Auto Insurance Guide for New Drivers

Getting your first car means you need auto insurance for new driver protection. The process can feel overwhelming with so many coverage options and confusing terms.

We at Direct Insurance Services know that new drivers face higher premiums and unique challenges when shopping for coverage. This guide breaks down everything you need to know to make smart insurance decisions and save money.

What Auto Insurance Coverage Do You Actually Need

Essential Coverage Types Every New Driver Must Have

Auto insurance contains six main types of coverage, but only two are mandatory in most states. Liability coverage protects others when you cause an accident and costs an average of $1,400 annually according to the Insurance Information Institute. This required coverage includes bodily injury liability, which pays medical bills for injured parties, and property damage liability, which covers vehicle repairs and property damage you cause.

Most states require liability insurance before you can legally drive. Without this coverage, you face license suspension and substantial fines that far exceed the cost of basic insurance.

Optional Coverage That Protects Your Investment

Collision and comprehensive coverage protect your own vehicle but remain optional in most states. Collision pays for accident damage regardless of fault, while comprehensive covers theft, vandalism, and weather damage. New drivers with vehicles worth more than $4,000 should purchase both types since repair costs often exceed the deductible.

Personal injury protection covers your medical expenses after accidents, and uninsured motorist coverage protects you from drivers without adequate insurance. These coverages become particularly valuable when you consider that many drivers carry only minimum liability limits.

Key Factors That Drive Your Premium Costs

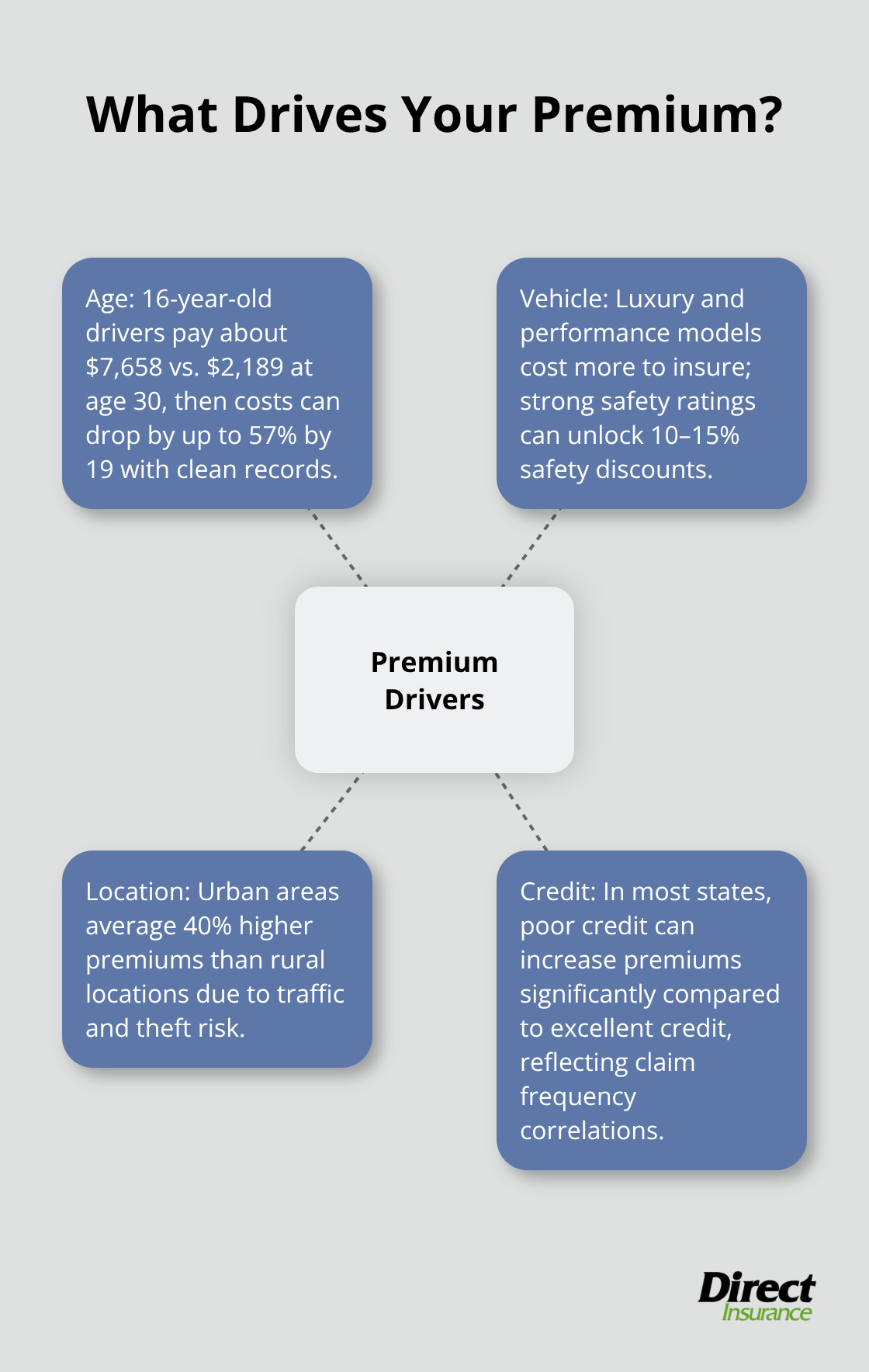

Insurance premiums depend on four key factors that dramatically affect your costs. Age impacts rates most significantly, with 16-year-old drivers paying $7,658 annually compared to $2,189 for 30-year-old drivers (a 254% difference that reflects crash statistics).

Your vehicle choice matters equally – luxury cars like Mercedes cost substantially more to insure than economy models due to higher repair costs and theft rates. Location determines rates through accident frequency and crime statistics, with urban areas averaging 40% higher premiums than rural locations.

Your credit score influences premiums in most states, with poor credit increasing costs by up to 115% compared to excellent credit scores. Understanding these factors helps you make informed decisions about coverage levels and vehicle selection that will impact your rates for years to come.

What Makes Your Insurance Rate So Expensive

Age Creates the Biggest Premium Shock

Your age dominates insurance costs more than any other factor. Teen boys pay $495 more yearly than teen girls according to industry data, with 16-year-old male drivers facing significantly higher premiums due to higher accident frequency. This gender gap reflects crash statistics that show teenage male drivers speed more frequently, drive aggressively, and wear seatbelts less often than their female counterparts.

Rates drop dramatically with experience. Teen drivers see insurance costs decrease by up to 57% from age 16 to 19 with clean records. The Insurance Institute for Highway Safety reports that fatal crash rates for drivers aged 16-19 are three times higher per mile driven than drivers over 20, which explains why insurers price policies so aggressively for new drivers.

Vehicle Choice Determines Your Premium Category

Your car selection directly impacts insurance costs through repair expenses and theft statistics. High-performance vehicles and luxury brands like Porsche or Mercedes carry substantially higher premiums due to expensive parts and labor costs. Vehicles with superior safety ratings from the National Highway Traffic Safety Administration qualify for discounts, while cars with high theft rates increase your comprehensive coverage costs.

Choose vehicles with strong safety features and lower theft rates. Cars equipped with anti-lock brakes, airbags, and electronic stability control often qualify for safety discounts that can reduce premiums by 10-15%. Avoid modified vehicles or sports cars during your first years of driving, as these choices can double insurance costs compared to standard sedans or compact cars.

Credit and Location Create Hidden Rate Multipliers

Your credit score influences premiums in most states, with poor credit increasing costs by up to 115% compared to excellent credit scores. Insurance companies use credit-based insurance scores because data shows strong correlations between credit responsibility and claim frequency. New drivers should focus on building credit through responsible use of student credit cards or becoming authorized users on parent accounts.

Geographic location affects rates through accident frequency and crime statistics. Urban areas average 40% higher premiums than rural locations due to increased traffic density and theft rates. States like North Carolina offer the lowest teen driver premiums at $3,692 annually, while New Hampshire, Louisiana, and Florida exceed $10,000 for teen coverage (making location one of the most significant cost factors).

These rate factors work together to create your final premium, but smart new drivers can take specific steps to reduce these costs through strategic discount opportunities and policy choices.

How Can New Drivers Cut Insurance Costs

Target These High-Value Discounts First

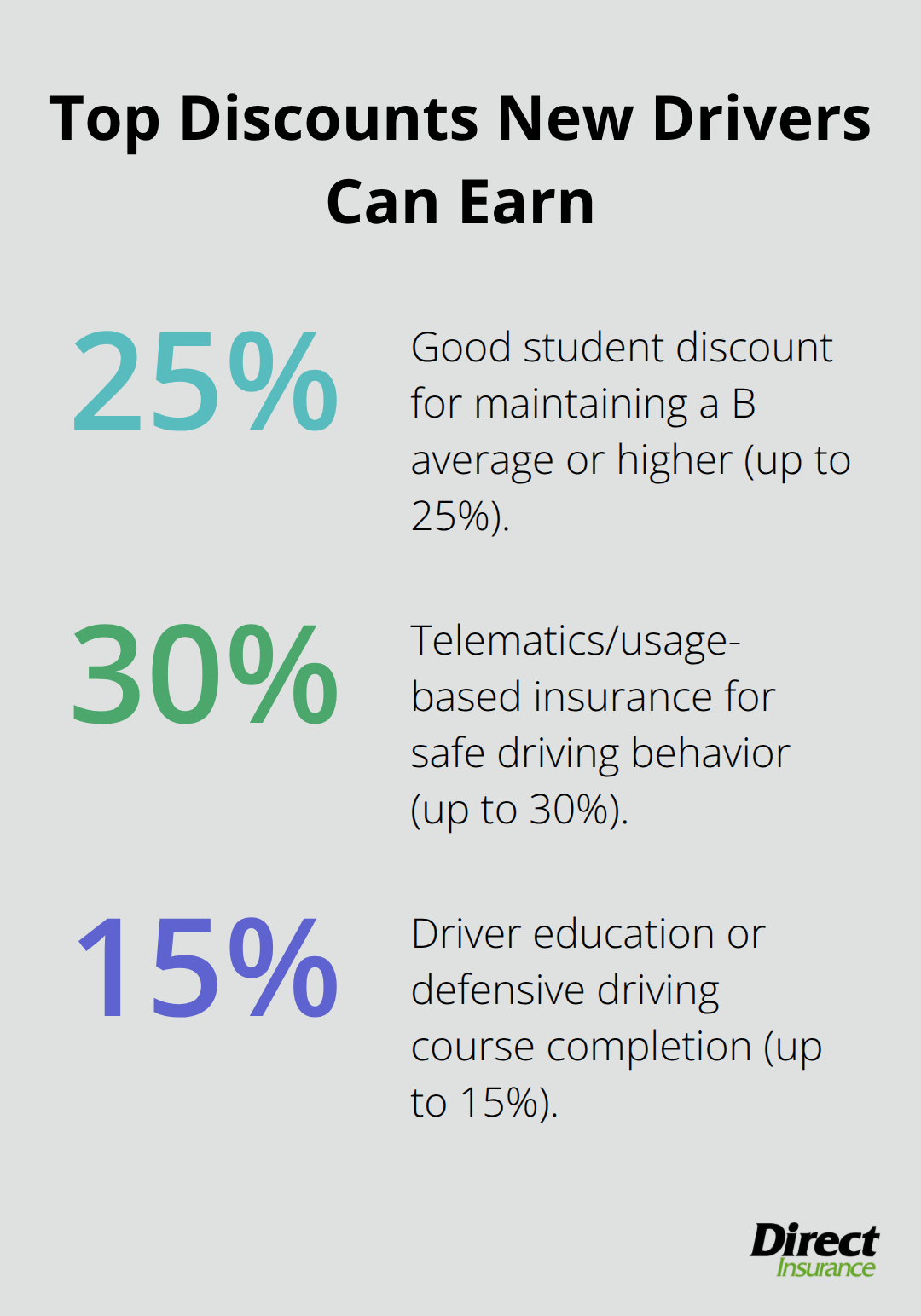

Good student discounts deliver the biggest savings for new drivers, with insurers reducing premiums by 15-25% for students who maintain a B average or higher. Erie Insurance offers the lowest average rates for teen drivers at $3,478 for females and $4,351 for males, making them worth comparing against other carriers. Driver education course completion cuts costs by another 5-15%, with defensive driving programs from organizations like the National Safety Council providing certificates that most insurers accept.

Telematics programs represent the fastest growing discount category, with usage-based insurance monitoring your driving behavior through smartphone apps or plug-in devices. Safe drivers save up to 30% through these programs when they demonstrate good habits like smooth braking, moderate acceleration, and avoiding late-night driving. Multi-car discounts apply when you join a family policy rather than purchase separate coverage (typically saving 10-25% compared to individual policies).

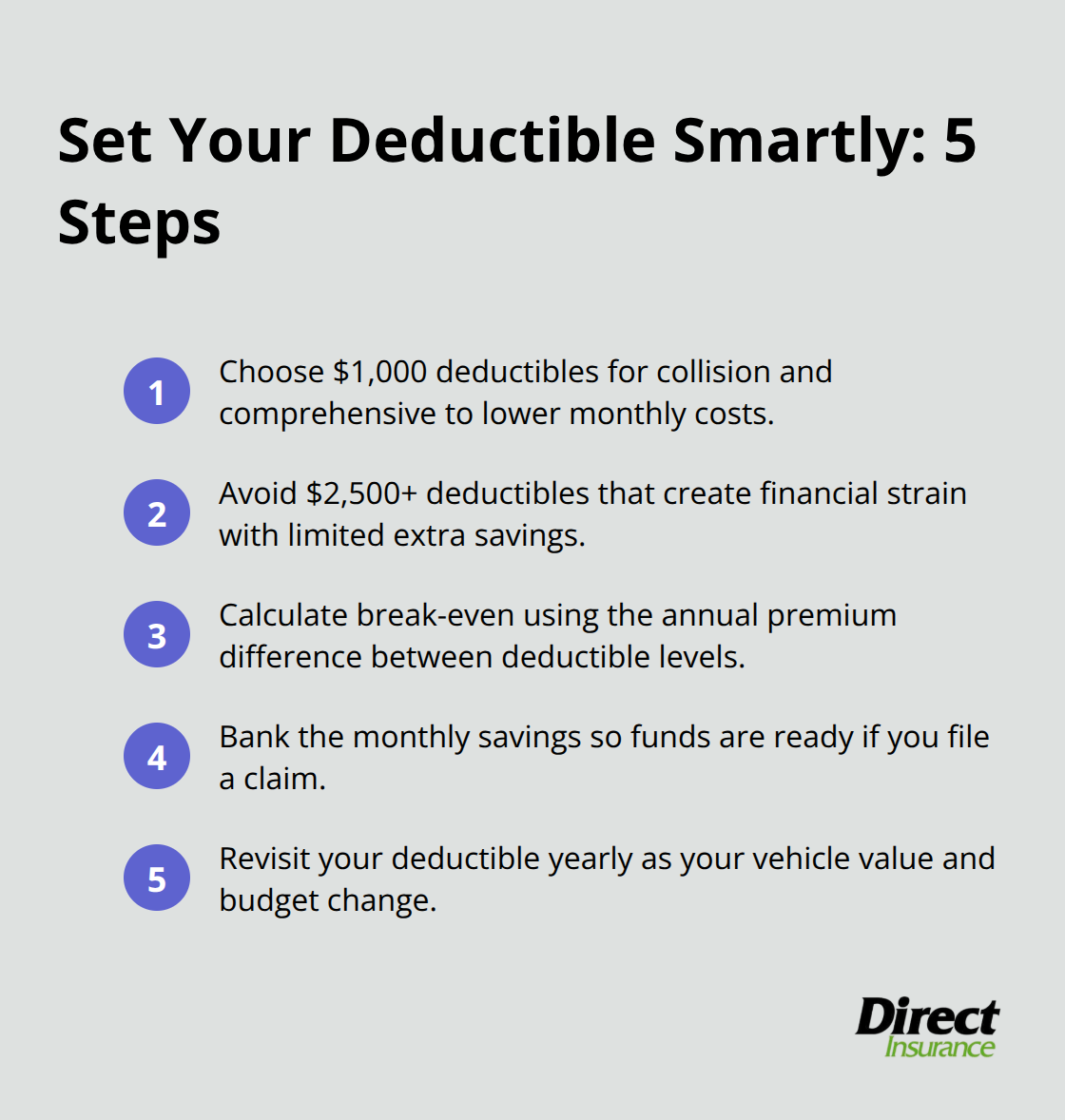

Set Your Deductible at $1,000 for Maximum Savings

New drivers should choose $1,000 deductibles on collision and comprehensive coverage to reduce monthly premiums by 25-40% compared to $250 deductibles. This strategy works because insurance losses vary significantly by vehicle class and size, making the higher deductible manageable while generating substantial monthly savings. Avoid $2,500 or higher deductibles since the additional savings become minimal while creating financial strain during accidents.

Calculate your annual premium difference between deductible levels to determine break-even points. If switching from $250 to $1,000 deductibles saves $600 annually, you recover the higher deductible cost in less than two years of claim-free driving. Keep your deductible amount in a separate savings account to prepare for potential claims.

Bundle Renters Insurance for Instant Multi-Policy Savings

Adding renters insurance to your auto policy creates immediate savings of 5-25% on both coverages while providing valuable personal property protection. Renters insurance costs only $180 annually on average but can reduce your auto premium by $200-400 yearly through multi-policy discounts. This combination protects your belongings in apartments or rental homes while maximizing your insurance budget efficiency (making it one of the smartest financial moves for young adults).

Final Thoughts

Auto insurance for new driver coverage requires three essential steps that will set you up for success. Start by collecting your driver’s license number, Social Security number, and vehicle identification number before you request quotes. Compare rates from at least five insurers since premiums vary dramatically between companies, with some offering rates 23-26% below national averages for teen drivers.

An independent agent provides access to multiple carriers without the pressure of single-company sales tactics. We at Direct Insurance Services help new drivers navigate coverage complexities by comparing options from top-rated carriers to find policies that fit both needs and budgets. Independent agents understand the unique challenges new drivers face and can identify discount opportunities you might miss when you shop alone.

Good habits immediately impact your future insurance costs. Maintain a clean record since a single speeding ticket increases annual premiums by $435 on average (making every safe mile count toward lower future premiums). Complete defensive driving courses for immediate discounts and consider telematics programs that monitor your behavior, as safe drivers save up to 30% through these usage-based insurance options.