How to Save on Auto Insurance: Tips and Strategies for Lower Rates

Most drivers overpay for auto insurance without realizing it. Small changes to your coverage, strategic discount hunting, and comparing quotes across providers can cut your premiums significantly.

At Direct Insurance Services, we’ve seen firsthand how people save hundreds annually by understanding their options. This guide walks you through the most effective ways to lower your rates.

How Deductibles Affect Your Auto Insurance Rates

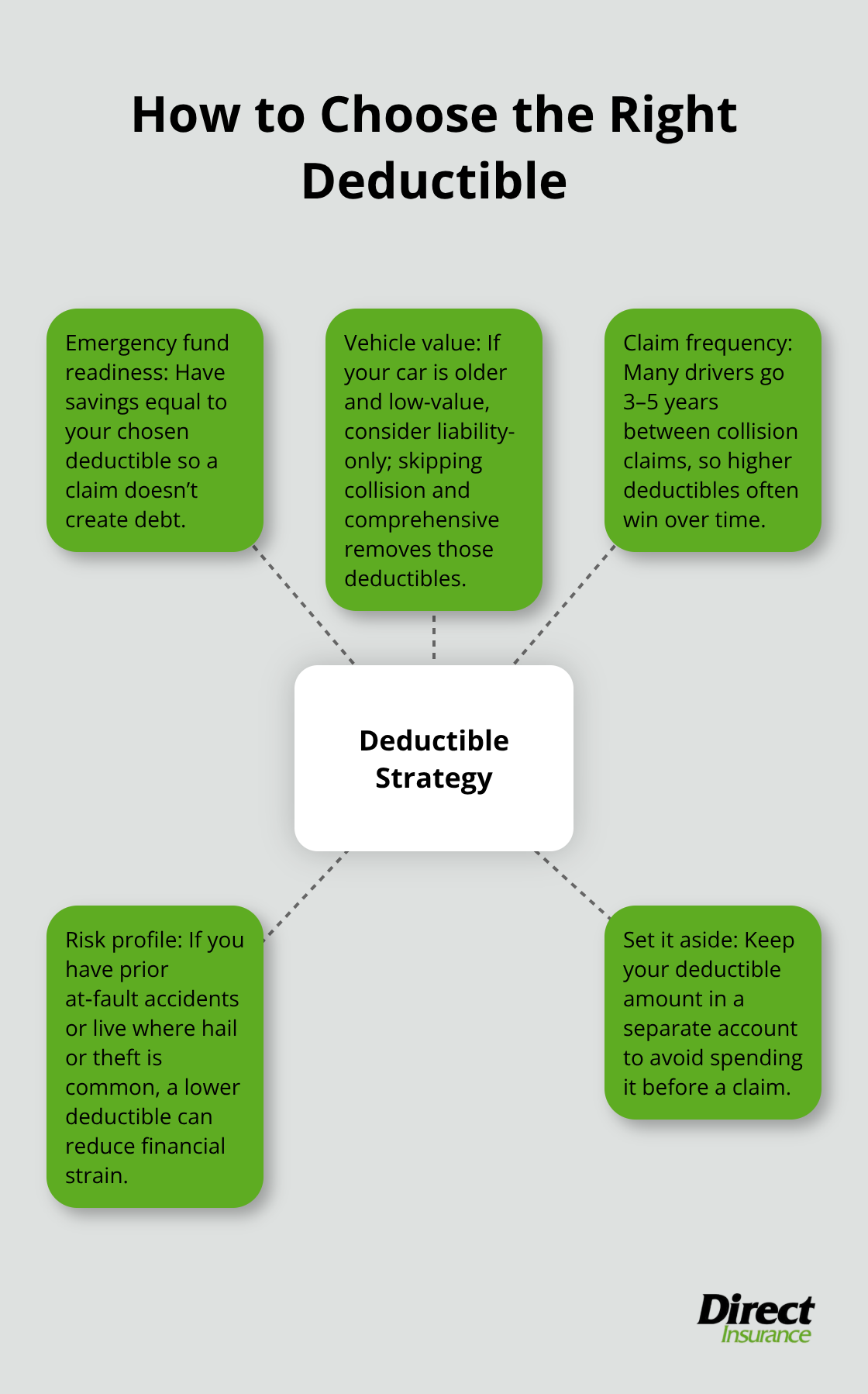

Your deductible is the amount you pay out of pocket when you file a claim, and it’s one of the most powerful levers you control to reduce your monthly premium. Here’s the reality: raising your deductible from $500 to $1,000 slashes premiums by an average of about 8.5 percent across the United States, depending on your insurer and vehicle. Clients save money annually just by adjusting this single number. The trade-off is straightforward-you absorb more cost upfront if an accident happens, but you pay less every month. This strategy works best if you have an emergency fund that covers your chosen deductible without forcing you into debt. If you can’t comfortably afford to pay $1,000 or $2,500 out of pocket, a lower deductible makes sense even if your premium is higher.

The math changes entirely if you drive an older vehicle worth less than $5,000. Many drivers insuring older cars carry only liability coverage and skip collision and comprehensive altogether, which eliminates deductibles entirely for those coverages. This approach only works if you can replace the vehicle without insurance money, but it’s worth calculating.

Understanding Deductible Amounts and Trade-offs

The higher your deductible, the lower your monthly premium. However, you must have sufficient savings to cover that deductible if you file a claim. If you lack an emergency fund, a lower deductible protects you from financial hardship, even if it costs more monthly.

Calculating the Right Deductible for Your Situation

To determine the right deductible for your situation, start by calculating three months of your current premium multiplied by 12 to see your annual cost. Then request quotes at different deductible levels-typically $250, $500, $1,000, and $2,500-and compare the annual savings. If raising your deductible saves you money but costs you an extra $500 if you claim, you break even after roughly two years of claims-free driving. Most drivers go 3 to 5 years between collision claims, which means the higher deductible almost always wins financially.

The key is honesty about your driving habits. If you have multiple at-fault accidents in your history or live in an area with frequent hail or theft, a lower deductible protects you from financial strain. If you maintain a clean driving record and park in a secure location, aggressive deductible increases make sense.

Impact of Higher Deductibles on Monthly Premiums

Once you’ve chosen your deductible, set that exact amount aside in a separate savings account. This removes the temptation to spend it and ensures you’re truly prepared if a claim happens. Your deductible choice directly affects your monthly bill-higher deductibles lower premiums, but only if you can actually afford to pay that amount when needed. The savings accumulate quickly, but only if you stay claims-free long enough to recoup the difference.

Now that you understand how deductibles work, the next step is uncovering discounts you likely qualify for but haven’t claimed yet.

Discounts You Might Be Missing Out On

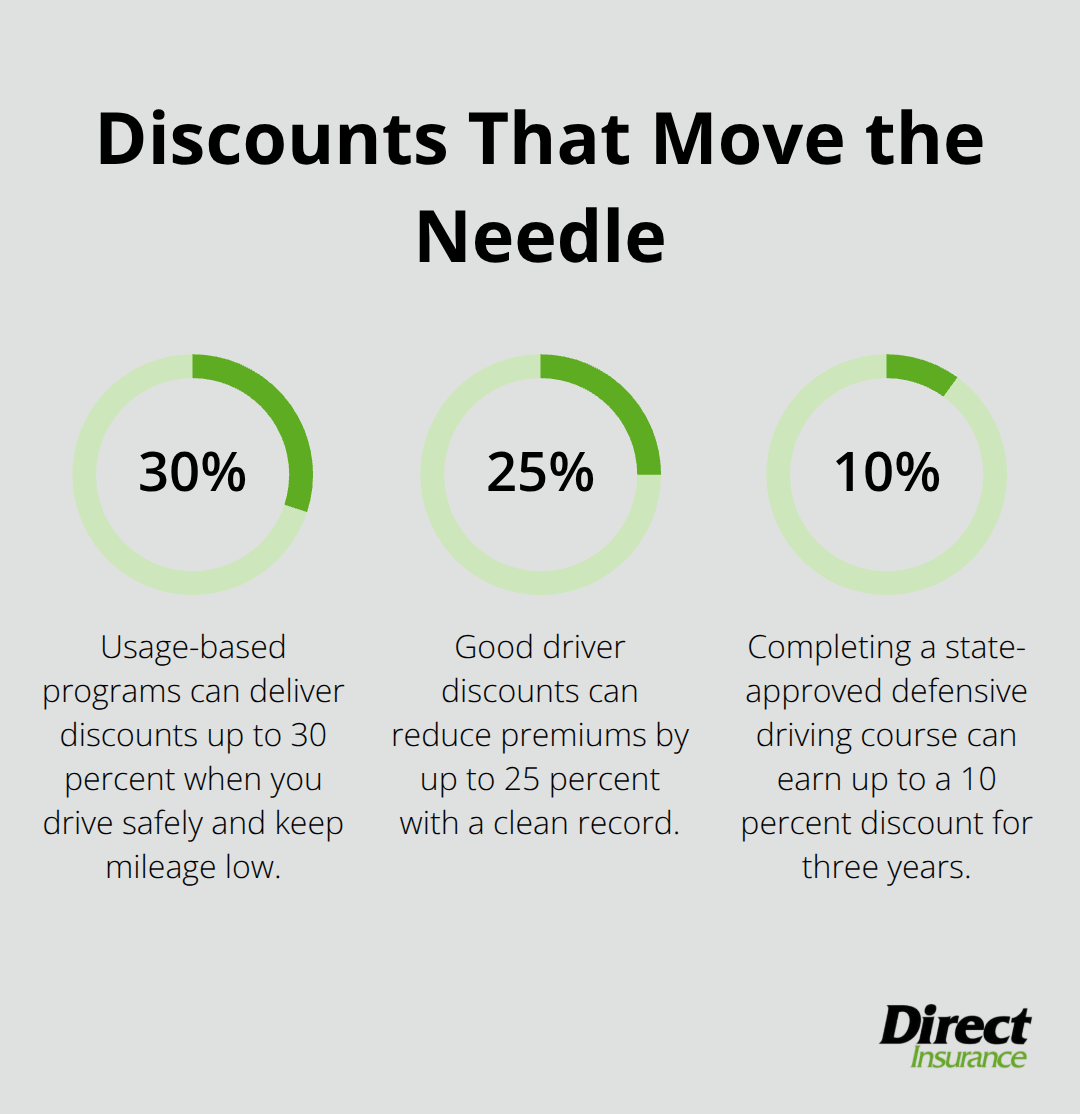

Most drivers leave money on the table by not asking about available discounts. The average driver qualifies for at least two to three discounts they never claimed. A clean driving record forms the foundation-drivers without at-fault accidents or violations typically qualify for good driver discounts that reduce premiums by 10 to 25 percent depending on your insurer. However, this discount doesn’t apply automatically. You must ask your agent specifically about safe driver discounts and provide documentation of your clean record.

Safe Driver and Good Driving Record Discounts

If you’ve gone three or more years without an accident or ticket, mention it directly when getting quotes. Some insurers offer accident forgiveness programs that prevent rate increases after your first at-fault claim, but only if you enroll before an accident happens. This protection matters far more than people realize-one collision can spike your premium by 25 to 40 percent for three to five years, so accident forgiveness essentially locks in your current rate even after a claim.

Bundle Coverage and Multi-Policy Discounts

Bundling your auto insurance with homeowners or renters coverage from the same company typically saves 10% to 25% on your total insurance bill. This is the single most underutilized strategy available. If you’re paying auto insurance through one company and home insurance through another, you’re almost certainly overpaying. Contact your home insurance provider and request a bundled auto quote, then contact your auto insurer and ask about adding homeowners coverage. The savings difference is often dramatic enough to justify switching both policies.

Low Mileage and Usage-Based Insurance Programs

Low-mileage discounts apply if you drive significantly less than average-typically under 10,000 to 12,000 miles annually. If you work from home, use public transit, or drive mainly for pleasure, tell your insurer your exact annual mileage. Some companies offer usage-based insurance programs like Snapshot or Milewise that monitor your actual driving habits through a mobile app or plug-in device. These programs reward safe driving and lower mileage with discounts up to 30 percent. The catch is they track your speed, hard braking, and time of day you drive, so this only works if you’re genuinely a safe driver.

Defensive Driving Courses and Additional Savings

Enroll in a state-approved defensive driving course-most states offer these online for around 30 to 50 dollars, and completion qualifies you for a 5 to 10 percent discount that lasts three years. This combines with your safe driver discount for compounding savings. Once you’ve claimed every discount available to you, the real savings opportunity emerges: comparing quotes across multiple insurers reveals just how much your current provider charges compared to competitors. Electronic auto-pay and anti-theft device discounts can provide additional savings depending on your insurer and the specific protection you add.

Shopping Around and Comparing Quotes

Why Annual Rate Comparisons Matter

Shopping for auto insurance once every three to five years can result in significant savings. Prices shift annually based on claims history, vehicle age, and competitive pressure between insurers, meaning your current rate today may be substantially higher than what competitors offer for identical coverage. At Direct Insurance Services, we recommend obtaining fresh quotes at minimum every three years, but annual shopping produces maximum savings. Prices vary dramatically across carriers-one company charges $1,200 annually while another charges $800 for the same protection. Most drivers never discover this gap because they assume their current insurer offers competitive rates.

What Information You Need to Gather for Accurate Quotes

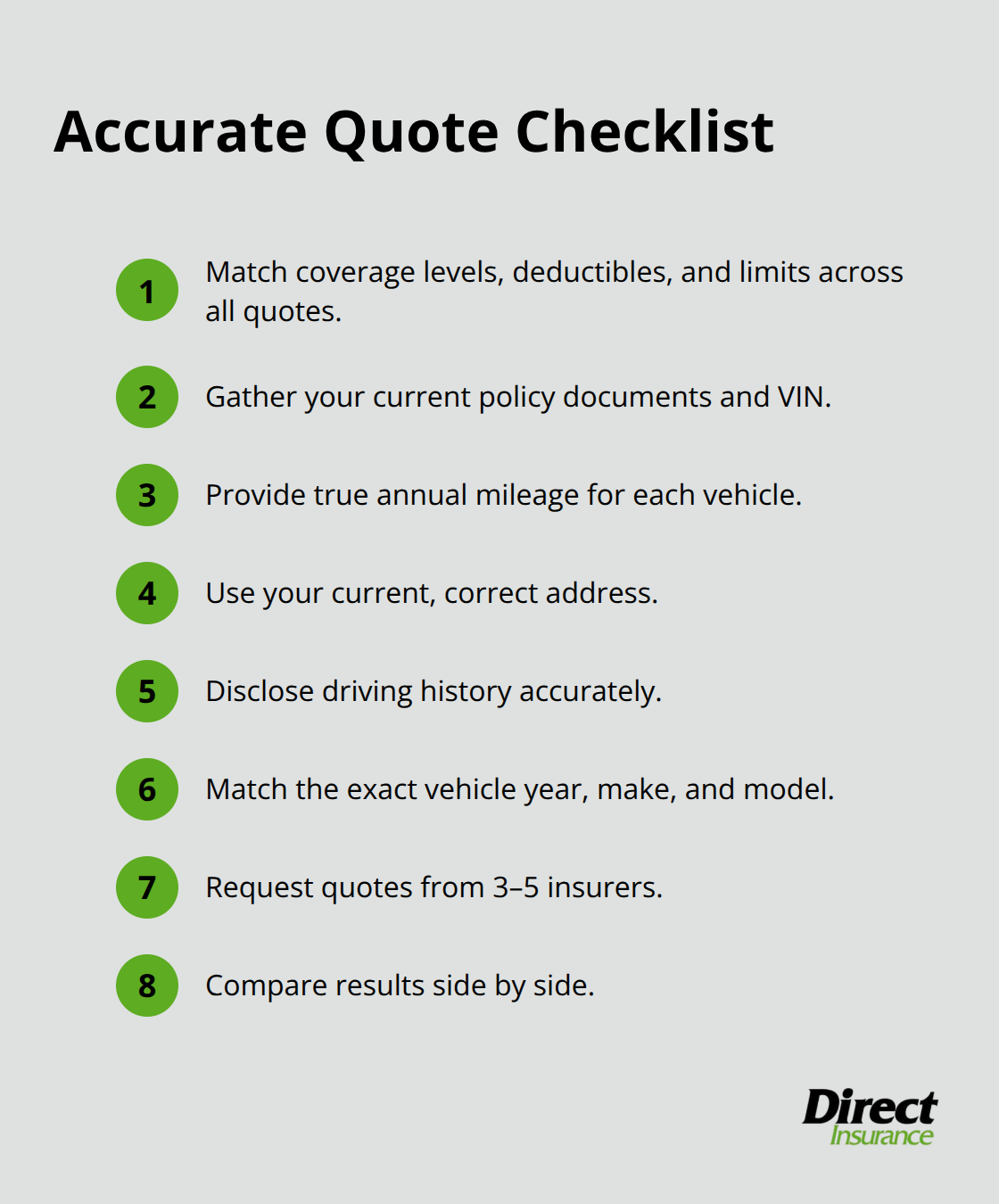

Start with your current policy documents and vehicle information, then contact at least three to five insurers for quotes using the exact same coverage levels, deductibles, and limits across all requests. Accuracy matters tremendously here. Provide your true annual mileage, current address, driving history, and exact vehicle make and model year to every insurer you contact. Mismatched information produces useless quotes that don’t reflect real pricing differences. Many drivers obtain quotes online in 15 minutes per insurer, and the time investment pays off when you compare results side by side.

Red Flags When Evaluating Different Insurance Providers

Red flags appear during this process if an insurer quotes significantly lower than competitors without explaining why, as this often signals coverage gaps or exclusions buried in the fine print. Read the quote details carefully and verify that liability limits, collision deductibles, and comprehensive coverage match across all quotes before comparing prices. Another warning sign is an insurer that seems dismissive about discounts. Ask every company directly what discounts you qualify for, and if they don’t mention good driver, bundling, low mileage, or safety feature discounts, push back and ask again. Some agents simply fail to apply available savings.

When you find a better rate, contact your current insurer before switching and ask if they’ll match it or offer additional discounts to keep your business. Loyalty sometimes works, but often the best rates come from switching to a new provider. Once you’ve selected a new insurer, verify the policy documents match your quote exactly before the coverage starts. Check that your address, vehicle information, drivers listed, and all applied discounts are correct. This final verification step prevents costly surprises when your policy activates.

Final Thoughts

You now have three concrete strategies to lower your auto insurance rates: adjusting your deductible to match your financial situation, claiming every discount you qualify for, and shopping for quotes at least every three years. These steps work independently, but combined they produce dramatic savings. A driver who raises their deductible, bundles policies, and switches to a cheaper insurer can easily save $500 to $1,500 annually.

Your rates change yearly based on your age, driving record, vehicle value, and competitive pricing shifts between insurers. A policy that offered the best rate three years ago may now be overpriced by hundreds of dollars. Life changes matter too-if you switched to remote work and now drive 5,000 miles annually instead of 15,000, your insurer needs to know this to apply low-mileage discounts.

Set a calendar reminder to review your policy every 12 months and spend 30 minutes gathering quotes from three to five insurers using identical coverage levels. If you find a better rate, switch; if your current insurer matches it or offers new discounts, stay. When you’re ready to take action on how to save on auto insurance, Direct Insurance Services can help you navigate your options and discover savings you may have missed.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation