How to Find the Lowest Cost Auto and Home Insurance

Most people overpay for auto and home insurance without realizing it. The difference between the highest and lowest quotes for identical coverage can exceed $1,000 per year, according to insurance industry data.

At Direct Insurance Services, we’ve helped thousands of customers cut their premiums by understanding what actually drives their rates and where savings hide. This guide walks you through the concrete steps to find affordable coverage that doesn’t sacrifice protection.

What Coverage Do You Actually Need?

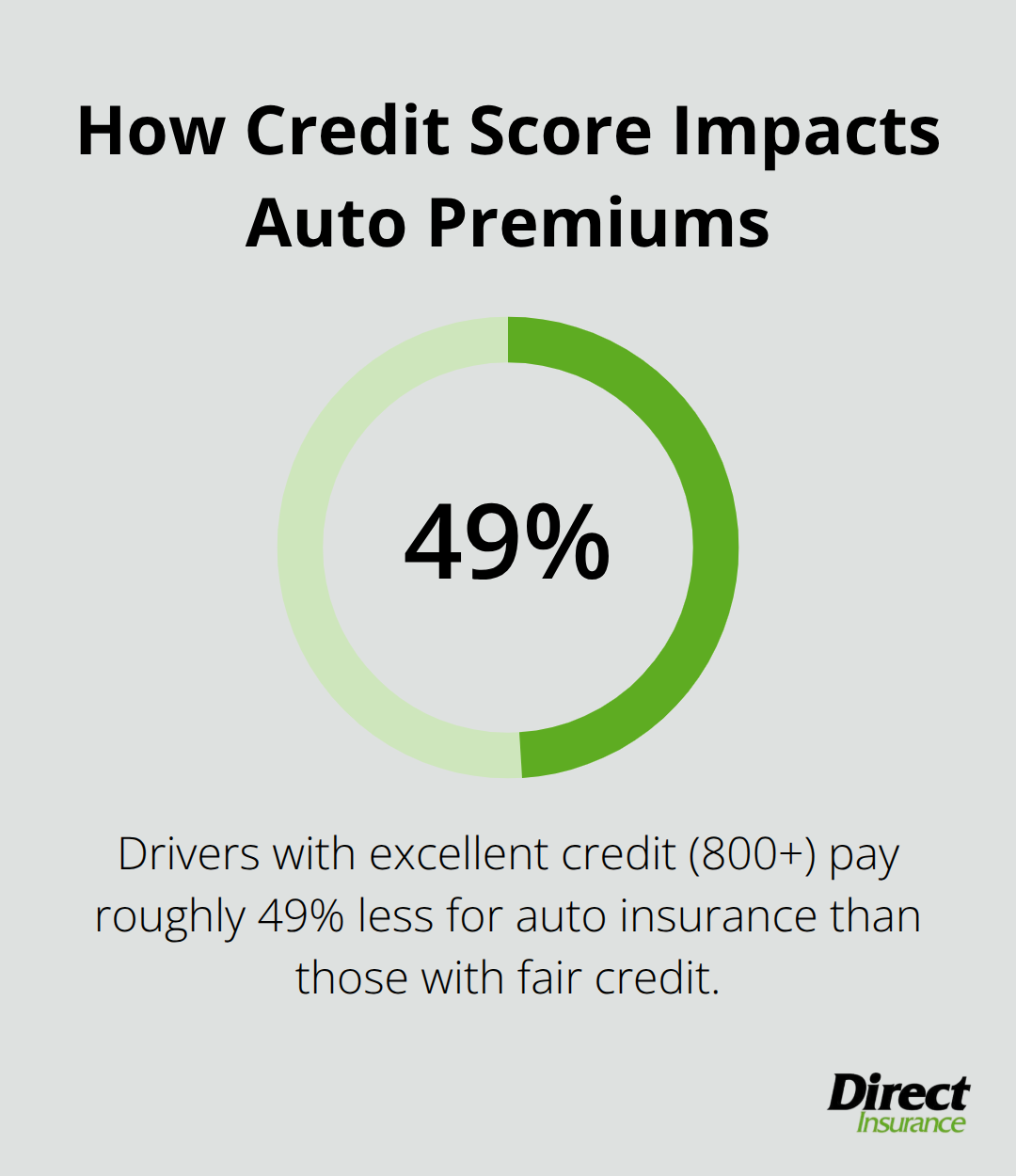

Getting your coverage right starts with honest math, not guesswork. Most people either over-insure and waste money or under-insure and face catastrophic risk. Customers often fail to calculate what their home or car is actually worth, or they don’t understand what your state legally requires. Start by finding your car’s current market value using resources like Kelley Blue Book or NADA Guides. For your home, use your most recent property tax assessment or a recent appraisal as a baseline, then adjust for any renovations or major improvements you’ve made. This number matters because it determines your liability limits and replacement cost coverage. A 2023 Consumer Federation of America study found that Americans with excellent credit (800+) paid roughly 49% less for auto insurance than those with fair credit, but even more dramatic are the differences based on coverage choices. If you’re financing or leasing your vehicle, your lender requires collision and comprehensive coverage-non-negotiable. For homeowners with a mortgage, your lender demands dwelling coverage at least equal to what they’d need to rebuild. The real challenge lies in distinguishing what’s required from what actually makes sense.

Liability Limits Demand Serious Attention

State minimums are genuinely inadequate. Liability limits vary by state, but a single serious accident can generate six-figure medical bills and lost wages. Try carrying at least $100,000 per person and $300,000 per accident-and if you have significant assets, consider $250,000 or $500,000. The premium difference between $50,000 and $100,000 limits is typically $15–$30 per year, making it absurdly