How Much Is Homeowners Insurance?

Homeowners insurance costs vary dramatically depending on where you live, your home’s characteristics, and the coverage you select. Most homeowners pay between $1,200 and $2,500 annually, but your actual premium could be significantly higher or lower.

At Direct Insurance Services, we help Utah homeowners understand what influences their rates and find ways to reduce their premiums. This guide breaks down the factors affecting your costs and shows you practical steps to save money.

What Drives Your Homeowners Insurance Price

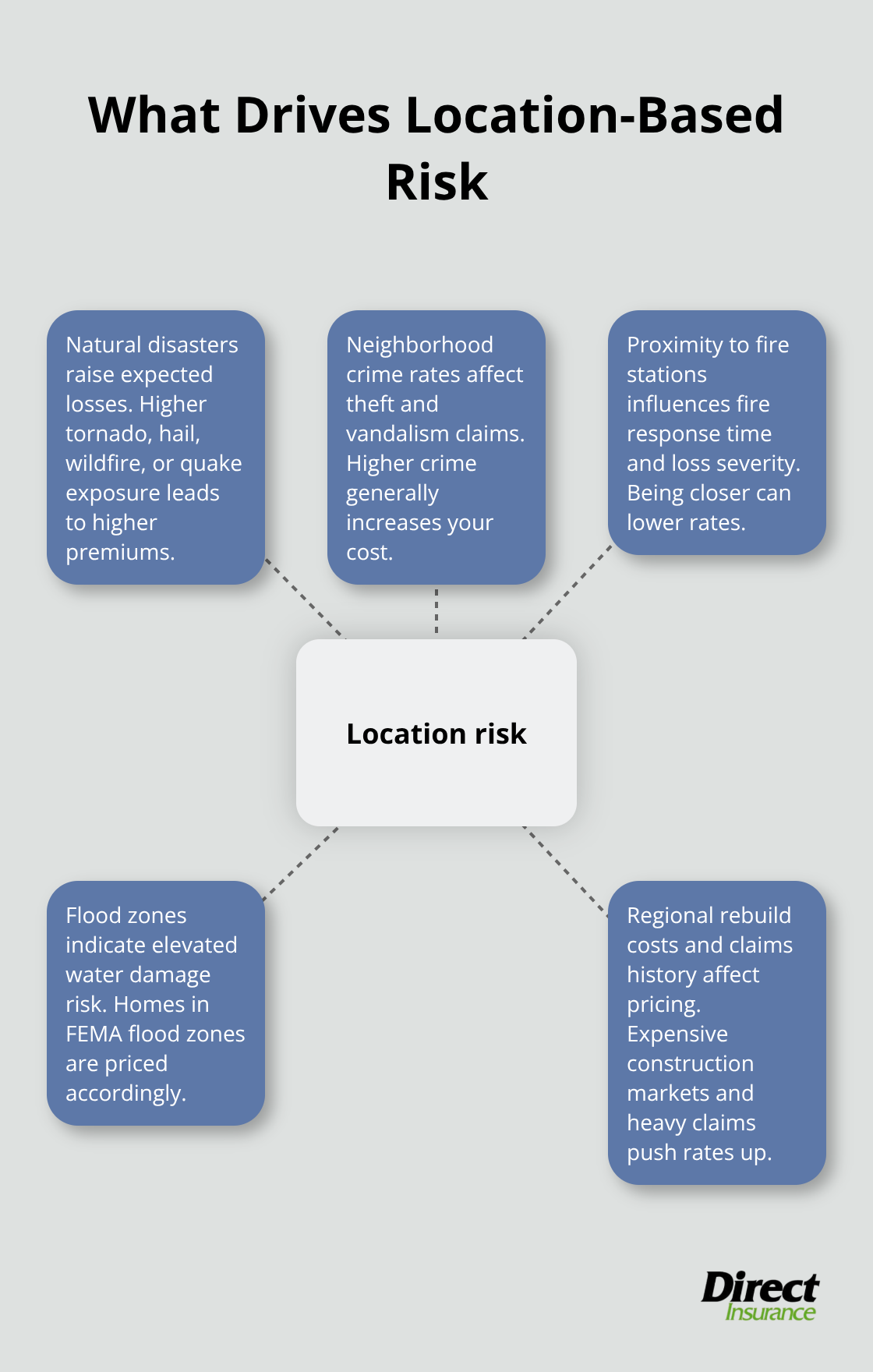

Location and Natural Disaster Risk

Your homeowners insurance premium depends on three primary factors that insurers evaluate before quoting you a rate. Location matters most because it determines your exposure to natural disasters, crime, and local construction costs. A home in Oklahoma City costs about $5,554 annually for $300,000 in dwelling coverage, while the same coverage in Portland, Oregon costs around $1,051, according to Bankrate’s analysis of Quadrant Information Services data. This massive difference reflects Oklahoma’s higher tornado and hail risk, elevated rebuilding costs, and regional claims history.

Natural disaster frequency directly impacts what insurers charge. NOAA reported over 25 billion-dollar weather and climate disasters in 2024 alone, forcing carriers to price in substantially higher risk for vulnerable regions. Your proximity to fire stations, local crime rates, and whether your area sits in a flood zone all influence your quote. If your home sits in a high-risk area, you’ll pay more regardless of how well-maintained your property is.

Home Age and Construction Materials

Home age and construction type significantly affect your premium because they correlate with repair and rebuild costs. A 1959-built home averages $3,285 annually for $300,000 coverage, while a 2020-built home averages $2,182, according to Bankrate data. Older homes cost more to insure because they typically use outdated materials, have aging electrical systems, and carry higher fire risk.

Brick construction costs less to insure than wood-frame because brick resists fire better. Your home’s materials and condition directly influence how much insurers charge you at renewal time.

Coverage Limits, Deductibles, and Credit History

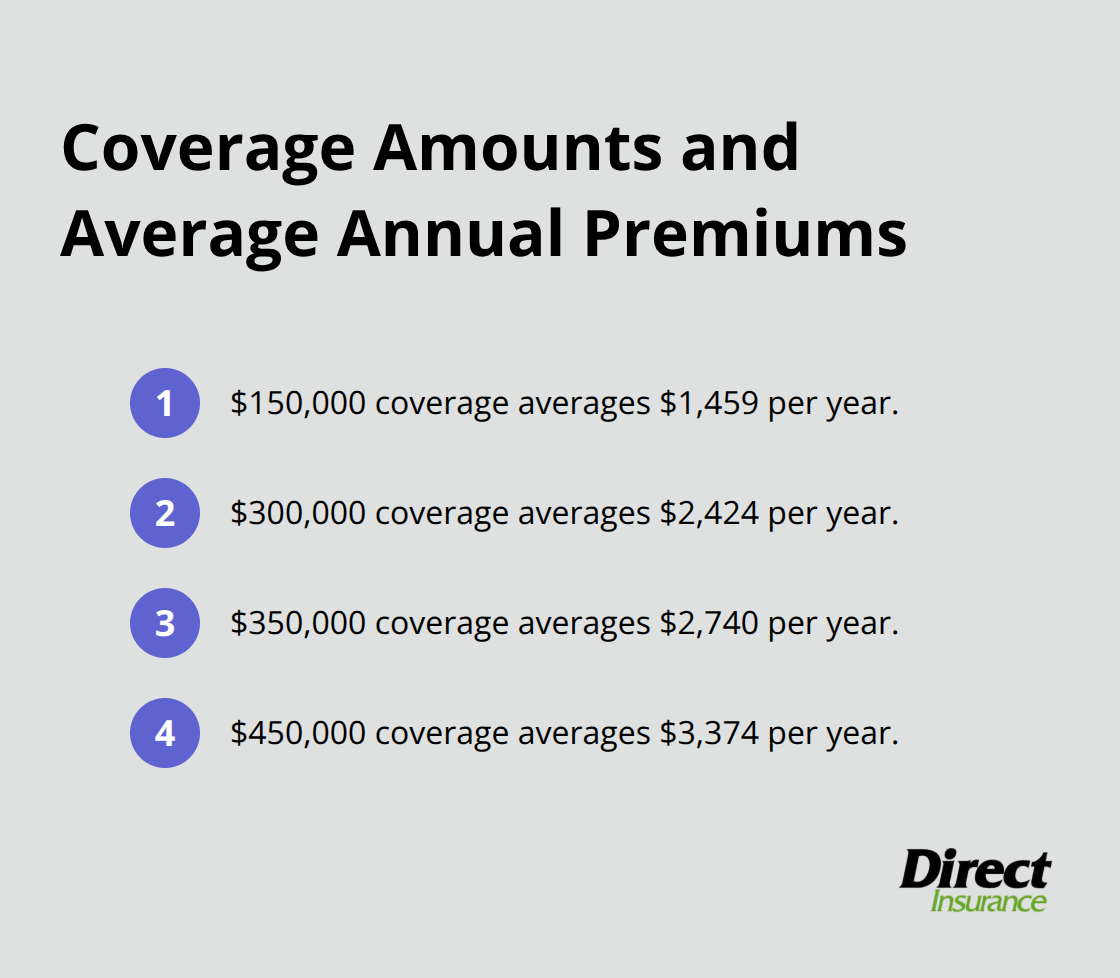

Your chosen coverage limits and deductible directly control your monthly payment. Raising your deductible from $1,000 to $2,500 reduces premiums by roughly 12% on average, but you’ll pay that full amount out of pocket if you file a claim. The dwelling coverage amount you select creates a clear cost ladder: $150,000 coverage averages $1,459 annually, $300,000 averages $2,424, and $450,000 averages $3,374.

Credit history also plays a role in many states. Good credit typically results in premiums around $2,424 for $300,000 coverage, while poor credit can push that to $5,122 (California, Hawaii, Maryland, and Massachusetts restrict or ban credit-based pricing). These factors work together to determine your rate, which is why two homes on the same street can have vastly different premiums. Understanding what influences your specific quote helps you identify which costs you can control and which ones depend on your location and home characteristics.

Average Homeowners Insurance Costs in Utah

Utah homeowners pay significantly less for insurance than residents in high-risk states, but more than those in the cheapest regions nationally. The national average for $300,000 in dwelling coverage sits at $2,424 annually according to Bankrate’s analysis of Quadrant Information Services data, which translates to roughly $202 per month. Utah’s rates fall below this national average, positioning the state as a moderate-cost region for homeowners insurance. This advantage stems from Utah’s relatively lower frequency of catastrophic weather events compared to tornado-prone Oklahoma or hurricane-vulnerable Florida, though your specific Utah city matters enormously. Salt Lake City and Provo residents typically pay less than those in rural areas prone to wildfires or homes in flood-prone valleys.

The Most and Least Expensive States

The five most expensive states nationally-Nebraska at $6,587, Louisiana at $6,274, Florida at $5,838, Oklahoma at $4,695, and Kansas at $4,444-all face elevated disaster risk that drives premiums far above Utah’s typical range. The five cheapest states-Vermont at $827, Delaware at $966, Alaska at $1,035, New Hampshire at $1,039, and West Virginia at $1,047-benefit from lower rebuilding costs and fewer high-cost weather events, making Utah’s middle-ground positioning realistic for budget planning.

How Coverage Amounts Shape Your Utah Bill

Your dwelling coverage selection creates the most direct impact on your Utah premium. A $150,000 coverage limit averages $1,459 annually, $300,000 averages $2,424, $350,000 averages $2,740, and $450,000 averages $3,374 based on Bankrate data. Utah homeowners often select $300,000 to $400,000 in dwelling coverage depending on neighborhood values and rebuild costs, which lands most policies in the $2,200 to $2,700 annual range.

Deductible Choices Lower Your Annual Cost

Your deductible choice adjusts this base amount significantly. A $1,500 deductible costs roughly $2,366 annually for $300,000 coverage, while a $2,000 deductible drops to $2,212, and a $5,000 deductible falls to $1,989. This means selecting a higher deductible can save you $400 or more yearly, but only if you maintain an emergency fund to cover that out-of-pocket amount after a claim.

Utah Compared to Neighboring States

Utah’s neighboring states show the value of your location within the region. Idaho and Wyoming typically cost less than Utah due to lower population density and fewer urban construction costs, while Colorado sits slightly higher due to mountain-area wildfire exposure. Wyoming averages around $1,800 to $2,100 for comparable coverage, making it one of the cheapest neighbors, while Colorado averages $2,300 to $2,600 depending on whether your home sits in wildfire zones near the Front Range or in safer mountain valleys. These regional differences highlight how your exact location within Utah-and how it compares to surrounding states-directly influences what you’ll pay each year.

How to Reduce Your Homeowners Insurance Premiums

Consolidate Policies for Immediate Savings

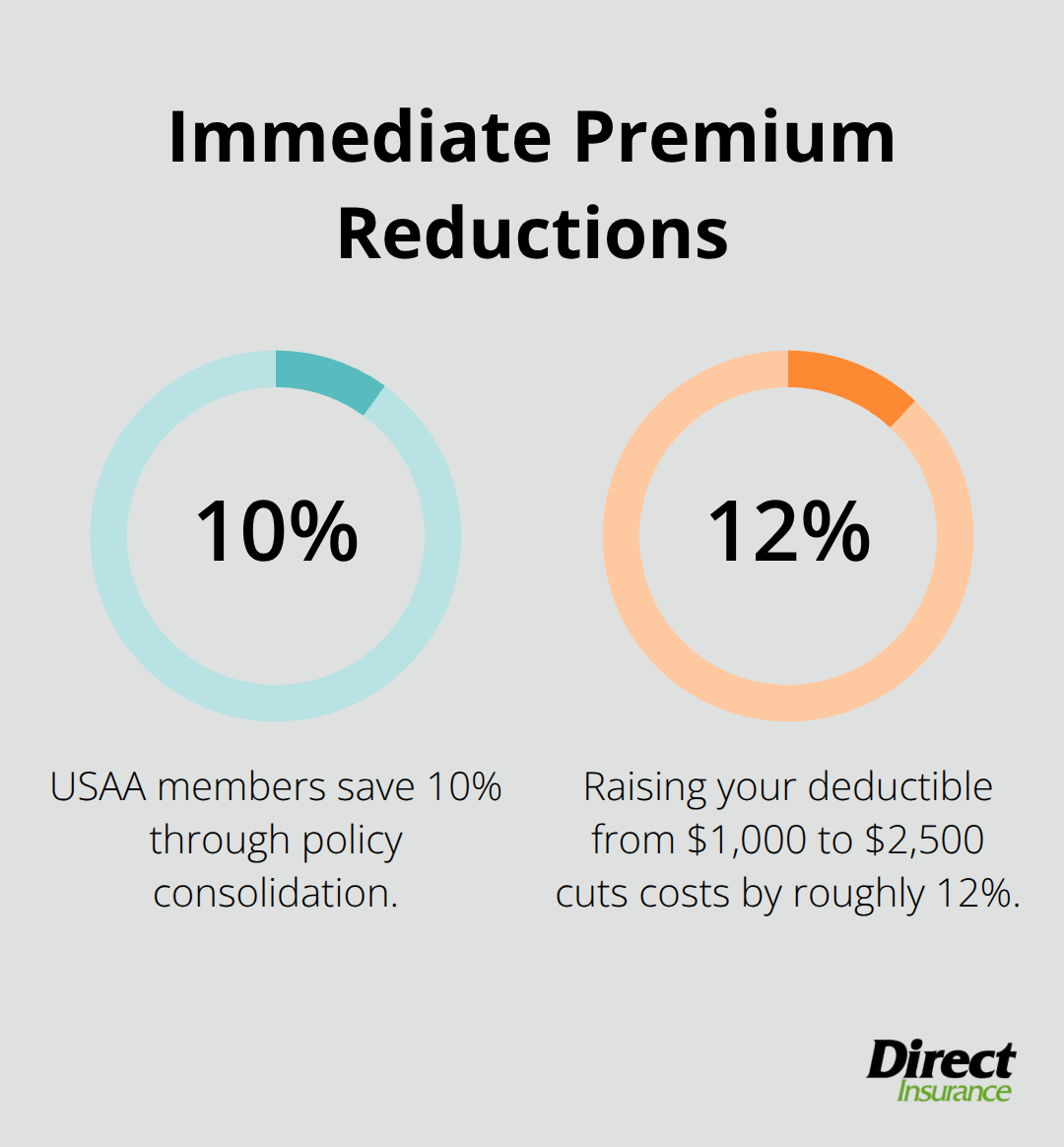

Consolidating your homeowners policy with auto insurance through the same carrier delivers immediate savings without requiring any home improvements or lifestyle changes. USAA members save 10% through consolidation, while Auto-Owners, Nationwide, Allstate, and State Farm all offer multi-policy discounts that typically range from 5% to 15%. For a Utah homeowner paying $2,400 annually for homeowners coverage, a 10% consolidation discount saves $240 per year with zero effort. The math is straightforward: if you currently split auto and home insurance between different companies, moving them to one carrier generates tangible savings instantly.

Many insurers also offer additional discounts when you pay your annual premium upfront rather than monthly installments, which can save another 2% to 5% depending on the carrier. This means consolidation plus annual payment could reduce your bill by $300 to $400 yearly without touching your coverage limits or deductible.

Install Home Security Systems and Safety Features

Insurers reduce premiums for homes with deadbolts, smoke alarms, fire extinguishers, and security systems because these features demonstrably lower claims frequency. Property owners who install security systems, smoke detectors, and central monitoring systems can reduce premiums by 10% to 20%, which translates to $120 to $240 annually on a $2,400 policy. The system pays for itself within two to four years purely through insurance savings, making it one of the few home improvements that directly and immediately lowers your costs. Storm shutters or hurricane-resistant laminated glass on exterior openings also qualify for discounts in most states, though Utah homeowners benefit less from this since the state faces lower hurricane risk. More valuable for Utah are roof upgrades using impact-resistant materials or electrical system updates, both of which reduce fire and weather-related claims risk. After you complete any qualifying home improvement, contact your insurer directly to confirm the discount applies at your next renewal, as many homeowners miss savings simply because they fail to notify their carrier of improvements.

Improve Your Credit Score for Long-Term Savings

Your credit history directly influences your premium in most states, with home insurance for bad credit typically coming with much higher rates. Unlike location or home age, credit sits entirely within your control. Paying all bills on time, reducing credit card balances, and checking your credit report for errors takes effort but produces measurable results. Insurers typically review credit information every three years at renewal, meaning credit improvements made today can generate lower rates at your next policy anniversary. If you dispute and correct errors on your credit report, inform your insurer immediately since corrections may entitle you to a refund or premium reduction retroactively. For Utah homeowners, this represents one of the few cost-reduction strategies that compounds over time-as your credit improves, your savings increase at every renewal period without requiring any additional actions.

Final Thoughts

Your homeowners insurance cost reflects location, home characteristics, and choices you control like deductible and credit history. Utah homeowners typically pay between $2,000 and $2,600 annually for $300,000 in dwelling coverage, positioning the state as a moderate-cost region compared to disaster-prone states like Oklahoma and Florida. Understanding what drives your specific premium helps you identify realistic savings opportunities without overpaying for coverage you don’t need.

The most effective ways to lower your bill require minimal effort and produce immediate results. Consolidating your homeowners and auto policies with one carrier saves 5% to 15% right away, while installing security systems and smoke detectors can reduce premiums by 10% to 20%. Improving your credit score takes longer but produces lasting savings at every renewal period, and raising your deductible from $1,000 to $2,500 cuts costs by roughly 12% if you maintain emergency savings to cover that amount after a claim.

Getting an accurate quote requires comparing coverage options across multiple insurers to determine how much is homeowners insurance in your specific situation. Determine your home’s replacement cost value, decide on dwelling coverage limits that match your rebuild needs, and select a deductible that fits your budget and risk tolerance (shopping around reveals significant rate differences between carriers). Contact Direct Insurance Services to get personalized quotes and discover how much you can save on your Utah homeowners policy.