Understanding Your Auto Insurance Deductible

Your auto insurance deductible directly affects both your premium costs and out-of-pocket expenses when filing a claim. Most drivers don’t fully understand how this financial component works until they need to use their coverage.

At Direct Insurance Services, we see clients struggle with deductible decisions that can cost them hundreds or thousands of dollars. This guide breaks down everything you need to know about choosing and managing your deductible effectively.

What Exactly Is an Auto Insurance Deductible

The Financial Mechanism Behind Your Coverage

An auto insurance deductible represents the specific dollar amount you pay out-of-pocket before your insurance company covers the remaining costs of a covered claim. The Insurance Information Institute reports that most drivers select a $500 deductible, though options typically range from $100 to $2,000. When you file a claim for $3,000 in damages with a $500 deductible, your insurer pays $2,500 while you handle the $500 portion directly.

Coverage Types That Include Deductibles

Deductibles apply exclusively to collision, comprehensive, uninsured motorist, and personal injury protection coverages. Liability coverage never includes a deductible since it pays for damages you cause to others. This distinction matters because many drivers mistakenly believe all coverage types require deductible payments. State Farm data shows that comprehensive claims average $1,621, while collision claims average $4,711 (making your deductible choice particularly significant for these coverage types).

The Claims Payment Process

You pay your deductible after your claim receives approval and processing, not upfront when you file. If your claim receives approval for $5,000 with a $250 deductible, your insurance company issues a check for $4,750. The deductible amount gets subtracted from the total payout. However, if repair costs fall below your deductible amount, you pay all expenses yourself since the claim doesn’t meet the threshold for insurance coverage activation.

