Best Mobile Home Insurance Companies

Mobile home insurance protects your property and finances, but finding the right coverage isn’t simple. The best mobile home insurance companies offer different protection levels, pricing, and customer support options that can significantly impact your wallet and peace of mind.

At Direct Insurance Services, we’ve reviewed what matters most when selecting a policy. This guide walks you through coverage types, rate factors, and how to compare providers so you can make an informed decision.

Coverage Options and Types

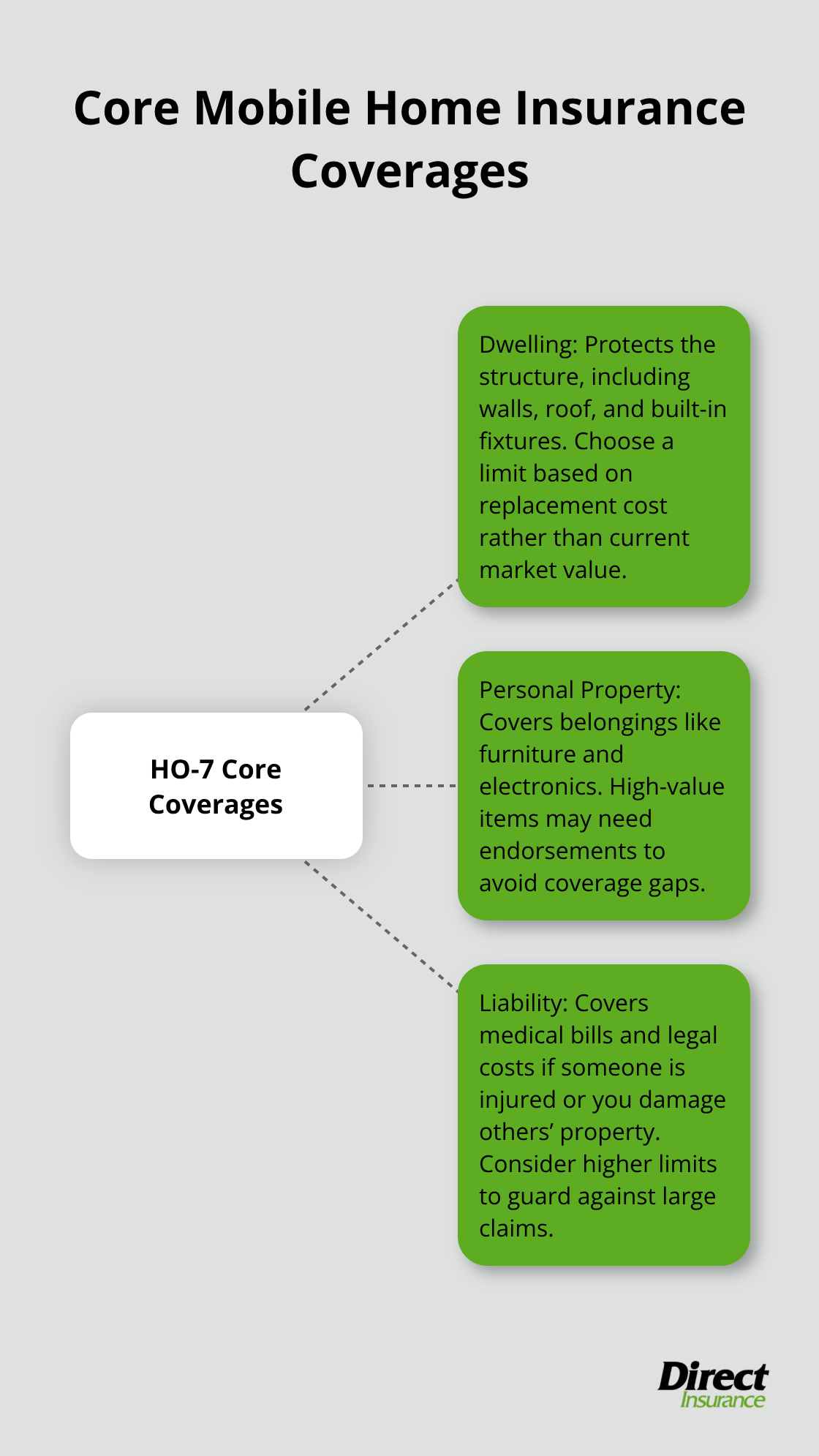

Dwelling Coverage Protects Your Structure

Mobile home insurance uses the HO-7 policy form, which differs from standard homeowners coverage because it accounts for the unique construction and value of manufactured homes. Dwelling coverage protects the structure itself, including the walls, roof, and built-in fixtures, but the amount you select matters more than most people realize. According to MarketWatch Guides, dwelling coverage is one of the three core components alongside personal property and liability. Your dwelling coverage limit should reflect your home’s replacement cost, not its current market value-this distinction is important because mobile home repair costs can spike quickly.

If your home was built before 1976, insurers typically charge more because older construction standards mean higher repair expenses.

Personal Property Coverage Protects Your Belongings

Personal property coverage protects your belongings inside the home, from furniture to electronics, and you need to calculate this accurately. Many homeowners underestimate their belongings’ value and end up underinsured. Walk through your home and itemize high-value items like jewelry, collectibles, or sporting equipment, which may require separate endorsements for full protection. This inventory process takes time but prevents costly gaps in your coverage when you file a claim.

Liability Protection Shields Your Finances

Liability coverage is where most mobile homeowners make dangerous mistakes. This protection covers medical bills and legal costs if someone is injured on your property or if you accidentally damage someone else’s property. Standard liability limits typically range from $100,000 to $300,000, but you should consider the higher end because medical costs have exploded-a single serious injury lawsuit can easily exceed $250,000. MarketWatch data shows that liability and medical payments to others are standard across all major insurers, but many people accept minimum limits without questioning whether those limits match their actual risk.

Additional Protections and Endorsements

Additional protections like water backup coverage, earthquake endorsements, and identity theft protection vary significantly between carriers. American Modern stands out for flexibility, offering coverage for mobile homes used as rentals or vacant properties, while Foremost includes relocation damage coverage if your home is moved. The practical takeaway: do not assume all policies are identical. Request quotes that specify coverage limits and endorsements so you can compare apples to apples, and increase your liability limit if you frequently host guests or live in an area with higher litigation costs. Understanding these coverage options positions you to evaluate which insurers actually match your specific protection needs.

Factors Affecting Mobile Home Insurance Rates

Location Determines Your Premium More Than Any Other Factor

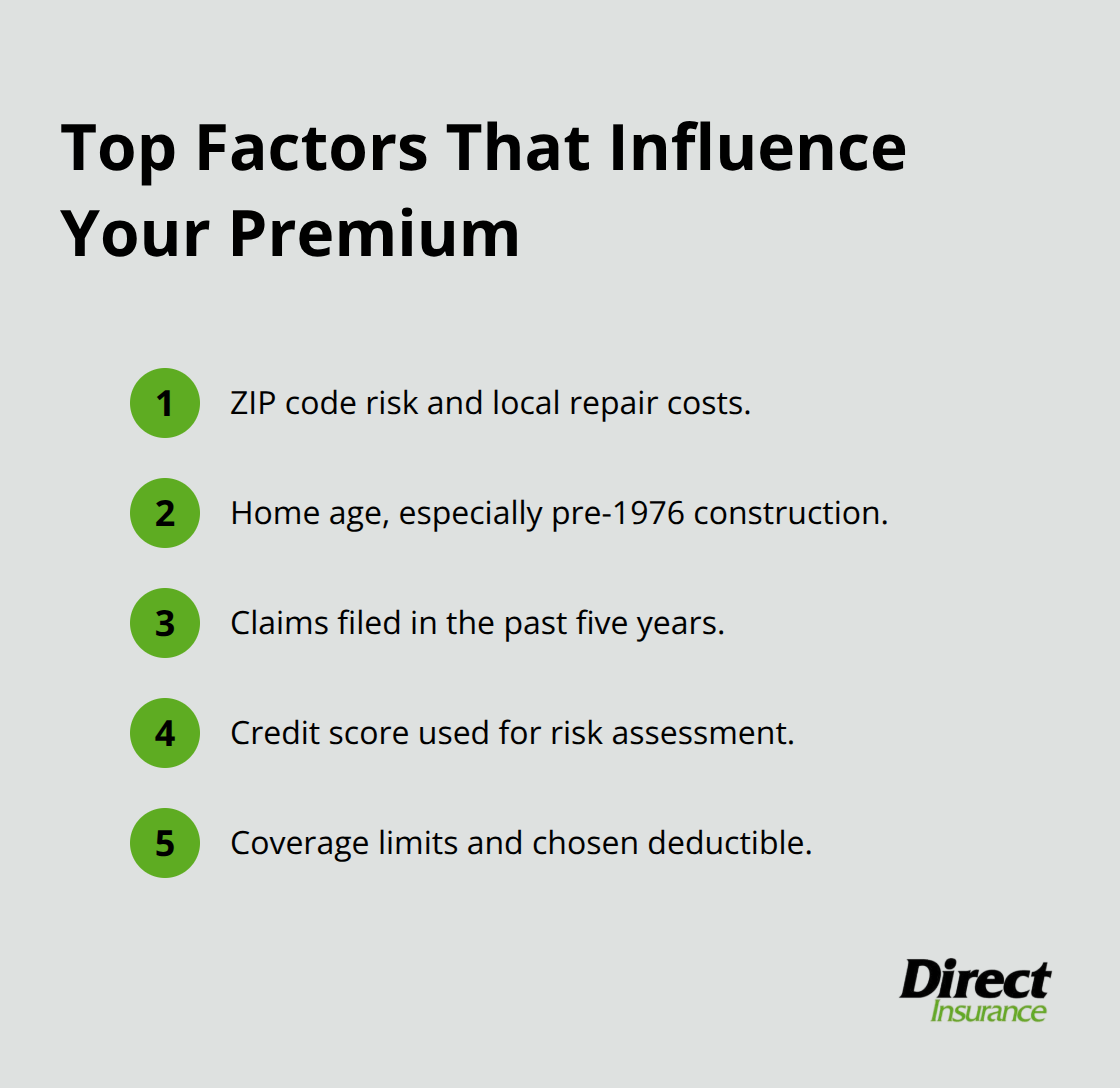

Your ZIP code is the single biggest factor that determines what you pay for mobile home insurance, and it’s not even close. Location affects premiums because environmental hazards and regional repair costs vary dramatically across the country. A mobile home in hurricane-prone areas of Texas costs significantly more to insure than the same home in Indiana, according to MarketWatch Guides. Beyond hurricanes, your location exposes you to wildfires, hail, tornadoes, and flooding. When you request a quote, insurers pull your specific ZIP code data to assess these risks, which is why two identical homes in different states have vastly different premiums. If you’re considering moving your mobile home, factor insurance costs into your relocation decision. Some areas add $500 to $1,000 annually compared to lower-risk regions.

The Age of Your Home Creates a Hard Pricing Divide

The age of your mobile home creates a hard divide in pricing that most owners don’t anticipate. Homes built before 1976 cost substantially more to insure because they don’t meet modern HUD standards established that year. Older construction means higher repair expenses when damage occurs, so insurers charge premiums that reflect this reality. If your home was built in 1975 versus 1980, you’ll notice a meaningful difference in quotes. This age threshold matters more than most homeowners realize when they shop for coverage.

Your Claims History and Credit Score Impact Rates

Your claims history in the last five years directly impacts rates, and this is where owner behavior matters. A single claim filed within the past five years raises your premium across nearly all carriers. Your credit score influences rates too, with higher scores typically resulting in lower premiums since insurers correlate credit behavior with claim likelihood. When you shop for quotes, lenders may pull your credit, so understand that this factor affects your final price. These two elements work together to shape what insurers consider your overall risk profile.

Coverage Limits and Deductibles Give You Control

Coverage limits and deductible selection give you direct control over your costs. Increasing your deductible from $500 to $1,000 lowers your annual premium, but this only makes sense if you can actually afford to pay that higher amount when a loss occurs. Your dwelling coverage limit should match your home’s replacement cost, not its market value. According to MarketWatch Guides, typical annual mobile home insurance costs range from $750 to $2,400, but this range reflects the cumulative effect of all these factors combined.

How to Compare Quotes Effectively

The practical strategy is to request quotes with identical coverage limits and deductibles across multiple insurers, then adjust only the deductible to find your comfort zone between premium cost and financial risk tolerance. This approach reveals which carriers offer the best rates for your specific situation rather than comparing misleading headline numbers. Once you understand what drives your costs, you’re ready to evaluate which insurance companies actually deliver the coverage and customer support you need.

How to Choose the Right Mobile Home Insurance Provider

Request Quotes with Identical Coverage Details

Start with quotes from at least three to five different insurers using identical coverage limits and deductibles, then compare the actual dollar amounts side by side. This step is non-negotiable because the difference between carriers can easily exceed $500 annually for the same protection. According to MarketWatch Guides, typical annual costs range from $300 to $1,200, but your specific quote depends entirely on which company you select and how you structure your coverage. When you gather quotes, specify your exact dwelling limit, personal property coverage amount, liability limit, and deductible so you’re comparing real apples to apples.

Many people make the mistake of comparing headline prices without confirming that coverage matches, which leads to false savings estimates. One of the most effective ways to find affordable coverage involves comparing quotes from multiple providers because it forces insurers to provide written comparisons, and you’ll have documentation to reference later. The companies that make quoting difficult or refuse to provide detailed breakdowns are signaling that customer transparency isn’t their priority.

Evaluate Claims Processing Speed and Approval Rates

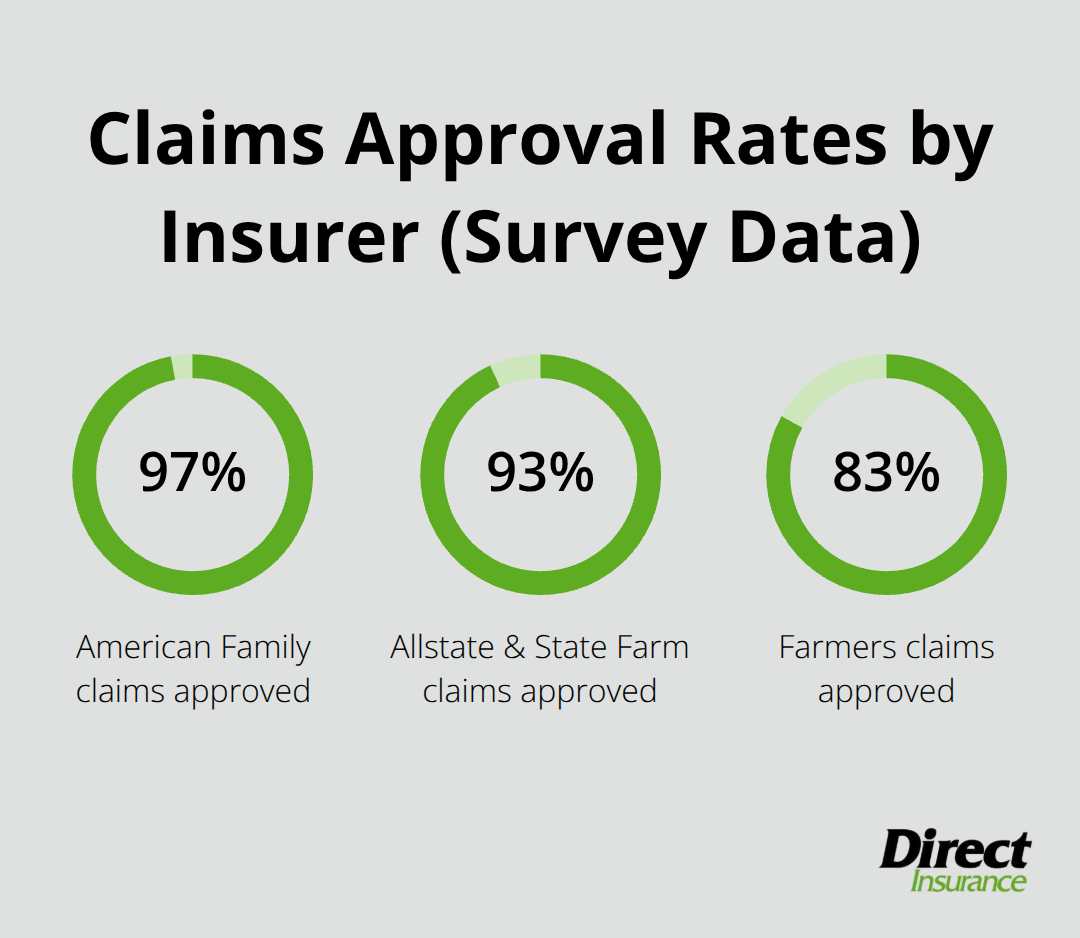

Beyond price, evaluate how each company handles claims because that’s when you actually need insurance to work. American Family processes claims in zero to six days with approximately 97 percent approval rates according to survey data, while Allstate and State Farm typically settle claims within one to two weeks with approval rates around 93 percent.

Farmers takes one to two weeks but carries an 83 percent approval rate, which is notably lower.

These differences matter enormously when your home suffers damage and you need funds quickly for repairs or temporary housing. Contact each company’s claims department directly and ask specific questions about their process, required documentation, and average settlement time. Check whether they offer mobile app claim filing since this speeds up the process considerably, though Foremost notably lacks this feature despite being MarketWatch’s top pick.

Compare Discount Opportunities and Coverage Features

Discount opportunities vary significantly between carriers, so don’t skip this step. Allstate offers discounts for homeowners aged 55 and above plus original mobile home owner discounts, while State Farm focuses on bundling discounts when you insure multiple properties with them. American Family includes hidden water damage and matching siding coverage as standard endorsements rather than optional add-ons, which effectively reduces your coverage gaps without additional premium costs.

Foremost provides relocation coverage if your home needs to be moved, and American Modern allows coverage flexibility for rental or vacant mobile homes. Your job is to match these specific features against your actual situation, not against what marketing materials claim matters most.

Final Thoughts

Selecting the right mobile home insurance requires you to balance three critical elements: adequate coverage that protects your actual assets, competitive pricing that fits your budget, and reliable claims support when you need it most. The best mobile home insurance companies deliver all three, but they don’t always come from the same carrier. Foremost excels at specialized mobile home protection with relocation coverage, American Family processes claims faster than competitors, and State Farm provides extensive local agent support that matches your specific situation rather than chasing the lowest headline price.

Contact Direct Insurance Services or request quotes directly from at least three carriers using identical coverage specifications. Specify your dwelling limit, personal property amount, liability coverage, and deductible so comparisons remain accurate. Ask each company about claims processing time, approval rates, and available discounts specific to your situation, since this process takes a few hours but prevents years of regret over inadequate protection or overpaid premiums.

Select the carrier that balances your coverage needs with acceptable pricing and responsive claims support once you’ve gathered quotes and evaluated customer service options. Mobile home insurance isn’t optional if you finance your home or live in a community requiring it, and it shouldn’t be treated as a commodity purchase based solely on price. Your decision today determines whether insurance actually protects you when damage occurs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation