What Does Homeowners Insurance Cover?

Most homeowners don’t know exactly what their insurance covers until they need to file a claim. That’s when gaps in coverage become painfully obvious.

We at Direct Insurance Services want to change that. This guide breaks down the main coverage types in a homeowners policy so you understand what’s actually protected and where you might have blind spots.

What Your Dwelling Coverage Actually Protects

The Foundation of Your Homeowners Policy

Your dwelling coverage forms the backbone of your homeowners insurance, protecting far more than most people realize. This coverage pays to repair or rebuild the main structure of your home after a covered loss like fire, storms, or vandalism. According to the Insurance Information Institute, dwelling coverage should reflect your home’s current rebuilding costs, not its market value-a distinction many homeowners miss. If your home would cost $400,000 to rebuild today but is worth $500,000 on the market, your dwelling coverage limit should be closer to $400,000. The National Association of Insurance Commissioners recommends updating this estimate every few years, especially after renovations or major construction projects in your area.

Coverage That Extends Beyond Your Main Walls

Your coverage also extends to attached structures like garages, decks, and carports, which fall under the same dwelling protection. These additions matter because damage to a detached garage or deck can add up quickly. Most homeowners underestimate how much these structures contribute to their total replacement cost, so reviewing your dwelling limit with these features in mind helps prevent coverage shortfalls.

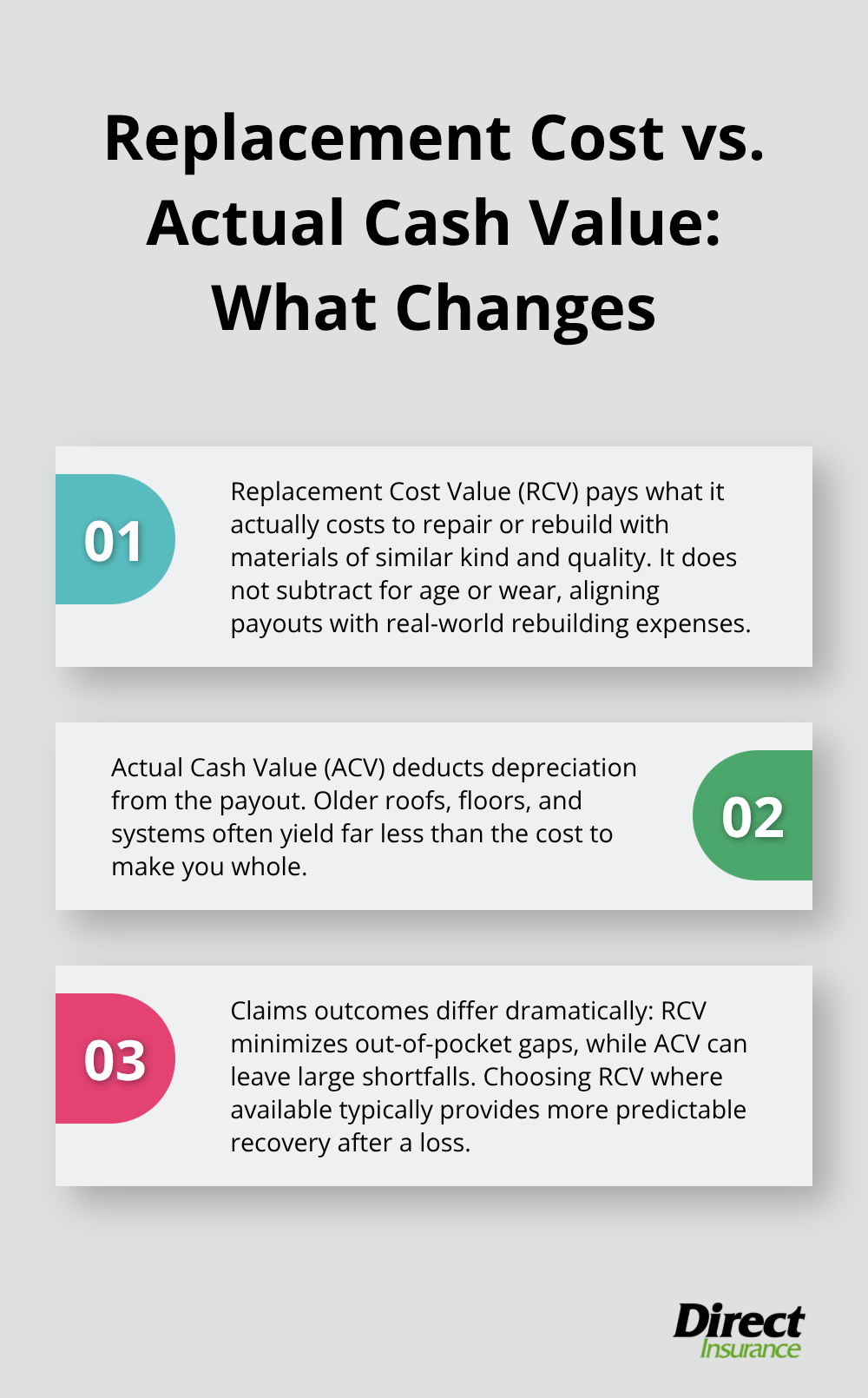

Replacement Cost Value vs. Actual Cash Value

The choice between replacement cost value and actual cash value fundamentally changes what you’ll receive after a claim. Replacement cost value pays what it actually costs to repair or rebuild using materials of similar quality, without subtracting for age or wear. Actual cash value pays the cost to repair or replace your home or personal property based on its value, which often leaves a significant gap between what you owe and what you receive.

Consider a roof damaged by hail: under replacement cost value, you’d receive the full cost minus your deductible; under actual cash value, that same roof might pay only a portion after depreciation is factored in. Most insurers now offer replacement cost value for dwelling coverage because it better reflects real rebuilding expenses, but some policies still use actual cash value. When reviewing your policy or getting a quote, ask explicitly whether you’re getting replacement cost or actual cash value (this single decision could mean tens of thousands of dollars in out-of-pocket costs after a loss).

What Comes Next in Your Coverage Picture

Understanding what your dwelling coverage protects sets the stage for evaluating your personal property coverage, which handles the belongings inside your home and how much protection they actually receive.

What Your Personal Property Coverage Actually Covers

Your personal property coverage protects the belongings inside your home-furniture, electronics, clothing, kitchen appliances-after covered losses like fire, theft, or storms. According to the Insurance Information Institute, personal property coverage typically runs 50 to 70 percent of your dwelling limit. If your home has $300,000 in dwelling coverage, you’d likely receive $150,000 to $210,000 for personal belongings. That sounds reasonable until you start inventorying what you actually own. Most homeowners are shocked to discover their belongings exceed this automatic limit.

Create a Home Inventory Before You Need It

The National Association of Insurance Commissioners recommends creating a detailed home inventory with photos, receipts, and serial numbers before a loss occurs. This inventory becomes invaluable when you file a claim because it proves what you owned and its condition. Without documentation, insurers have no way to verify your losses, and you’ll struggle to recover what you’re entitled to. Start in one room, photograph items, note purchase dates and prices, and store the list somewhere safe outside your home-a cloud drive works perfectly. This single step prevents massive underpayment after a loss.

Why High-Value Items Need Special Treatment

Standard personal property coverage includes sub-limits on specific categories. Jewelry typically caps at $1,500 to $2,500, electronics at similar ranges, and collectibles even lower. If you own engagement rings, watches, art, or antiques worth more than these limits, you’re underinsured. The solution is a scheduled property endorsement, which lists valuable items individually with their appraised values and covers them up to their full worth without depreciation. This costs more than standard coverage but protects what matters most.

Get Appraisals for Items Over $5,000

Appraisals from jewelers, art specialists, and antique experts provide the written documentation insurers require. Without an appraisal, you’re relying on your word about an item’s value, and claims adjusters often dispute inflated estimates. The deductible also applies differently to scheduled items. While your standard deductible might be $1,000, scheduled property often carries a lower deductible or sometimes none at all, making claims more straightforward when damage occurs.

Off-Property Coverage for Valuables You Travel With

If you travel frequently or keep valuable belongings outside your home, off-property coverage extends personal property protection to about 10 percent of your limit worldwide. High-value items still face sub-limits even off-property, so the scheduled endorsement remains essential for comprehensive protection. Understanding what your personal property coverage actually covers-and where the gaps exist-sets the stage for evaluating your liability protection, which handles injuries that occur on your property and the legal costs that follow.

Liability Coverage and Additional Living Expenses

When a Guest Gets Hurt on Your Property

Liability coverage protects you when someone is injured on your property and holds you responsible. The Insurance Information Institute reports that the five-year average cost of a home insurance liability claim reaches about $31,960, which explains why this protection matters far more than most homeowners realize. Standard liability coverage typically starts at $100,000, though this limit often falls short for serious injuries. If a guest slips on your icy walkway and requires surgery, medical bills alone can exceed $50,000 within weeks.

Your $100,000 limit covers the medical expenses, but once legal fees and settlements enter the picture, that protection erodes quickly. Higher liability limits cost surprisingly little to add-raising your coverage to $300,000 or $500,000 typically adds only $15 to $30 annually to your premium. If you own significant assets, an umbrella policy extending your liability protection to $1 million or higher becomes a practical necessity rather than an optional upgrade.

Medical Payments Coverage Works Independently

Medical payments to others coverage operates separately from liability and covers minor injuries regardless of fault. This coverage typically pays up to $1,000 to $5,000 per person for medical expenses when someone is injured on your property, even if you bear no legal responsibility. A neighbor’s child hits their head in your pool, or a delivery driver slips on your steps-medical payments coverage handles these bills without requiring a liability claim. This distinction matters because using medical payments coverage doesn’t trigger a claim history that could affect your renewal rates.

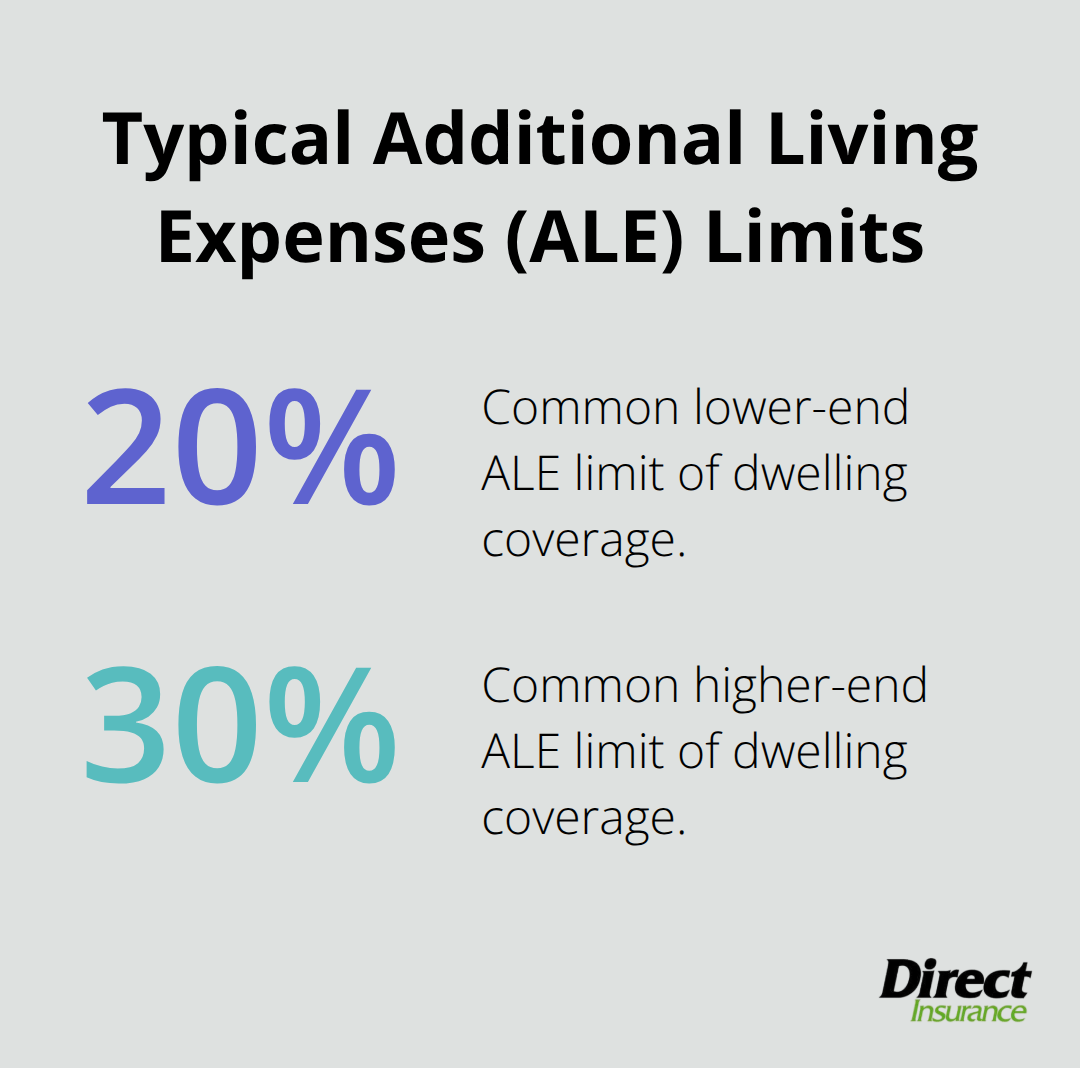

Additional Living Expenses When Your Home Becomes Uninhabitable

Additional living expenses coverage addresses what happens when your home becomes uninhabitable after a covered loss. If a fire damages your kitchen and bedroom, making the house unlivable for three months while repairs proceed, this coverage pays for temporary housing, meals at restaurants, pet boarding, and laundry services. The Insurance Information Institute notes this coverage typically provides 20 to 30 percent of your dwelling limit, so a $300,000 home might receive $60,000 to $90,000 in additional living expenses protection.

Local Costs Dramatically Affect Your Coverage Adequacy

Actual payouts depend on your area’s hotel rates and living costs, which vary dramatically. A family displaced in rural Wyoming faces lower temporary housing costs than one in Salt Lake City, yet the coverage limit remains the same. Many homeowners discover after a loss that their additional living expenses limit exhausted within weeks, leaving them responsible for months of housing costs. Reviewing this limit against your local rental market prevents this gap.

Final Thoughts

Your homeowners policy protects far more than most people realize, but only if you understand what’s actually covered and where the gaps exist. Dwelling coverage rebuilds your home’s structure and attached features, personal property coverage protects your belongings (though standard limits often fall short for valuable items), and liability coverage shields you from lawsuits when someone gets injured on your property. Floods and earthquakes aren’t covered by standard policies, mold from long-term leaks falls outside protection, and your additional living expenses limit may exhaust within weeks in high-cost areas.

Most homeowners discover too late that what does homeowners insurance cover doesn’t match their actual needs. Your personal property limit might not reflect what you own, high-value items face sub-limits far below their worth, or your liability protection falls short of your assets. These gaps aren’t minor oversights-they’re the difference between recovering fully after a loss and facing significant out-of-pocket costs that strain your finances.

The only way to know where your protection actually stands is to review your policy carefully or have someone walk through it with you. We at Direct Insurance Services help Utah families understand their coverage, identify gaps, and adjust limits to match their real needs. Contact us to review your current policy or get a quote that reflects what you actually need to protect.