How Deductible Amounts Affect Your Premiums

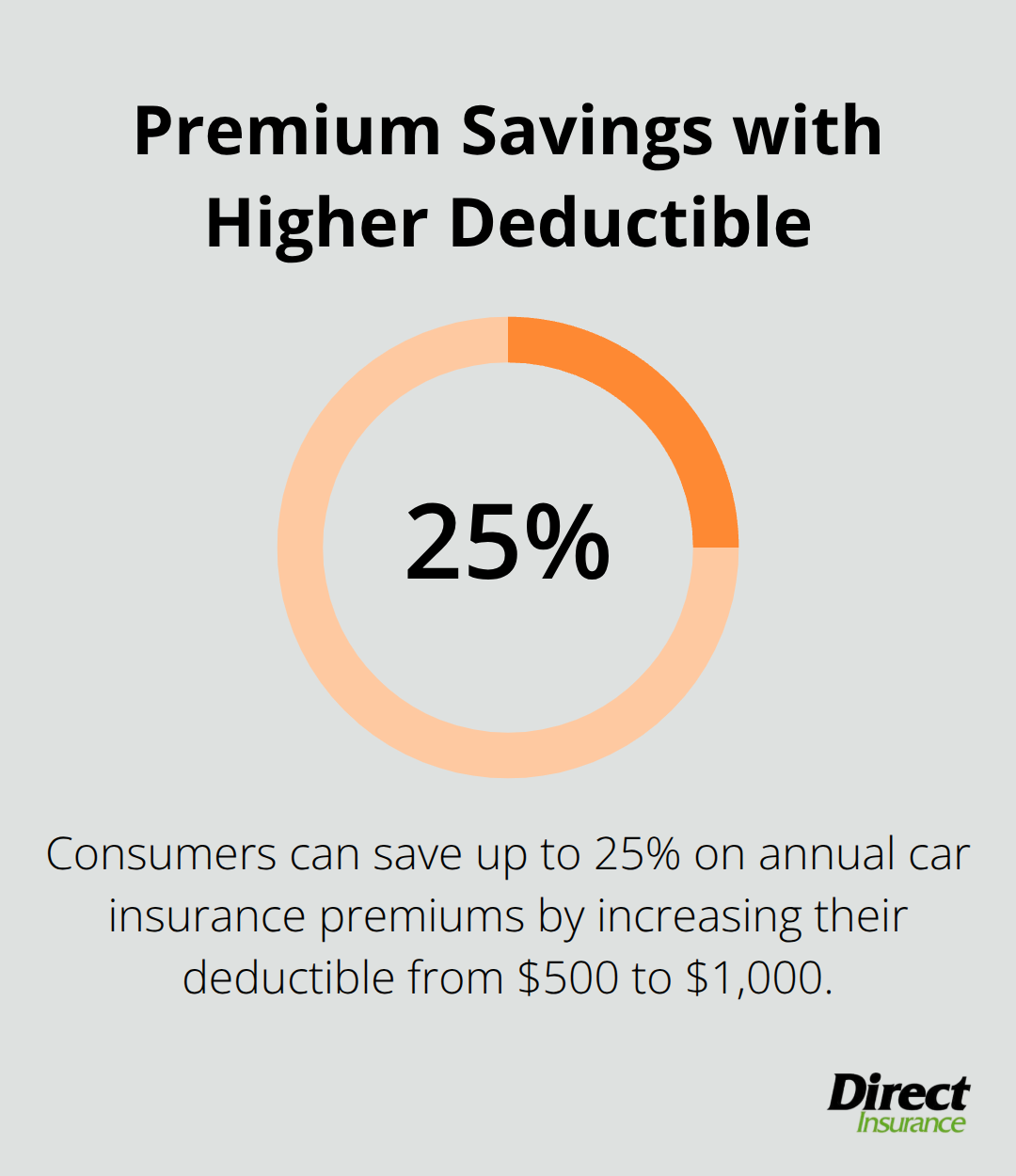

Higher deductibles directly reduce your monthly premiums while lower deductibles increase them. Consumers who raise their deductible from $500 to $1,000 typically save 20-25% on their car insurance premiums annually. This trade-off means you accept more financial responsibility during claims in exchange for lower ongoing costs. The decision becomes particularly important when you consider that drivers with clean records may go years without filing claims (making higher deductibles more attractive for long-term savings).

How Much Should Your Deductible Be

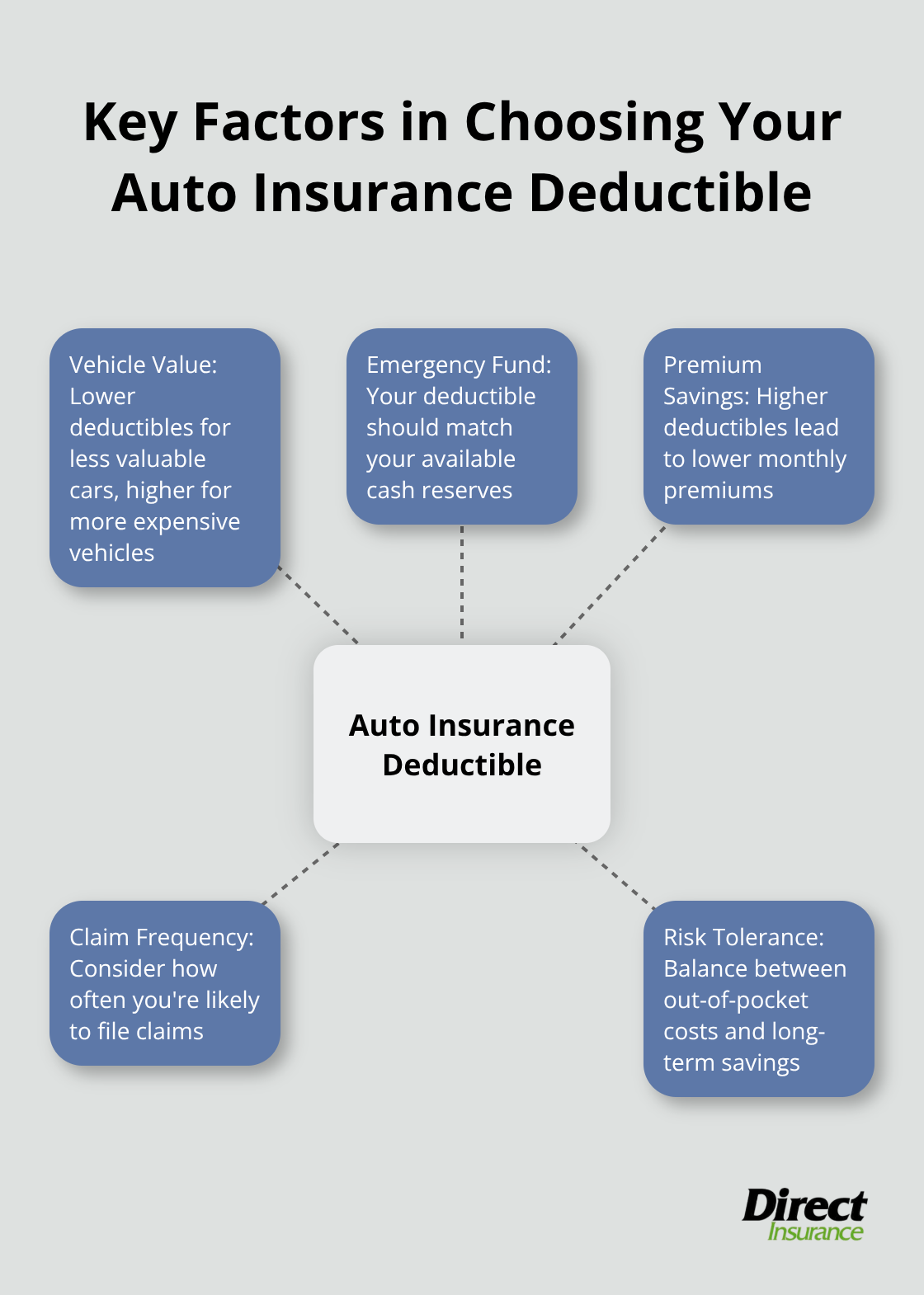

Your Vehicle Value Determines Your Strategy

Vehicle value should drive your deductible decision more than any other factor. If your car is worth $5,000 or less, choose a $250 or $500 deductible to avoid payment of a large percentage of your vehicle’s value out-of-pocket. For newer cars worth $20,000 or more, a $1,000 deductible makes financial sense since the deductible represents a smaller portion of the vehicle’s value and premium savings compound over time.

Emergency Fund Size Matters Most

Your available cash reserves should match your deductible amount exactly. Financial advisors recommend that you have three to six months of expenses saved, but your deductible needs immediate accessibility. If you can’t comfortably write a $1,000 check tomorrow, don’t select a $1,000 deductible regardless of premium savings. Higher deductibles can be financially dangerous for many drivers without adequate emergency funds.

Premium Savings vs Risk Calculation

Increasing your auto insurance deductible from $500 to $1,000 typically saves $200 to $400 annually on premiums. This means you break even after 2.5 years without a claim if you save $400 yearly. However, drivers who file claims every three years or more frequently should stick with lower deductibles. Higher deductibles prove profitable for safe drivers with substantial emergency funds.

Common Deductible Amounts and Their Real Impact

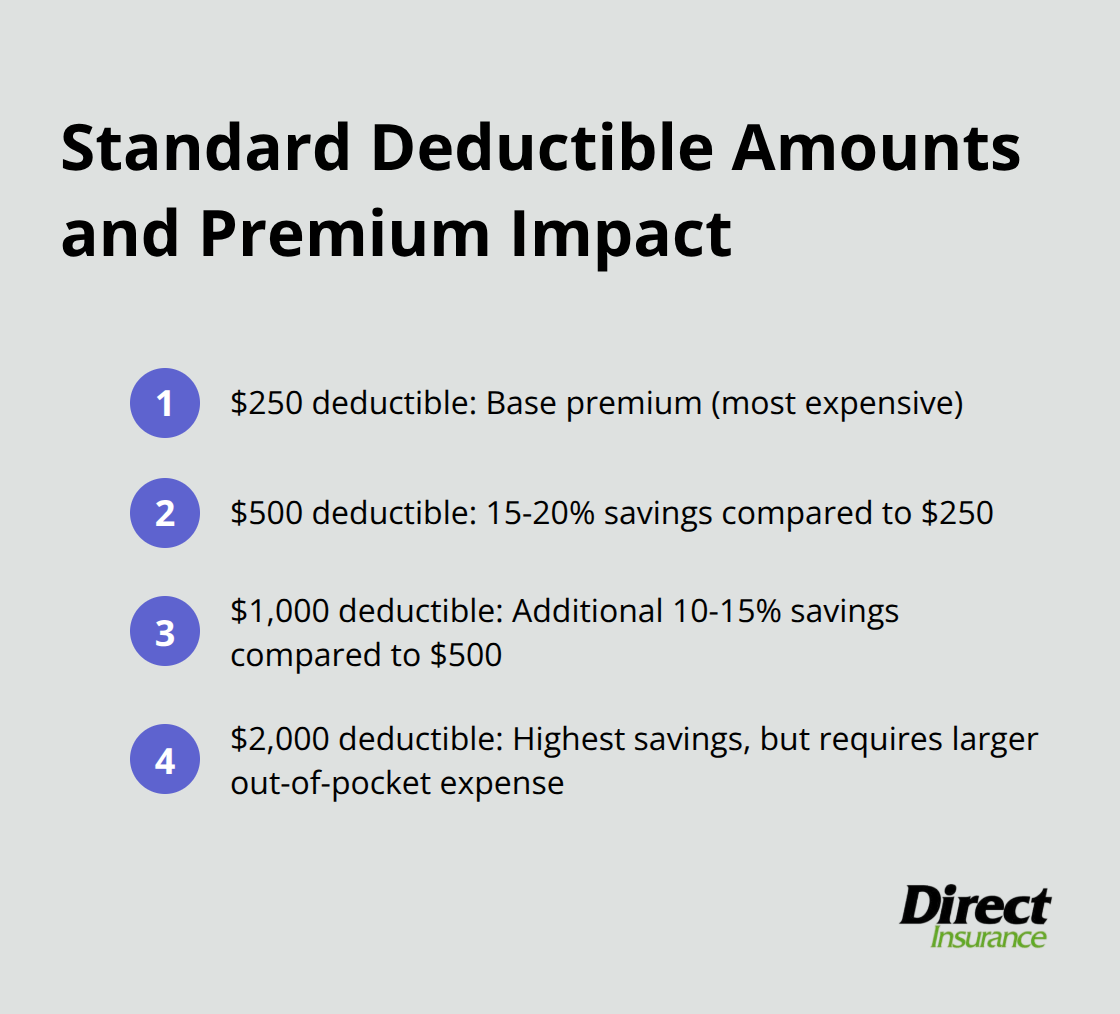

Most insurers offer standard deductible amounts of $250, $500, $1,000, and $2,000. The $500 deductible remains the most popular choice among drivers, but this middle-ground approach often costs more than necessary. Drivers who increase from $250 to $500 typically save 15-20% on premiums, while the jump from $500 to $1,000 saves an additional 10-15%. These percentage savings translate to real dollars that accumulate year after year, but only benefit drivers who can handle the higher out-of-pocket costs when claims occur.

When Does Your Deductible Apply

Collision and Comprehensive Claims Always Require Payment

Your deductible applies to every collision and comprehensive claim you file, regardless of fault determination or claim amount. If another driver hits your parked car and their insurance company accepts liability, you still pay your deductible upfront to your insurance company for repairs. Your insurer then pursues reimbursement from the at-fault driver’s insurance, which includes your deductible amount. This reimbursement process can take several weeks to months, which means you temporarily absorb the cost. Comprehensive claims for theft, vandalism, or weather damage also trigger immediate deductible payment, with no exceptions for circumstances beyond your control.

Liability Coverage Never Involves Deductibles

Liability coverage operates without any deductible requirements since it pays for damages you cause to other people’s property and injuries. When you rear-end another vehicle, your liability insurance covers their repair costs and medical expenses directly without any payment from you beyond your regular premium. Personal injury protection and uninsured motorist coverage vary by state (with some states mandating deductibles and others operating deductible-free). Medical payments coverage typically functions without deductibles and pays medical expenses immediately after accidents regardless of fault determination.

Multiple Claims Create Separate Deductible Obligations

Each individual claim requires a separate deductible payment, even when multiple incidents occur within short timeframes. If hail damages your car in March and you file a comprehensive claim, then hit a deer in April that requires another comprehensive claim, you pay two separate deductibles that total your selected amount multiplied by two. Some insurers offer disappearing deductible programs that reduce your deductible by $50-100 annually for claim-free periods, but these programs reset after any claim payment. Drivers who file multiple claims within short timeframes face significant out-of-pocket costs, making claim frequency a critical factor in deductible selection strategy.

Final Thoughts

Your auto insurance deductible choice affects your finances for years and ranks among the most important insurance decisions you make. Data reveals clear patterns: drivers with emergency funds benefit from higher deductibles through premium savings, while those without adequate cash reserves should prioritize lower deductibles despite higher monthly costs. The math favors higher deductibles for safe drivers who save $300 annually on premiums with a $1,000 deductible (breaking even after 3.3 years without a claim).

This strategy fails if you cannot afford the out-of-pocket expense when accidents occur. Higher deductibles prove profitable only for drivers with substantial emergency funds and clean records. Lower deductibles provide immediate financial relief during claims but elevate long-term insurance costs significantly.

We at Direct Insurance Services help clients find the optimal balance between premium costs and deductible amounts for their specific situations. Review your current deductible annually, especially after major life changes like new car purchases, emergency fund growth, or changes in your risk profile. Contact our experienced team to evaluate whether your current auto insurance deductible aligns with your financial situation and risk tolerance.