cheap insurance against financial ruin. For homeowners, standard liability coverage tops out at $100,000 or $300,000, which sounds substantial until someone is seriously injured on your property. If you own a pool, trampoline, or have frequent visitors, jumping to $500,000 in liability costs almost nothing extra. Optional coverage like umbrella policies starts around $150–$300 annually for $1 million in additional protection, creating a safety net that most people skip despite its low cost.

Collision and Comprehensive: Know When to Drop Them

Collision and comprehensive on older vehicles represent the biggest money-wasters. If your car is worth less than $5,000, collision coverage-which pays to repair your car after an accident-often costs $400–$600 annually. The math is simple: paying $500 per year to protect a $4,000 car means you break even in eight years, and most cars depreciate faster. For vehicles worth under $7,000, dropping collision makes financial sense unless you couldn’t afford to replace the car outright. Comprehensive coverage (theft, weather, vandalism) is cheaper-usually $100–$200 annually-and you should keep it longer since catastrophic losses happen suddenly. On the home side, most standard policies don’t cover flood or earthquake damage, yet these cause billions in annual losses. If you’re in a flood zone or earthquake-prone area, adding these riders costs $500–$1,500 yearly but prevents total loss.

Water Damage and Replacement Cost Coverage

Water damage from burst pipes is covered, but gradual leaks are not-a distinction that matters when a claim arises. Ask specifically about replacement cost versus actual cash value on both your home and personal belongings; replacement cost means the insurer pays what it costs to replace items today, not what you paid ten years ago. This costs 10–15% more but is worth every penny. The coverage choice you make here directly affects how much you’ll actually receive if you file a claim, making it one of the most important decisions in your policy.

Understanding what you truly need sets the foundation for smart shopping. The next step is comparing what different insurers actually charge for the coverage you’ve selected-and that’s where most people find their biggest savings.

Where to Find the Lowest Quotes and Biggest Savings

Compare Quotes from Multiple Insurers

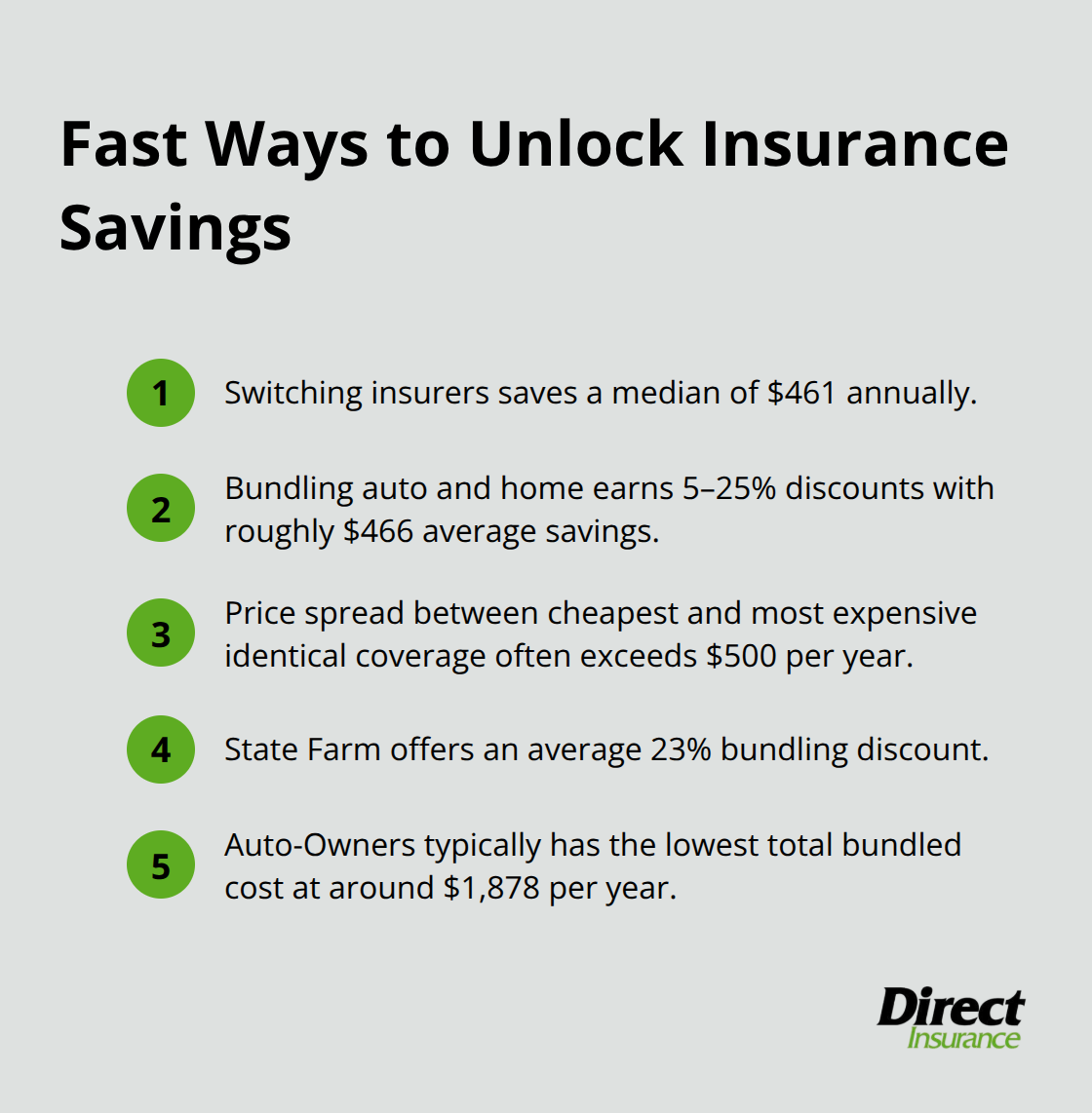

Shopping around for insurance quotes isn’t optional if you want the lowest cost-it’s non-negotiable. A 2024 Consumer Reports survey found that people who switched insurers saved a median of $461 annually, yet most people never request more than one quote. Start by gathering quotes from at least three different insurers using the same coverage levels and deductibles for each one-this is the only way to compare apples to apples. Many insurers offer online quote tools where you enter your ZIP code and basic information, but some require speaking with an agent to get accurate pricing. The time investment pays off dramatically: the difference between the cheapest and most expensive quote for identical coverage regularly exceeds $500 per year.

Request quotes from both national carriers like State Farm and Travelers and regional insurers, since pricing varies wildly based on how each company evaluates risk in your specific area.

Bundle Auto and Home for Substantial Discounts

Bundling your auto and home policies with a single insurer is where serious savings happen. Carriers automatically apply discounts of 5-25% when you combine auto and home insurance policies, translating to roughly $466 in annual savings on average. State Farm offers the largest bundling discount at an average of 23%, while Auto-Owners typically has the lowest total bundled cost at around $1,878 per year. The mechanics of bundling vary by insurer-some apply the discount to both policies equally, while others weight it differently-so always ask how your specific discount gets calculated. One critical detail: if you cancel one policy in a bundle, you often lose the multi-policy discount entirely, which can spike your remaining premium, so factor this into any decision to drop coverage.

Layer On Additional Discounts

Beyond the base bundling discount, you can stack multiple savings opportunities. Safe-driver discounts typically range from 5–15%, while loyalty rewards and paid-in-full discounts add more value. Electronic billing discounts (4–10% depending on the carrier) and automatic payment setup (often 5% savings) require minimal effort but deliver real reductions. Anti-theft devices installed in your vehicle can reduce premiums by 5–20%, depending on the device type and your location. For homeowners, security system installation, roof upgrades, and new construction discounts add up quickly. The key is asking about every possible discount-many insurers don’t volunteer them unless you specifically inquire. These layered discounts transform a modest bundling offer into substantial annual savings.

Understand How Bundling Affects Your Total Cost

The mechanics of how insurers calculate bundling discounts matter more than you might think. Some carriers apply the discount percentage to both policies equally, while others weight the discount toward the more expensive policy. Request a detailed breakdown showing your auto premium, home premium, bundling discount, and final total-this transparency reveals whether bundling actually saves you money compared to separate policies. A few insurers offer single-deductible options when you bundle, meaning if both your home and car suffer damage in the same event, you pay one deductible instead of two. Verify whether your policy includes this perk, as it can provide additional protection value.

Evaluate Bundling Against Separate Policies

Bundling isn’t always the cheapest option, despite its convenience. Compare your bundled quote against the cost of purchasing auto and home policies from different carriers-sometimes splitting your coverage yields lower total premiums. This evaluation becomes especially important if one insurer excels at auto rates while another dominates home pricing in your area. The decision hinges on your specific situation, your location, and the carriers available to you, making quote comparison the only reliable way to determine your best path forward.

What Actually Drives Your Insurance Costs

Your Driving Record and Claims History Control Your Rates

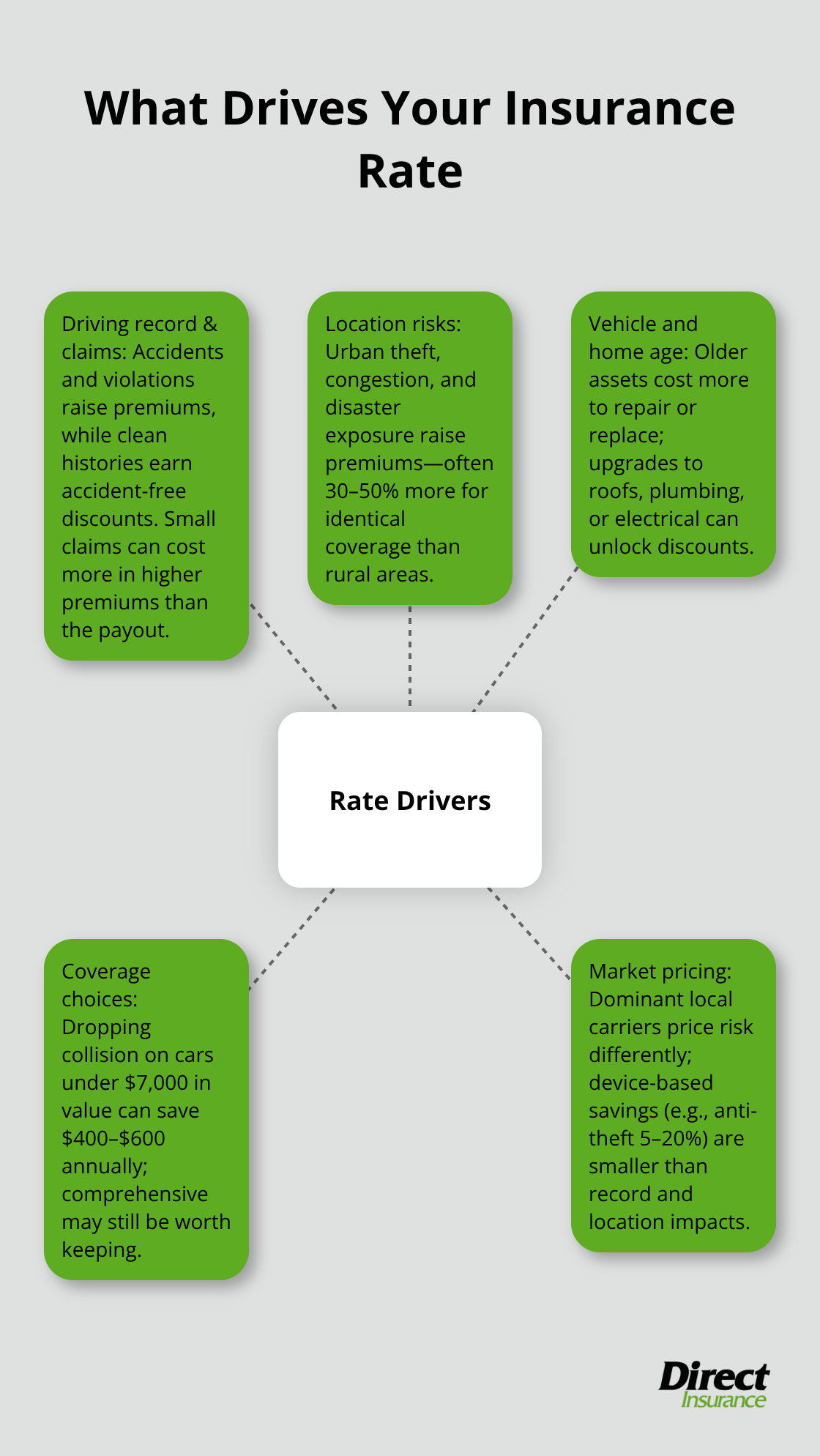

Your driving record and claims history are the two factors that most directly control what you pay. A single accident or moving violation increases your premiums, while maintaining a clean record qualifies you for accident-free discounts that many carriers offer after three to five years without a claim. According to Insurify data, your actual driving behavior matters far more than any gadget you install. If you file a claim for minor damage-say, a $500 fender-bender or small home repair-you often lose more in premium increases than you gain from the payout. The math is brutal: a homeowner with a recent claim pays significantly more than one with a clean history, which is why many people skip claims entirely for small damages and pay out of pocket instead.

Location Creates Risk Calculations Beyond Your Control

Your location determines risk calculations that have nothing to do with your personal driving or home maintenance. Urban areas with higher theft rates, accident frequencies, and natural disaster exposure cost more to insure than rural regions, sometimes by 30–50% for identical coverage. States with severe weather patterns-hurricanes in Florida, hail in Colorado, earthquakes in California-drive home insurance costs substantially higher, while auto insurance rates spike in areas with heavy congestion and poor road conditions.

Vehicle and Home Age Affects Replacement Costs

The age of your vehicle and home matters because older structures cost more to repair and older cars cost more to replace, but depreciation works in your favor eventually. Once your car drops below $5,000–$7,000 in value, dropping collision coverage typically saves $400–$600 annually, and that savings only grows as the vehicle ages. Your home’s age affects both replacement cost estimates and the likelihood of system failures; a 50-year-old roof costs more to insure than a ten-year-old one, but upgrading electrical, plumbing, or roofing systems can qualify you for discounts that offset those increases.

Market Dominance and Local Pricing Variations

The carriers that dominate your state’s market may price vehicles and homes differently based on local repair costs and claim frequency. This variation is why comparing quotes across multiple insurers remains essential regardless of your personal profile. Anti-theft devices reduce premiums by 5–20% depending on the device type and your location, but these savings pale compared to the impact of your driving history and geographic risk factors.

Final Thoughts

Finding the lowest cost auto and home insurance requires three concrete actions: comparing quotes across multiple carriers, bundling your policies strategically, and stacking every available discount. People who shop around save hundreds annually, yet most never request more than one quote. Your driving record and claims history matter far more than any single discount, so maintaining a clean record pays dividends for years.

Start by gathering quotes from at least three different insurers using identical coverage levels and deductibles. Request bundling quotes alongside separate policy options to determine which approach actually saves you money in your specific situation. Ask about every discount available-safe-driver credits, electronic billing, automatic payments, security systems, and anti-theft devices all compound into meaningful savings.

An independent agent transforms this process from overwhelming to manageable. Unlike captive agents who represent a single carrier, independent agents access multiple insurers and compare quotes on your behalf, saving you hours of research. At Direct Insurance Services, our team helps Utah families and businesses find affordable protection that actually covers what matters.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation