How Auto Insurance with Accident Forgiveness Works

Getting into an accident doesn’t have to mean watching your insurance rates skyrocket for years. Auto insurance with accident forgiveness protects drivers from premium increases after their first at-fault claim.

We at Direct Insurance Services see many Utah drivers who could benefit from this coverage but don’t fully understand how it works. This protection can save you hundreds of dollars over time while providing valuable peace of mind on the road.

What Does Accident Forgiveness Actually Cover

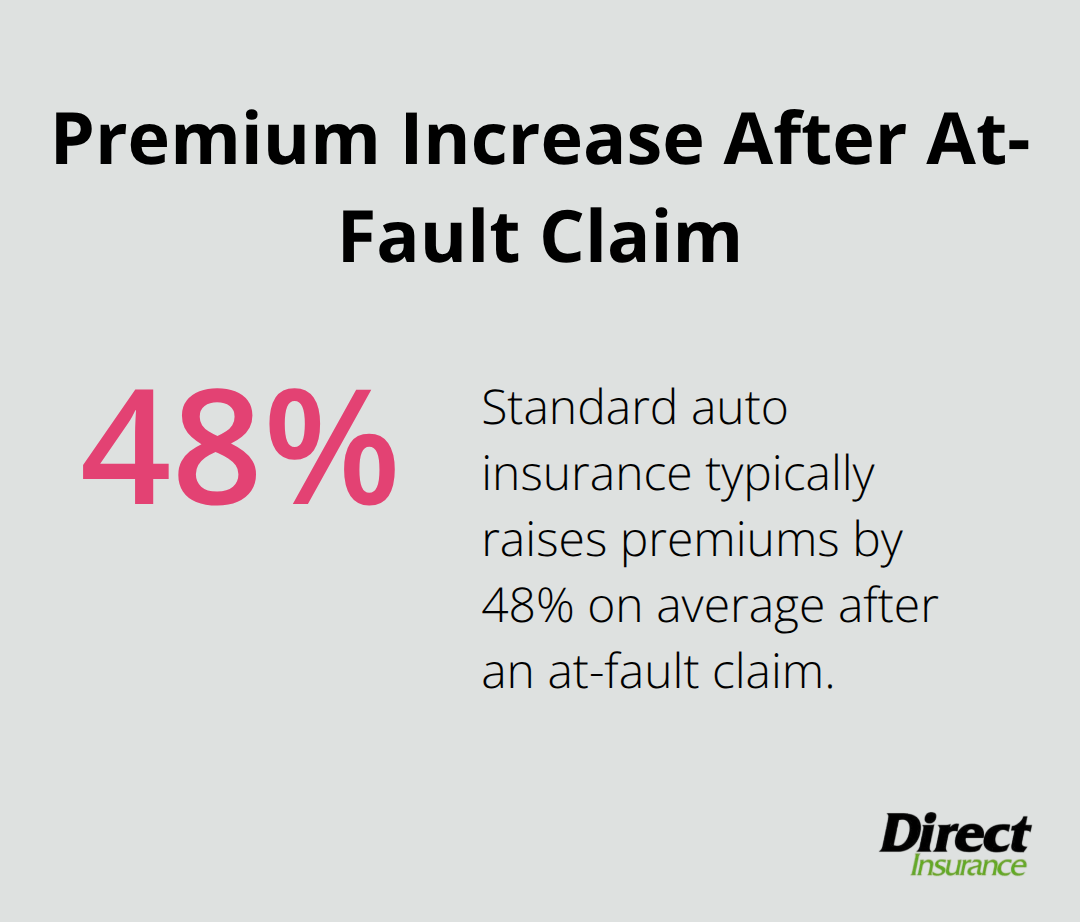

Accident forgiveness prevents your insurance rates from rising after your first at-fault accident. Standard auto insurance typically raises premiums by 48% on average after an at-fault claim, according to industry data. This coverage acts as a shield against these rate hikes and keeps your premium stable even when you file a claim for damage you caused.

The Cost Difference From Regular Coverage

Without accident forgiveness, drivers face significant premium increases after an at-fault accident. Progressive automatically includes Small Accident Forgiveness for claims under $500 at no extra cost in most states, while larger accident protection requires specific eligibility criteria. Liberty Mutual offers accident forgiveness after five years of clean driving and applies the benefit to all household drivers including teenagers. This differs dramatically from standard policies where any at-fault accident immediately triggers premium increases that persist for three to six years on your record.

Program Types Available Today

Insurance companies offer two main accident forgiveness structures. Earned forgiveness requires you to maintain a clean record for three to five years before you qualify, while purchased forgiveness can be added immediately for an additional premium. GEICO provides free accident forgiveness after five years of safe driving but allows drivers over 21 to purchase it earlier. Nationwide sells accident forgiveness after six months of coverage and permits two at-fault accidents every three years without rate increases.

Reset Requirements and Limitations

State Farm takes the longest approach and requires nine years of safe driving before it grants free forgiveness. Each program resets after use and typically requires another three to five years of accident-free driving before the benefit becomes available again. Most insurers apply forgiveness per policy rather than per individual driver, though specific terms vary between providers.

The next consideration involves understanding exactly who qualifies for these programs and what restrictions apply to your specific situation.

How Much Your Rates Actually Increase

An at-fault accident without forgiveness coverage raises your auto insurance premiums by an average of $1,127 annually according to Insurance Information Institute data. This increase typically persists for three to six years on your record, which means a single accident costs you $3,381 to $6,762 in additional premiums over time. These numbers explain why accident forgiveness becomes financially attractive even when it costs $100 to $200 extra per year upfront.

The Three-Year Premium Impact Reality

Your rate increase depends heavily on your insurance company’s specific policies and your state’s regulations. Allstate customers see average increases of 40% after their first at-fault claim, while Progressive’s data shows smaller increases for drivers with longer tenure. The severity matters too – a $15,000 property damage claim triggers larger premium hikes than a $2,000 fender bender (though both accidents stay on your record for the same duration).

State Rules That Change Everything

California prohibits accident forgiveness programs entirely, while Utah allows insurers to offer these benefits with different terms. Some states require insurers to reduce surcharges over time, but others permit companies to maintain higher rates for the full penalty period. Massachusetts drivers face different rules than Utah residents, which makes it essential to understand your local regulations before you purchase coverage.

Premium Calculation Factors

Insurance companies consider multiple factors when they calculate your post-accident rates. Your age, location, and previous claims history all influence the final increase percentage. Drivers under 25 typically face steeper penalties than experienced drivers (sometimes 60% or higher increases). The type of accident also matters – rear-end collisions often result in different rate adjustments than intersection accidents or single-vehicle crashes.

Understanding these rate structures helps you evaluate whether accident forgiveness eligibility requirements make financial sense for your specific situation.

Who Actually Qualifies for Accident Forgiveness

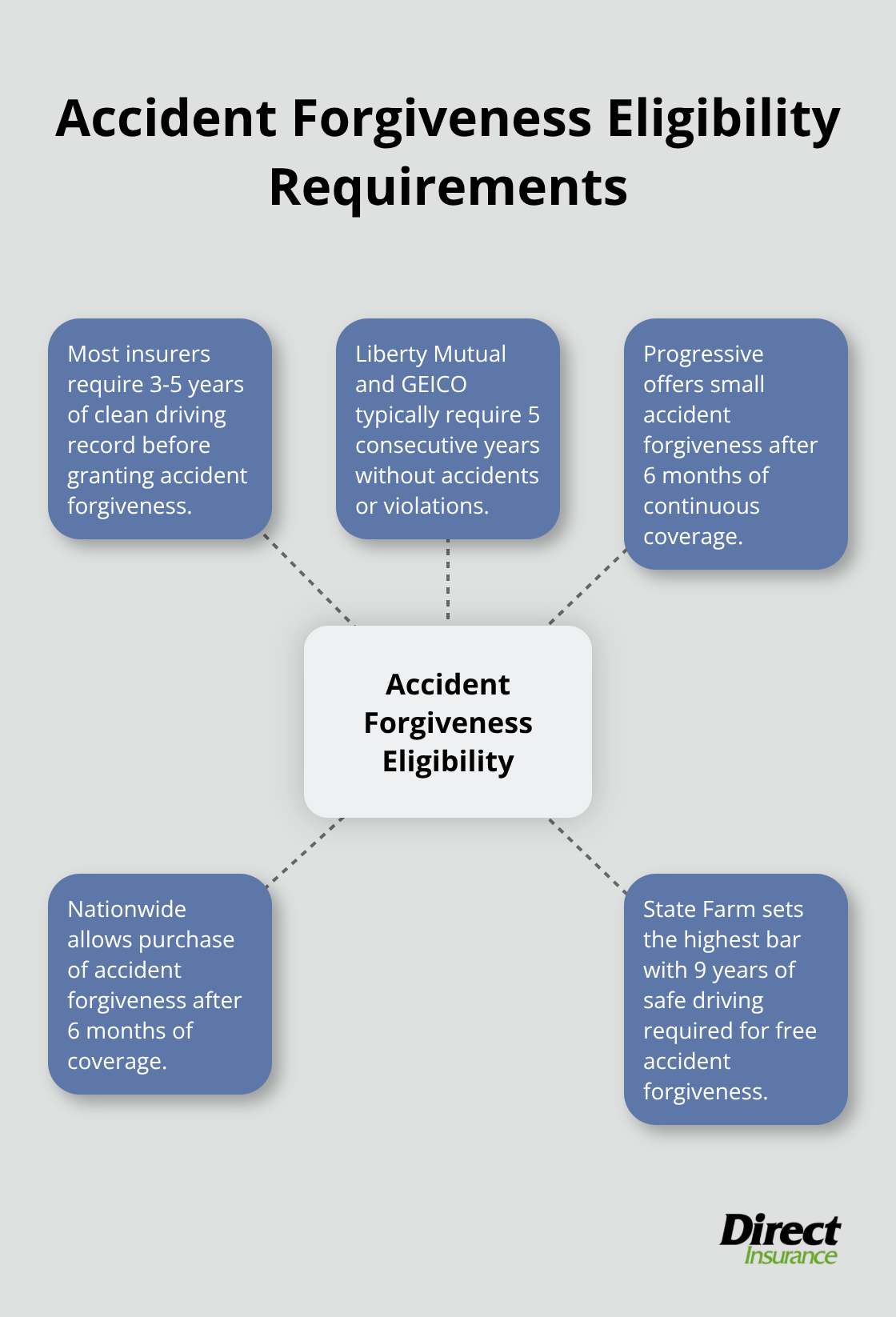

Most insurers demand a spotless record for three to five years before they grant accident forgiveness eligibility. Liberty Mutual requires five consecutive years without accidents or violations, while GEICO sets the same five-year standard but allows drivers over 21 to purchase coverage earlier based on their history. Progressive takes a different approach and requires only six months of continuous coverage to qualify for their small accident forgiveness program, though their large accident forgiveness demands five years of accident-free status. Nationwide permits drivers to purchase accident forgiveness after just six months of coverage, which makes them one of the most accessible options for newer customers.

Policy Duration Standards Across Major Insurers

State Farm sets the highest bar with nine years of safe operation required before they provide free accident forgiveness coverage. Erie Insurance requires three years as a customer before accident forgiveness becomes available, then offers complete forgiveness of all at-fault accidents after 15 years of loyalty. Travelers permits one accident and one minor violation every three years under their Responsible Driver plans, but you must maintain their coverage continuously to keep these benefits active. These loyalty requirements mean that you lose your eligibility timeline completely when you switch insurers (which makes accident forgiveness a strong retention tool for insurance companies).

Coverage Restrictions That Limit Protection

Accident forgiveness applies per policy rather than per individual driver in most cases, though Liberty Mutual extends coverage to all household members once the primary policyholder qualifies. The benefit typically covers only one accident every three to five years and companies often exclude drivers from safe driving discounts even when they forgive the rate increase. GEICO and Progressive limit their initial forgiveness programs to claims under $500, which requires additional tenure for larger accident protection. Most importantly, accident forgiveness does not cover your deductible costs and only prevents premium increases – you still pay out-of-pocket expenses when you file claims.

Age and Experience Requirements

Drivers under 25 face stricter qualification standards across most insurance companies. GEICO requires drivers to be over 21 before they can purchase accident forgiveness early, while other insurers may demand longer clean records for younger drivers. Some companies require at least six years of total experience before they consider any accident forgiveness benefits (regardless of how long you’ve held their specific policy). These age restrictions reflect the higher risk profile that insurers assign to younger drivers.

Final Thoughts

Auto insurance with accident forgiveness delivers substantial financial protection for Utah drivers who maintain clean records. This coverage prevents premium increases that average $1,127 annually after at-fault accidents and saves you thousands over three to six years. The protection becomes particularly valuable when you consider that 70% of drivers never experience accidents (which makes the upfront cost worthwhile for most responsible drivers).

The financial math works best for drivers who qualify for earned forgiveness after they maintain clean records for three to five years. Immediate purchase makes sense if you drive frequently or have teenage drivers on your policy who face higher risk profiles. Drivers with recent violations or claims should focus on record rebuilding before they invest in this coverage.

We at Direct Insurance Services help Utah families evaluate accident forgiveness options across multiple carriers to find the best fit for their specific situations. Our independent agency approach means we compare programs from different insurers and identify which eligibility requirements and benefits align with your history and budget. Contact Direct Insurance Services today to review your current coverage and explore accident forgiveness options that protect your financial future on Utah roads.