What Are Deductibles in Auto Insurance Policies?

Auto insurance deductibles directly impact both your premium costs and out-of-pocket expenses when filing claims. Many drivers don’t fully understand what are deductibles in auto insurance and how choosing the wrong amount can cost them hundreds of dollars.

We at Direct Insurance Services see drivers make costly deductible mistakes every day. This guide breaks down everything you need to know about deductibles to make informed decisions about your coverage.

What Exactly Is an Auto Insurance Deductible

An auto insurance deductible is the fixed amount you pay out of pocket before your insurance company covers the remaining costs of a covered claim. Your deductible applies each time you file a claim, not annually like health insurance deductibles.

How Deductible Payments Work in Real Claims

When you file a claim, you pay your deductible first, then your insurer covers the remaining costs. If your car sustains $3,000 in damage and you have a $500 deductible, you pay $500 while your insurance company pays $2,500. However, if repair costs are $400 and your deductible is $500, you pay the entire $400 since it falls below your deductible threshold. Most insurers require you to pay the deductible directly to the repair shop or reimburse you after you pay it yourself.

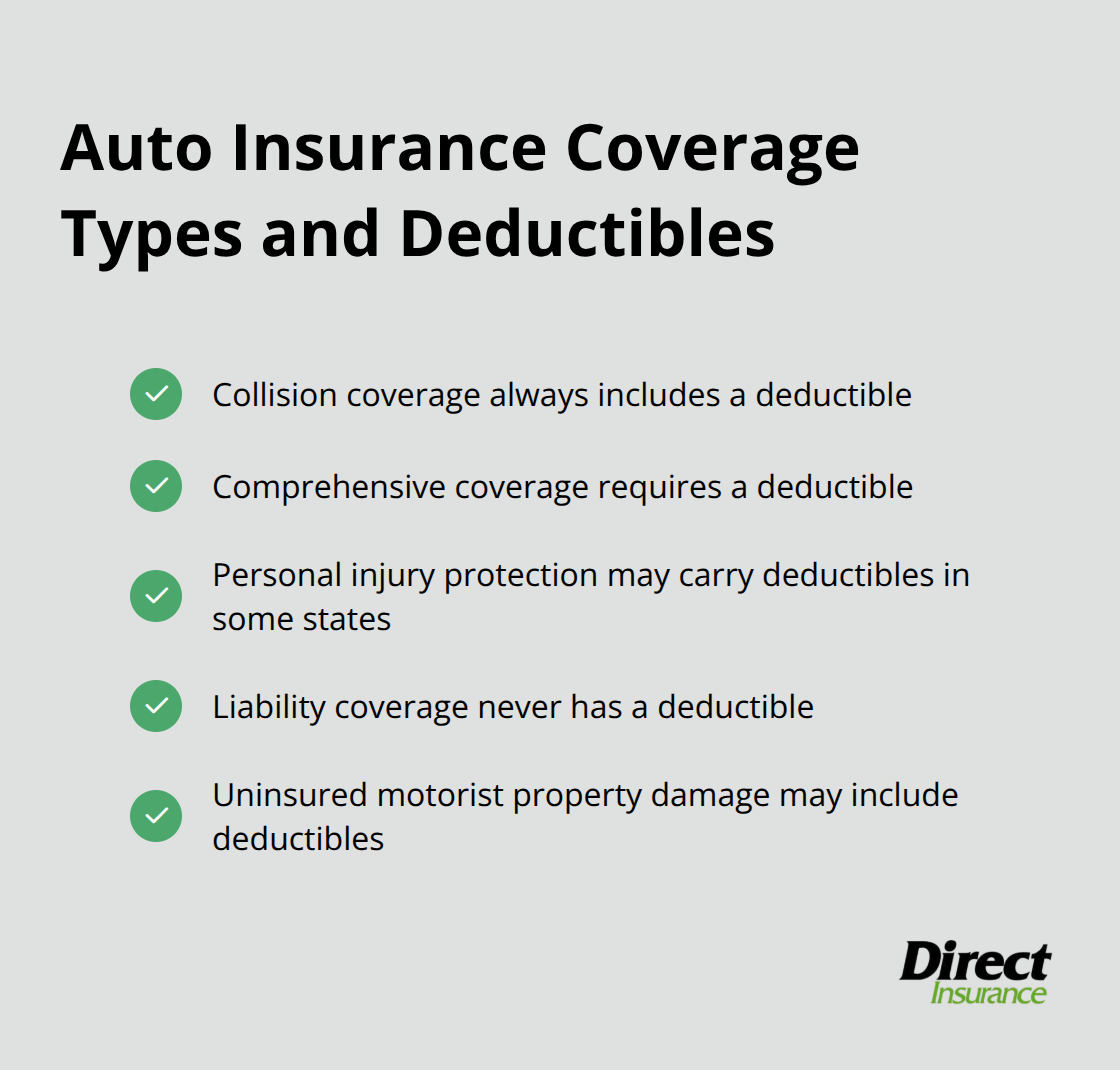

Which Coverage Types Require Deductibles

Collision coverage always includes a deductible when you hit another vehicle or object. Comprehensive coverage requires a deductible for theft, vandalism, weather damage, and animal strikes. Personal injury protection carries deductibles in states like Delaware and Florida. Liability coverage never has a deductible since it pays for damage you cause to others. Uninsured motorist property damage may include deductibles (depending on your state), while uninsured motorist bodily injury typically does not.

When Deductibles Don’t Apply

You won’t pay a deductible when another driver causes an accident and their liability insurance covers your repairs. Hit-and-run situations typically require you to pay your collision deductible unless you can identify the other driver. Some states offer collision damage waivers that eliminate deductibles when uninsured drivers hit you. Glass repair coverage sometimes waives deductibles for windshield replacement in certain areas where stone chips are common.

The amount you choose for your deductible significantly affects both your monthly premiums and potential out-of-pocket costs when accidents happen.

What Deductible Amounts Should You Choose

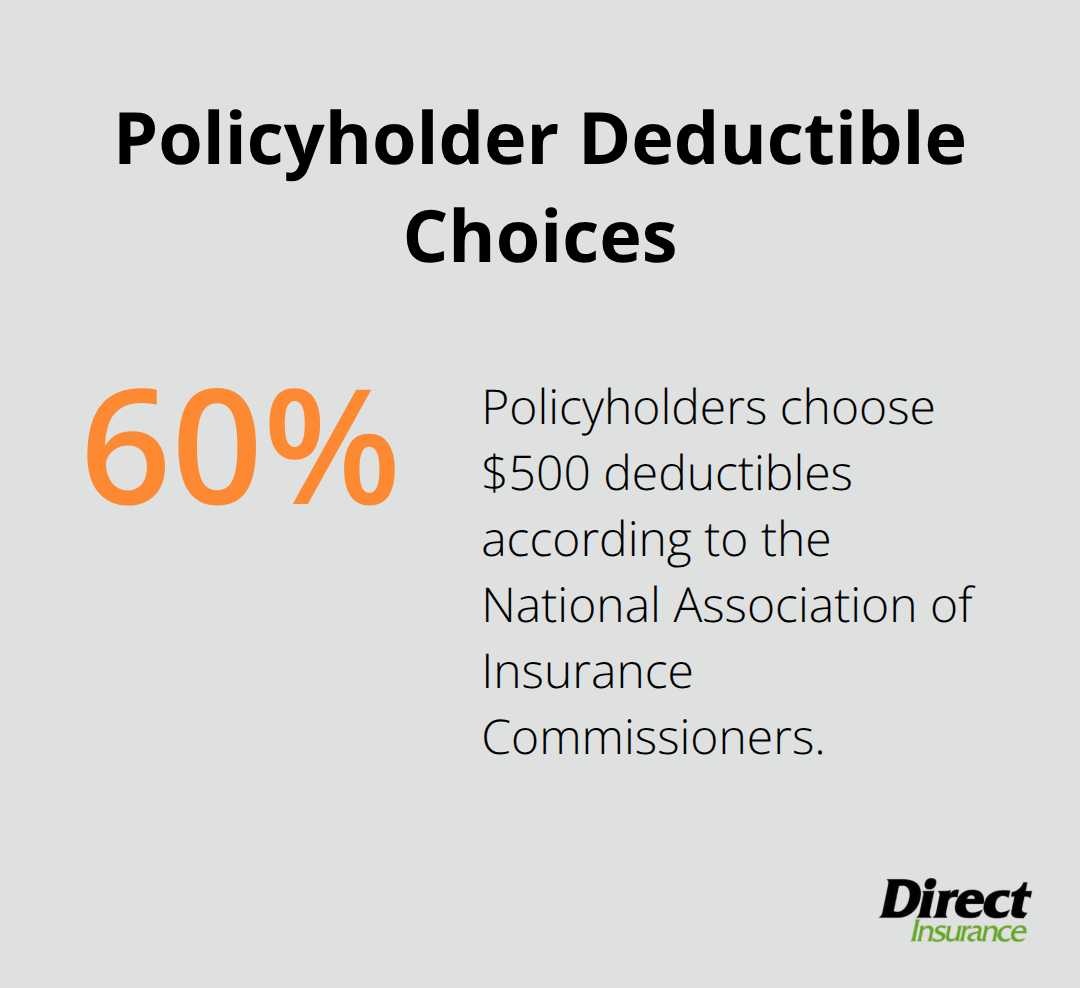

Most drivers select deductibles between $500 and $1,000, with the National Association of Insurance Commissioners reporting that over 60% of policyholders choose $500 deductibles. However, this popular choice isn’t always the smartest financial decision. Standard deductible ranges typically span from $250 to $2,000 for collision and comprehensive coverage, while personal injury protection deductibles in states that require them usually range from $250 to $1,000.

Higher Deductibles Create Substantial Premium Savings

Raising your deductible from $500 to $1,000 can provide savings, though the exact amount varies by insurer and driver profile. Drivers who choose a higher deductible save an average of $600 annually compared to $250 deductibles, but this strategy only works if you can comfortably pay the higher out-of-pocket amount during a claim. Your vehicle’s value should guide this decision-if your car is worth $15,000, a $2,000 deductible makes sense, but if your car is worth $5,000 or less, choose a $250 or $500 deductible.

Financial Readiness Determines Your Best Option

Your emergency fund balance directly impacts which deductible amount works best for your situation. Financial experts recommend you maintain savings equal to at least your deductible amount before you select higher options. Drivers who struggle to cover unexpected $1,000 expenses should stick with $250-500 deductibles despite the higher premiums. Those with solid emergency funds (typically 3-6 months of expenses) can confidently choose $1,000-2,000 deductibles for maximum premium savings.

Regional Factors That Drive Deductible Decisions

Utah drivers face unique considerations that should influence deductible choices. Hail damage occurs frequently along the Wasatch Front, which makes lower comprehensive deductibles valuable for protection against weather-related claims. Areas with high deer populations like southern Utah benefit from lower comprehensive deductibles since animal strikes happen often and cost thousands to repair. Urban drivers in Salt Lake City and Provo should consider their higher theft and vandalism risks when they set comprehensive deductibles.

These location-specific risks directly connect to how deductibles affect your overall insurance costs and claim experiences.

How Deductibles Impact Your Premium and Out-of-Pocket Costs

Deductible choices create dramatic differences in your annual insurance costs, often more than drivers realize. Understanding how auto insurance deductibles work helps you select the best option for your situation, with higher deductibles typically reducing your premium costs. Comprehensive coverage follows similar patterns, with higher deductibles cutting costs significantly per year.

State Farm reports that drivers who raise both collision and comprehensive deductibles from $500 to $1,000 save an average of $467 annually, while those who jump from $250 to $2,000 can save over $900 yearly. However, these savings disappear quickly if you file multiple claims within a few years.

Premium Savings vs Claim Frequency Analysis

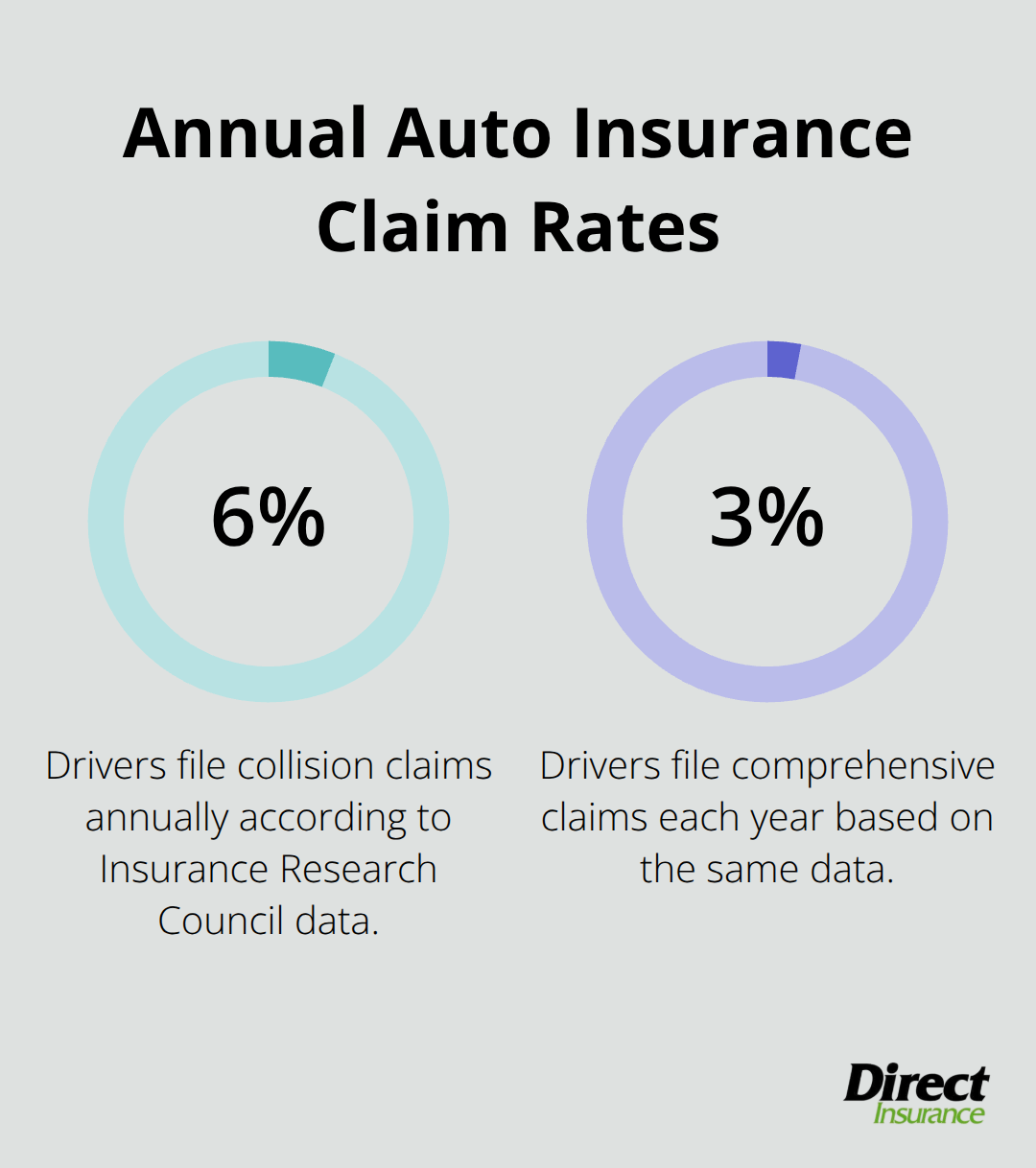

The math works strongly in favor of higher deductibles for drivers who file claims infrequently. Insurance Research Council data reveals that only 6% of drivers file collision claims annually, and just 3% file comprehensive claims each year. This means 94% of drivers pay higher premiums for lower deductibles they never use.

Drivers who choose $250 deductibles essentially pay an extra $400-600 annually to avoid an additional $750 out-of-pocket expense during rare claim events. The break-even point occurs when you file claims more than once every two years (which applies to fewer than 15% of all drivers according to National Association of Insurance Commissioners statistics).

When You Pay Your Deductible

You pay your deductible each time you file a covered claim, not annually like health insurance. Most insurers require you to pay the deductible directly to the repair shop before work begins, or they reimburse you after you pay it yourself. If repair costs fall below your deductible amount, you pay the entire bill out of pocket.

You won’t pay a deductible when another driver causes an accident and their liability insurance covers your repairs. Hit-and-run situations typically require you to pay your collision deductible unless you can identify the other driver.

Strategic Deductible Selection Based on Risk Factors

Your claim history and environment should determine your deductible strategy rather than popular choices. Drivers with clean records over five years should choose maximum deductibles ($1,000-2,000) to capture significant premium savings. Those who commute in heavy traffic areas or have filed claims within three years benefit from moderate deductibles ($500-750) that balance your monthly budget against potential out-of-pocket costs.

New drivers under 25 face higher accident rates and should stick with lower deductibles ($250-500) despite the premium penalty, since Insurance Institute for Highway Safety research shows drivers under 25 file claims at twice the rate of experienced drivers.

Final Thoughts

Auto insurance deductibles directly affect your premium costs and out-of-pocket expenses when accidents occur. Drivers with solid emergency funds and clean records benefit most from higher deductibles since they capture significant premium savings while they accept manageable financial risks. Those with limited savings or frequent claims should choose lower deductibles despite higher monthly costs.

Utah drivers face unique challenges that influence deductible decisions. Hail damage strikes frequently along the Wasatch Front, while animal collisions happen often in rural areas (especially during migration seasons). Your vehicle’s value, claim history, and emergency fund balance should guide your choice more than popular industry trends.

We at Direct Insurance Services help Utah families find the right balance between premium savings and financial protection. Our team works with top-rated carriers to provide personalized coverage solutions that fit your specific needs and budget. Contact our experienced agents to review your current deductibles and explore options that could reduce your insurance costs while they maintain appropriate protection levels.