What Does Landlord Insurance Not Cover?

Landlord insurance protects your rental property investment, but many property owners don’t realize the significant gaps in their coverage. Understanding what landlord insurance does not cover can save you thousands in unexpected expenses.

We at Direct Insurance Services see landlords face costly surprises when they assume their policy covers everything. The reality is that standard landlord insurance excludes many common risks that could impact your bottom line.

What Major Gaps Exist in Standard Landlord Insurance

Standard landlord insurance exposes property owners to three major financial risks that catch most landlords unprepared. The first major exclusion involves tenant personal belongings, which means anything your tenants own inside the rental property falls outside your coverage scope. When a fire destroys the building, your insurance covers structural repairs but not the tenant’s furniture, electronics, or clothing. This distinction matters because tenants often blame landlords for their losses and create potential liability issues even though standard policies provide no protection for these items.

Normal Wear and Tear Creates Expensive Blind Spots

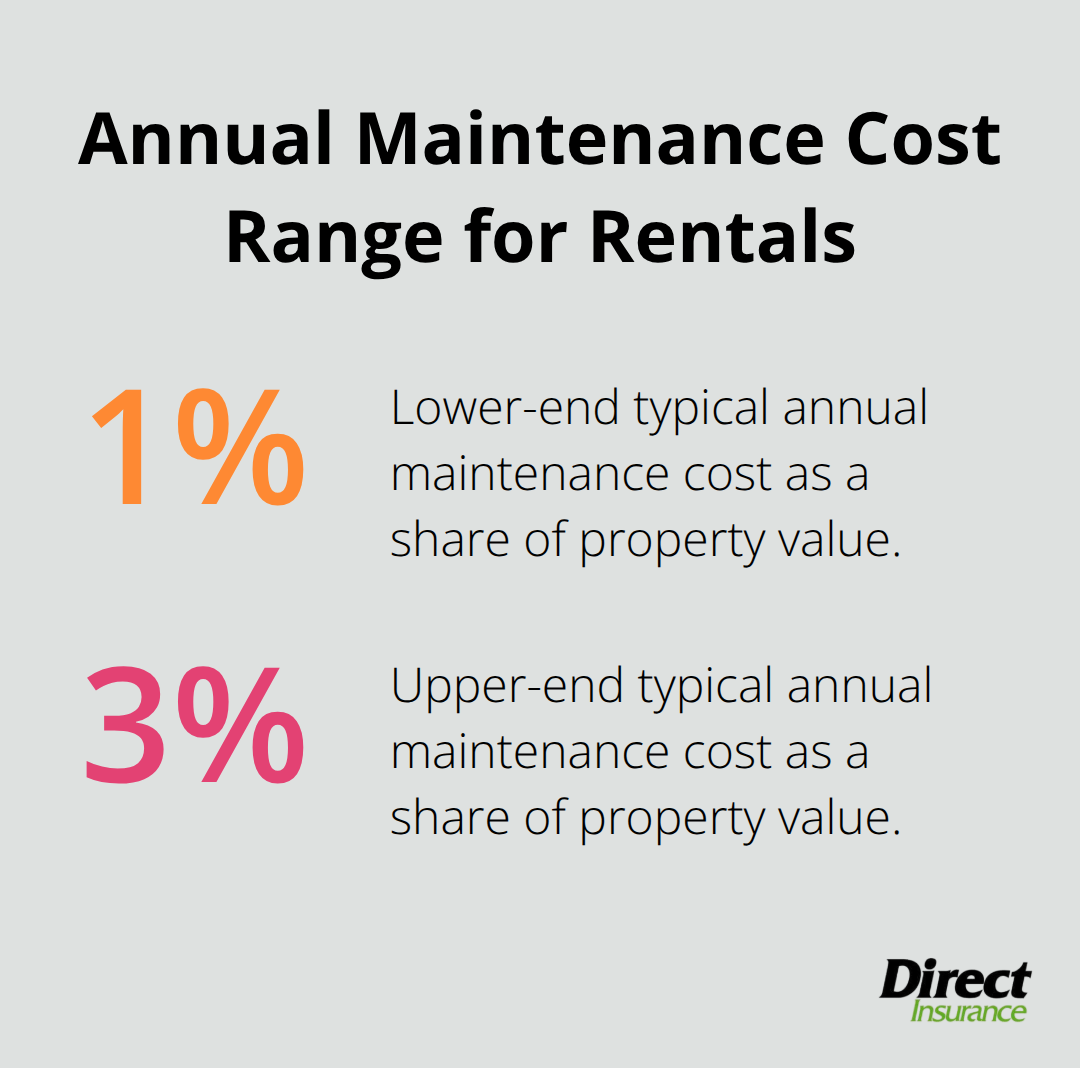

Landlord insurance never covers normal wear and tear, yet this represents one of the largest expenses for rental property owners. Paint fades, carpets wear thin, appliances break down from regular use, and minor plumbing issues fall squarely on your shoulders. Maintenance costs typically range from 1% to 3% of property value annually, which means a $300,000 rental property requires $3,000 to $9,000 in yearly upkeep that insurance won’t touch. Tenant damage beyond normal use might qualify for coverage, but property owners often face costly legal battles when they try to prove the difference between normal wear and actual damage.

Natural Disasters Require Separate Protection

Flood and earthquake damage represent the most expensive exclusions in standard landlord insurance policies. Just one inch of floodwater can cause significant property damage, yet standard policies exclude all flood losses. Earthquake coverage faces similar exclusions and leaves property owners in seismic zones completely vulnerable. These natural disaster policies require separate purchases through specialized providers, often at additional costs of thousands annually depending on your property’s risk level and location.

Vacancy Periods Void Standard Coverage

Most landlord insurance policies automatically void coverage after 30-60 days of vacancy, yet property owners rarely understand this limitation until they file a claim. Extended vacancies between tenants can leave your property completely unprotected against theft, vandalism, or weather damage. Insurance companies view vacant properties as higher risk because no one monitors the property daily for potential issues. Property owners must purchase separate vacant property endorsements or notify their insurer immediately when tenants move out to maintain any protection.

These coverage gaps create the foundation for understanding why landlords need additional protection beyond standard policies.

Common Misconceptions About Landlord Insurance Coverage

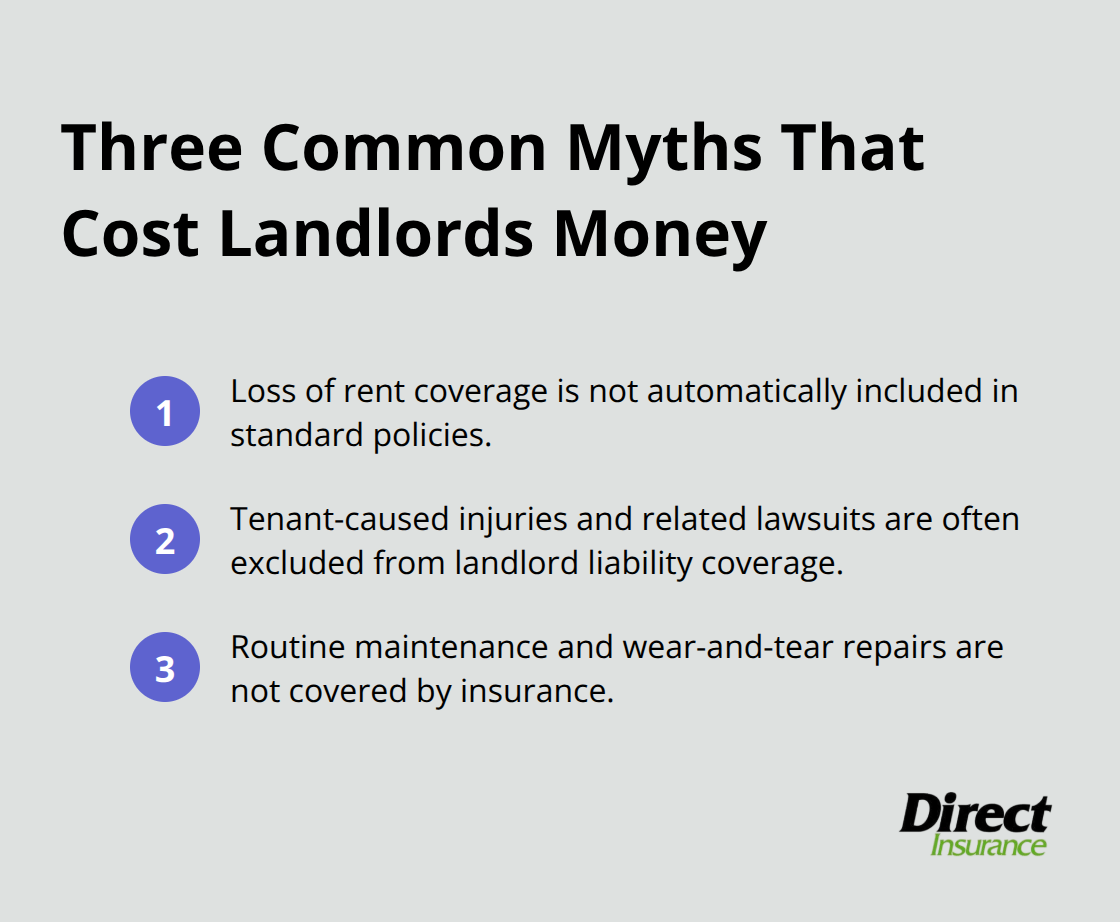

Property owners lose thousands annually because they believe three dangerous myths about landlord insurance coverage. The first myth assumes that rental income protection automatically comes with standard policies, but most landlord insurance policies provide zero coverage for lost rent during repairs or tenant disputes. Only a small percentage of landlord policies include automatic loss of rent coverage according to industry data, and those that do typically limit payments to 12 months maximum.

Property owners face extended repairs from water damage or fire and often discover their mortgage payments continue while rental income stops completely. Smart landlords purchase separate loss of rent riders that cost roughly $200-400 annually but can save $15,000-30,000 in lost income during major repairs.

Tenant Liability Creates Expensive Legal Blind Spots

The second costly myth involves liability coverage for tenant actions, where property owners wrongly assume their insurance protects them from all tenant-related lawsuits. Standard landlord policies exclude coverage when tenants cause injuries to guests or other tenants through negligence (this leaves property owners exposed to lawsuits that can reach six figures).

Insurance companies specifically exclude tenant-on-tenant violence, drug-related activities, and illegal subletting situations from liability protection. Property owners need umbrella policies that start at $150-300 annually to cover these gaps, especially in states with tenant-friendly laws where landlords face higher lawsuit risks.

Maintenance Exclusions Drain Property Profits

The third myth assumes insurance covers all property repairs, but maintenance exclusions create the largest expense category for rental properties. Plumbing failures from normal use, HVAC breakdowns, roof repairs from aging, and electrical issues fall entirely outside insurance coverage regardless of cost.

Appliance failures alone cost landlords significant amounts annually per property according to property management studies. Home warranty programs that cost $300-600 yearly can cover major appliance and system breakdowns (these programs fill critical gaps that standard policies ignore completely).

These misconceptions highlight why landlords must explore additional coverage options that address specific gaps in standard policies.

What Additional Protection Do Landlords Actually Need

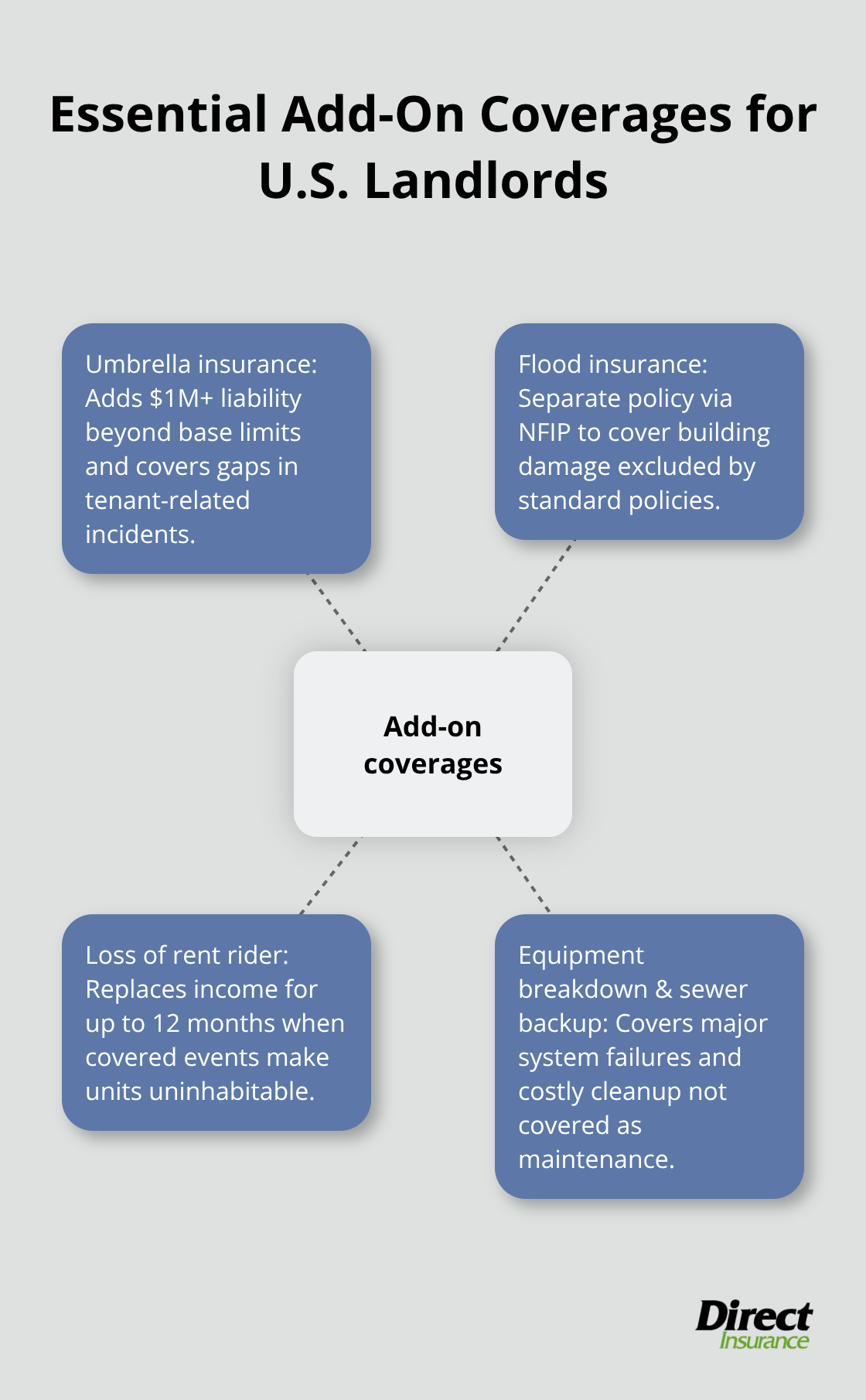

Smart landlords purchase three specific coverage types that standard policies ignore, starting with umbrella insurance that provides liability protection beyond basic policy limits. Umbrella policies cost between $150-300 annually for $1 million in additional coverage and protect against lawsuits that exceed your standard liability limits of $300,000-500,000. Property owners in high-lawsuit states like California and New York face tenant injury claims that regularly reach significant amounts according to legal industry data, making umbrella coverage essential rather than optional. These policies cover gaps in tenant-related liability situations where standard landlord insurance fails, including tenant-on-tenant violence, slip-and-fall incidents involving tenant guests, and discrimination lawsuits that can devastate property owners financially.

Flood Insurance Requires Immediate Action

Flood insurance through the National Flood Insurance Program costs $400-2,000 annually depending on flood zone designation and provides up to $250,000 in building coverage that standard policies completely exclude. Properties in moderate flood zones face significant flooding risk during mortgage periods according to FEMA data, yet most landlords skip this coverage until too late. Flood policies require 30-day waiting periods before activation, which means emergency purchases after storm warnings provide zero protection.

Loss of Rent Coverage Protects Income Streams

Loss of rent coverage riders cost $200-400 annually but replace up to 12 months of rental income when covered events make properties uninhabitable, filling the income gap that destroys landlord cash flow during extended repairs. Property owners face extended repairs from water damage or fire and often discover their mortgage payments continue while rental income stops completely. These riders activate when covered perils force tenants to vacate temporarily, providing monthly payments that match your rental income until repairs complete.

Equipment Breakdown Coverage Protects Major Systems

Home warranty programs cost $300-600 yearly and cover HVAC systems, appliances, and electrical components that standard policies exclude as maintenance items. These programs typically save landlords significant amounts annually on major appliance failures and system breakdowns that occur in rental properties. Sewer backup endorsements add $50-100 to annual premiums but cover cleanup costs that average significant amounts per incident according to insurance industry claims data.

Final Thoughts

Property owners who understand what landlord insurance does not cover protect their investments from expensive surprises. Standard policies exclude tenant belongings, normal wear and tear, flood damage, earthquake damage, and vacancy periods. These gaps cost landlords thousands annually when they assume complete protection exists.

Independent insurance agents help landlords identify specific policy gaps and recommend targeted solutions that fit their budgets. We at Direct Insurance Services work with multiple carriers to create customized protection plans rather than offer generic policies. Independent agents provide access to specialized coverage options that address the unique risks rental properties face.

Property owners should review their landlord insurance annually and examine policy exclusions carefully (this prevents costly surprises during claims). Calculate potential losses from uncovered risks and purchase additional riders for flood insurance, loss of rent coverage, and umbrella liability protection. Contact Direct Insurance Services to evaluate your current coverage and identify gaps that could impact your rental property profits.