Auto Insurance Deductible Utah: How Much Should You Expect to Pay

Choosing an auto insurance deductible in Utah isn’t one-size-fits-all. Your deductible directly impacts both your monthly premium and what you’ll pay out of pocket when you file a claim.

At Direct Insurance Services, we help Utah drivers find the right balance between affordability and protection. This guide walks you through the numbers so you can make a decision that fits your budget and driving situation.

What Is a Deductible and Why It Matters

A deductible is the amount you pay out of your own pocket when you file a claim. Once you pay this amount, your insurance company covers the rest of the damage or loss, up to your policy limits. In Utah, deductibles typically range from $250 to $1,000 for both collision and comprehensive coverage, though you can choose higher amounts to lower your premium.

How Deductibles Affect Your Premium

The relationship between deductible and premium is straightforward: a $250 deductible costs more per month than a $1,000 deductible because the insurance company takes on more financial responsibility when your deductible is lower. According to data from The Zebra, Utah’s average full-coverage premium is $1,498 per year. This $500 figure is the most common choice among Utah drivers because it strikes a reasonable balance.

If you choose a $250 deductible instead, you’ll pay roughly 15-20% more annually. If you jump to a $1,000 deductible, you could save 20-30% on your premium. The key is understanding that your deductible choice directly affects both your monthly budget and your financial exposure after an accident.

The Real Cost of Choosing Wrong

Many Utah drivers pick their deductible based solely on which option saves them the most money each month. This is a mistake. If you choose a $1,000 deductible to save $50 per month but then have a fender bender that costs $3,000 to repair, you’re responsible for paying that full $1,000 before insurance kicks in.

If you don’t have $1,000 readily available, you’ll either need to take out a loan, use a credit card, or delay repairs. The financially smart approach is to choose a deductible you can actually afford to pay within 24 hours if needed. If your emergency fund sits at $2,000, a $1,000 deductible makes sense. If you have only $500 in savings, a $250 or $500 deductible is more realistic.

How Your Driving History Shapes Your Decision

Your driving history also influences how seriously you should consider this decision. Drivers with a clean record pay less for full coverage, but those with even one at-fault accident see their rates increase significantly. A speeding ticket adds roughly $392 to your annual cost.

If your driving record suggests you’re more likely to file a claim, a lower deductible protects you from larger out-of-pocket expenses when that claim comes. This protection becomes especially valuable when you factor in the actual cost of repairs and the financial strain a high deductible could create. Understanding your personal risk level helps you make a deductible choice that won’t leave you financially vulnerable after an accident.

What Really Determines Your Ideal Deductible

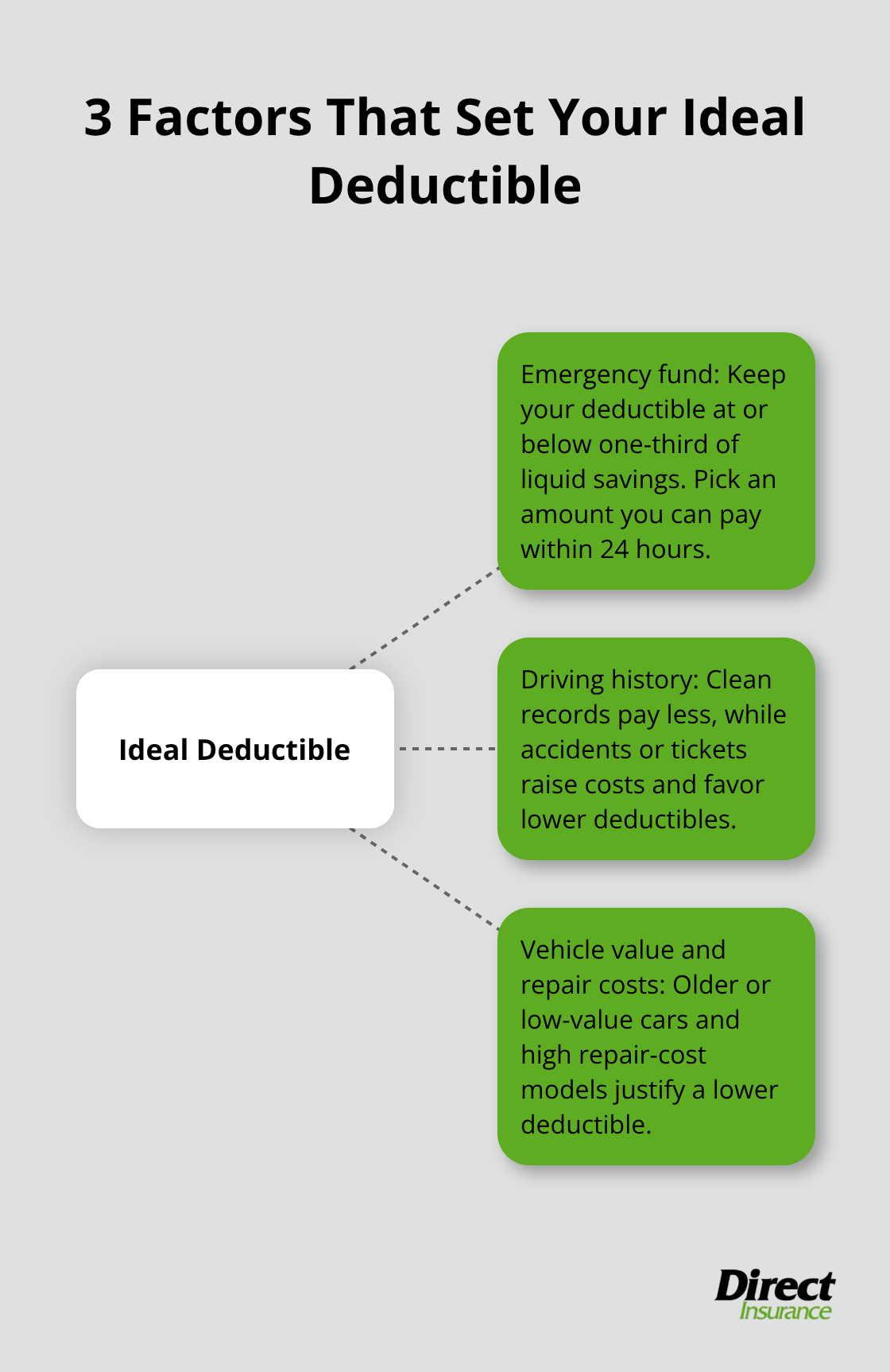

Your Emergency Fund Sets the Foundation

Your emergency fund forms the foundation of any smart deductible decision, and this is where most Utah drivers go wrong. If you have $3,000 in savings, a $1,000 deductible leaves you vulnerable because a single accident wipes out a third of your financial safety net. According to AutoInsurance.com data, drivers with poor credit pay around $4,217 per year for full coverage compared to $2,431 for those with good credit, which means your ability to handle unexpected costs varies significantly.

The practical rule that works best is this: your deductible should never exceed one-third of your liquid savings. If you have $1,500 available, a $500 deductible makes sense. If you have $4,500, a $1,000 or $1,500 deductible becomes realistic. This approach protects you from financial strain while still allowing you to capture premium savings.

How Your Driving History Changes the Math

Your driving history adds another layer to this calculation. Drivers with clean records pay $2,431 annually for full coverage in Utah, but one at-fault accident raises that to $3,460 per year according to AutoInsurance.com. If you’ve already had an accident or received a speeding ticket, the math changes dramatically.

A speeding violation costs roughly $392 extra per year, and that sits on top of your base premium. When your driving history suggests higher risk, the insurance company already prices in the likelihood that you’ll file a claim. In this situation, a lower deductible protects you financially when-not if-that claim happens. A driver with one accident in the past three years should seriously consider a $500 deductible despite the higher monthly cost, because the probability of filing another claim is measurably higher than someone with a spotless record.

Vehicle Age and Repair Costs Matter More Than You Think

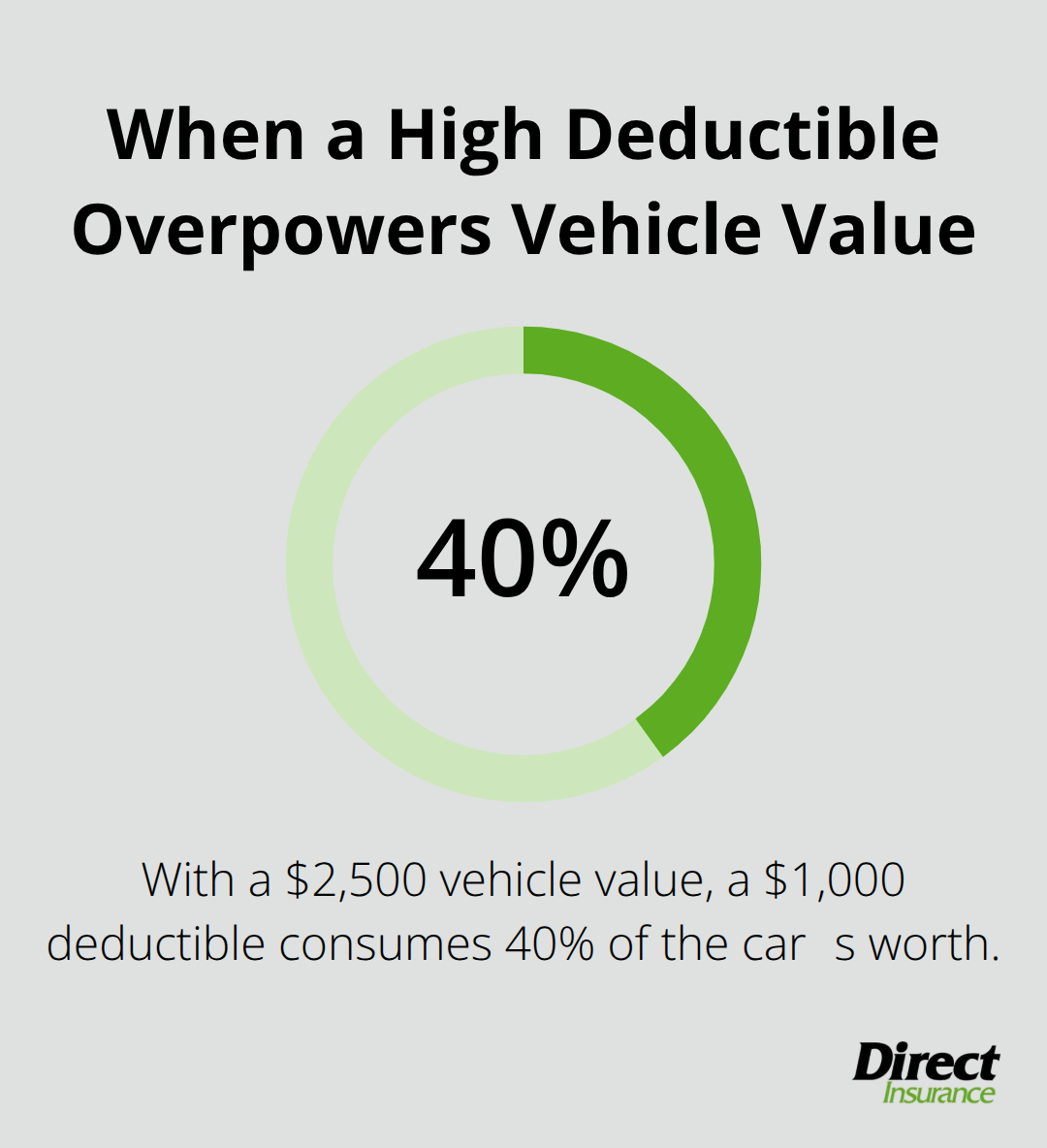

Your vehicle’s age and market value determine whether a high deductible even makes financial sense. If you drive a 2015 Honda Civic worth $8,000, a $1,000 deductible is reasonable. If you drive a 2006 Honda Civic worth $2,500, that same $1,000 deductible becomes reckless because it represents 40% of your car’s entire value.

A collision that costs $2,200 to repair means you pay $1,000 out of pocket while your insurer covers $1,200-that’s an unfavorable split. For older vehicles with lower market values, a $250 or $500 deductible protects you from situations where repair costs approach your vehicle’s total worth. Vehicle type also affects both repair costs and how often you might file a claim. A Tesla Model 3 with a minor fender bender might cost $3,500 to repair due to specialized parts and labor, while the same accident in a Toyota Camry costs $1,800.

If you own a vehicle with expensive repair costs, a lower deductible offsets that financial burden. The data from AutoInsurance.com shows full-coverage premiums vary by vehicle: a BMW 330i costs $2,661 annually while a Toyota Camry costs $2,188. That $473 difference reflects repair costs built into the premium. If you’re driving the more expensive-to-repair vehicle, your deductible choice becomes even more critical to your financial security.

Putting It All Together for Your Utah Situation

These three factors-your emergency fund, your driving history, and your vehicle’s value-work together to determine your ideal deductible. A driver with $5,000 in savings, a clean driving record, and a 2020 Toyota Camry can comfortably choose a $1,000 deductible. That same driver with one accident in the past two years should drop to $500. A driver with only $2,000 in savings should never choose a $1,000 deductible, regardless of how much money it saves each month.

The goal isn’t to find the lowest possible premium. The goal is to find the deductible that protects your financial stability while keeping your monthly costs manageable. Once you understand how these factors interact, you’re ready to explore the specific strategies that help you save money on your overall auto insurance without sacrificing the protection you actually need.

Strategies for Choosing the Right Deductible

Calculate Your Break-Even Point

Most Utah drivers treat deductible selection like a math problem with one correct answer. It’s not. Your deductible choice is a personal financial decision that depends entirely on what happens in the months between now and your next claim. The real strategy isn’t about picking the lowest premium or the safest deductible-it’s about understanding the actual trade-off you’re making and whether you can live with the consequences.

Start with a simple calculation. If a $500 deductible costs you $85 per month and a higher deductible costs you $65 per month, you’re spending an extra $240 per year for that lower deductible. This means you need to file a claim worth more than $740 in damages before the lower deductible saves you money. According to AutoInsurance.com, drivers with clean records file claims far less frequently than those with accidents in their history. A driver with zero incidents in five years might never reach that break-even point. Conversely, a driver with one accident already on record has proven they’re statistically more likely to file again, making that $240 annual investment in a lower deductible genuinely worthwhile.

Assess What You Can Actually Afford

The calculation shifts based on your actual risk profile, not on how much money you want to save each month. Next, you need to calculate what you can realistically afford to pay within one day of an accident. Most people overestimate this number. They think about their total savings and divide it by three, but they forget about next month’s rent, their kids’ school expenses, and the medical bills they might accumulate if the accident involves an injury.

The honest approach is to look at what’s actually available in your checking account right now. Assume you can access that amount without borrowing, and use that as your maximum deductible. If you have $800 available today, a $1,000 deductible is dangerous. If you have $3,500, a $1,000 deductible works. This isn’t theory-it’s the difference between handling a claim smoothly and facing financial stress when you need to pay your deductible and still cover your other obligations.

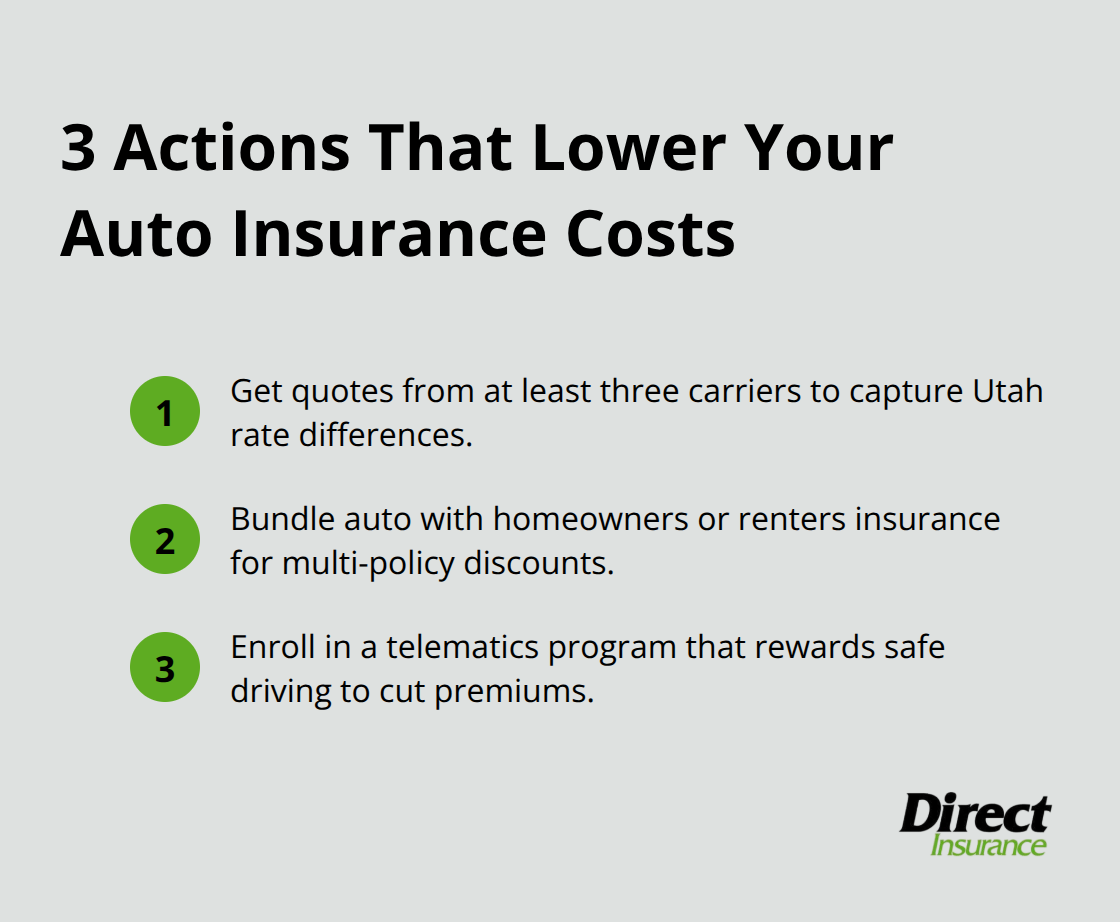

Three Actions That Lower Your Overall Costs

Beyond the deductible itself, three concrete actions lower your overall auto insurance costs regardless of your deductible choice. First, get quotes from at least three different carriers because rate variation in Utah is significant. GEICO’s average full-coverage premium sits around $1,622 annually while State Farm averages $4,036 for identical coverage according to AutoInsurance.com data. Shopping could save you $2,400 per year.

Second, bundle your auto policy with homeowners or renters insurance because insurers consistently discount customers who consolidate coverage. Third, ask specifically about telematics programs that monitor your driving. Safe drivers who enroll can reduce rates further. These three actions often save more money than optimizing your deductible alone, and they carry no financial risk if you’re ever in an accident.

Final Thoughts

Your auto insurance deductible in Utah depends on three factors: what you can afford to pay immediately after an accident, how your driving history affects your risk level, and whether your vehicle’s repair costs justify a lower deductible. The lowest premium doesn’t always protect you best-a $1,000 deductible saves money monthly, but only if you have the cash available when you need it. A $500 deductible costs more upfront yet protects you from financial strain when an accident happens.

Shopping quotes from multiple carriers delivers bigger savings than optimizing your deductible alone, since rate variation across Utah is substantial. GEICO’s average full-coverage premium sits around $1,622 annually while State Farm averages $4,036 for identical coverage, meaning you could save thousands by comparing options. Bundling your auto policy with homeowners or renters insurance consistently reduces your overall costs, and enrolling in telematics programs that monitor safe driving behavior lowers your premiums further.

Your financial situation changes, your vehicle ages, and your driving history evolves, which means your auto insurance deductible Utah needs shift over time. Contact Direct Insurance Services today to review your current deductible and explore how bundling or other strategies could lower your costs without sacrificing the protection your situation requires. We work with top-rated carriers to help you find coverage that matches both your budget and your actual protection needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation