300,000 to $1,000,000 in protection, though higher limits cost only slightly more in premiums. The modest additional expense for increased limits makes sense given the financial exposure from a single serious injury claim.

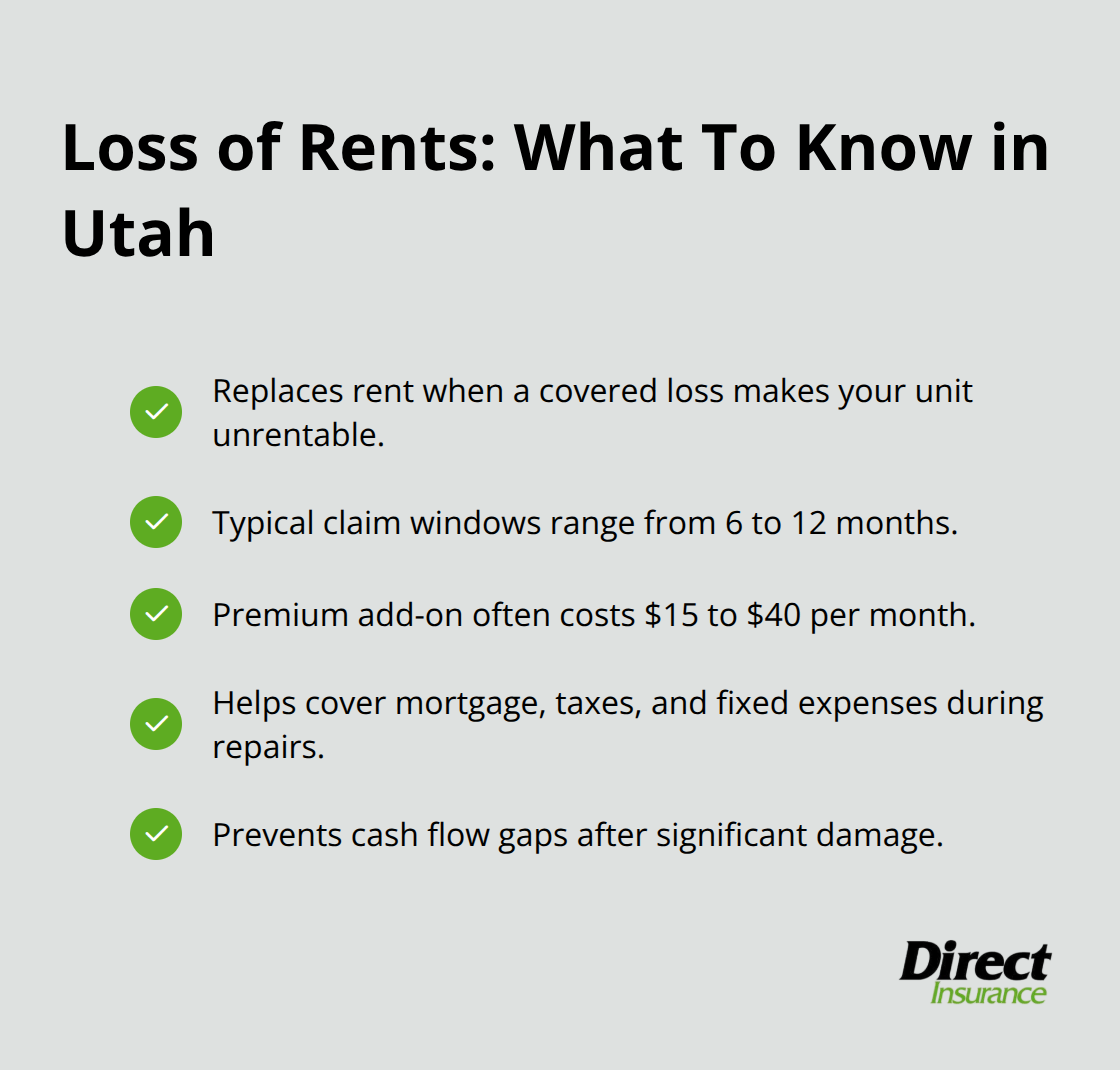

Loss of Rents Coverage Replaces Your Income During Repairs

Loss of rents coverage reimburses your monthly rental income when a covered loss makes the unit unrentable. If a fire damages the kitchen and you need 60 days to complete repairs, this coverage pays 60 days of lost rent while you cannot lease the property. Without it, you absorb that income loss while still paying your mortgage and property taxes.

Utah landlords often underestimate how quickly expenses pile up during vacancy periods. Most policies offer loss of rents coverage for 6 to 12 months of potential claims, which matches typical repair timelines for significant damage. The premium for this add-on costs modestly-usually $15 to $40 monthly depending on your property’s rental value-but the protection prevents financial hardship during extended repairs.

Selecting the Right Mix for Your Situation

The coverage types you select depend on your property’s age, location, and tenant profile. Older properties in areas with higher weather risk need robust dwelling coverage. Properties in neighborhoods with higher foot traffic warrant stronger liability limits. Your next step involves assessing exactly what your specific property requires before comparing quotes from carriers.

How to Get Landlord Insurance in Utah

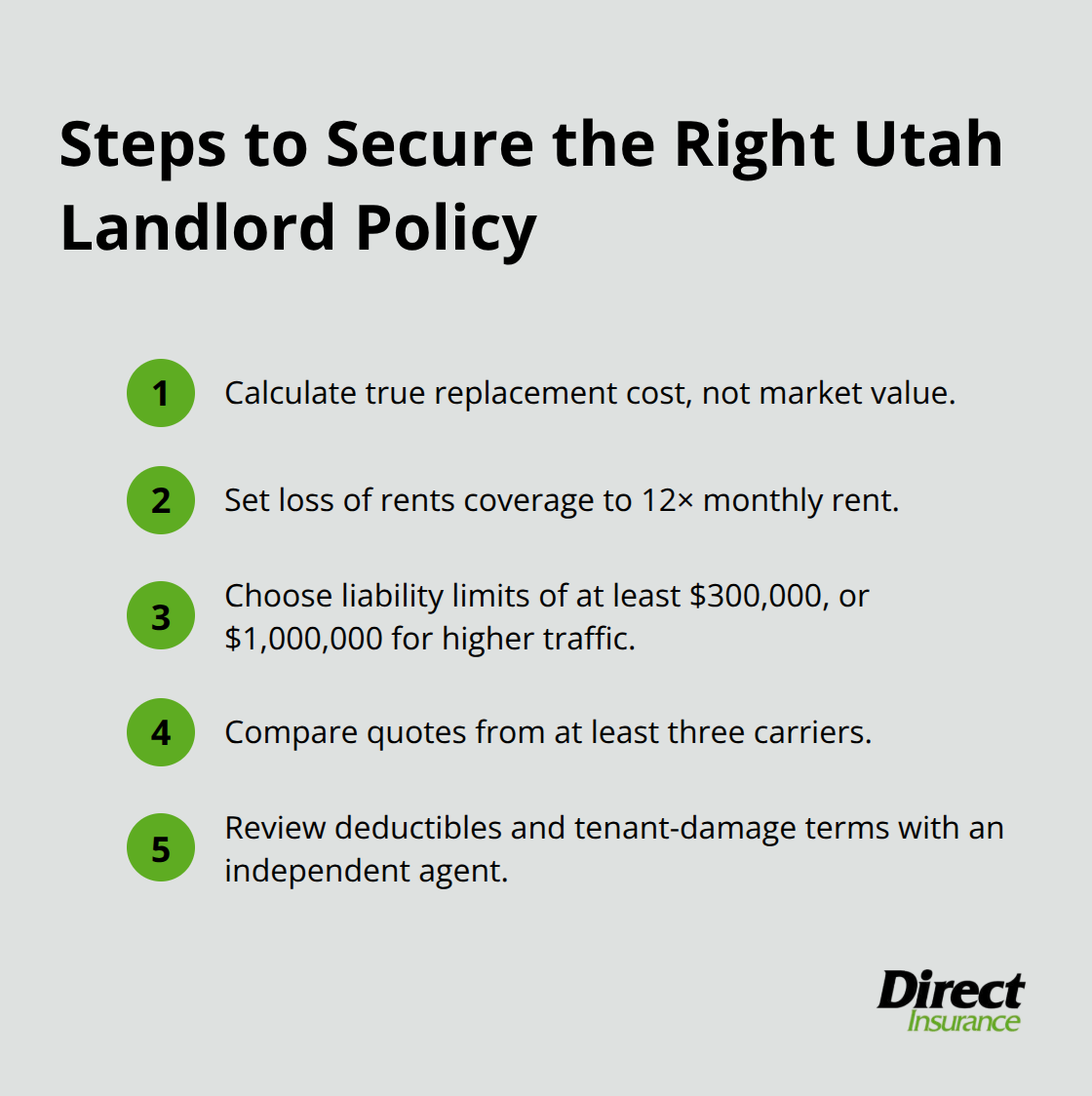

Calculate Your Property’s True Replacement Cost

Start by calculating your property’s replacement cost, not its market value. Contact a local contractor and ask what it would cost to rebuild your rental from the ground up-this number determines your dwelling coverage limit. Utah rental properties typically range from $250,000 to $500,000 in replacement value depending on square footage, construction type, and finishes. Underinsuring by even 10 percent leaves you personally liable for repair costs above your policy limit.

Establish Coverage Amounts Based on Your Income and Risk

Next, document your monthly rental income and multiply it by 12 to establish your loss of rents coverage amount. If your property rents for $1,800 monthly, you need at least $21,600 in annual loss of rents protection. For liability coverage, consider limits of $300,000 as your minimum with $1,000,000 strongly preferred for properties with regular tenant traffic or guest access.

Compare Quotes Across Multiple Carriers

Comparing quotes from multiple carriers reveals substantial premium differences for identical coverage. A property with $350,000 dwelling coverage, $500,000 liability, and 12 months loss of rents coverage might cost $800 annually from one carrier and $1,200 from another-that’s a $400 difference for the same protection. Contact at least three carriers directly rather than relying on online quote tools that often exclude landlord-specific endorsements.

Review Deductibles and Coverage Details

Ask each carrier specifically about their tenant damage deductibles, which typically range from $500 to $2,500 (lower deductibles cost more but reduce your out-of-pocket expense when claims occur). An independent agent can match your specific property profile to the insurer offering the best rates and coverage terms. Independent agents spend time understanding your property’s actual risk factors rather than plugging numbers into a generic algorithm, and that personalized approach consistently delivers better coverage at competitive prices.

Final Thoughts

Landlord insurance for tenant damage protects your rental income and property from financial devastation. The three coverage types we’ve outlined-dwelling fire policies, liability insurance, and loss of rents coverage-work together to address the real risks you face as a property owner. Without this protection, a single incident can drain thousands from your bank account and leave you scrambling to cover mortgage payments while repairs happen.

Calculate your replacement cost accurately, establish coverage limits based on your actual rental income, and compare quotes from multiple carriers to find the best rates. Deductible choices matter too-a lower deductible costs more upfront but saves you money when claims occur, which is worth considering based on your financial situation. An independent insurance agent takes time to understand your specific situation rather than applying generic formulas to your property.

Contact Direct Insurance Services to review your current coverage or get quotes on a new landlord policy. Our team understands the unique risks Utah landlords face and works with top-rated carriers to find coverage that fits your property and budget. Your rental investment deserves protection from someone who actually listens to your needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation