How to Get Hazard Insurance for Your Home Loan

Your mortgage lender requires hazard insurance, but many homeowners don’t understand what they’re actually buying. Without proper coverage, a single fire, theft, or storm could leave you financially devastated.

At Direct Insurance Services, we help homeowners navigate hazard insurance for their home loans so they get the protection they need at a price that makes sense. This guide walks you through everything from understanding coverage types to avoiding costly mistakes.

What Hazard Insurance Actually Covers

The Core Protection Your Lender Requires

Hazard insurance is the dwelling coverage portion of your homeowners policy that protects your home’s structure against specific perils your lender requires you to carry. This isn’t a separate standalone product-it’s embedded within a standard homeowners insurance policy. When your lender says you need hazard insurance before closing on your mortgage, they’re requiring you to protect the dwelling itself, which serves as collateral for their loan. The coverage typically includes fire, lightning, theft of the structure, vandalism, hail, windstorm damage, explosions, falling objects, and damage from burst pipes or appliances.

What the Numbers Tell You About Cost

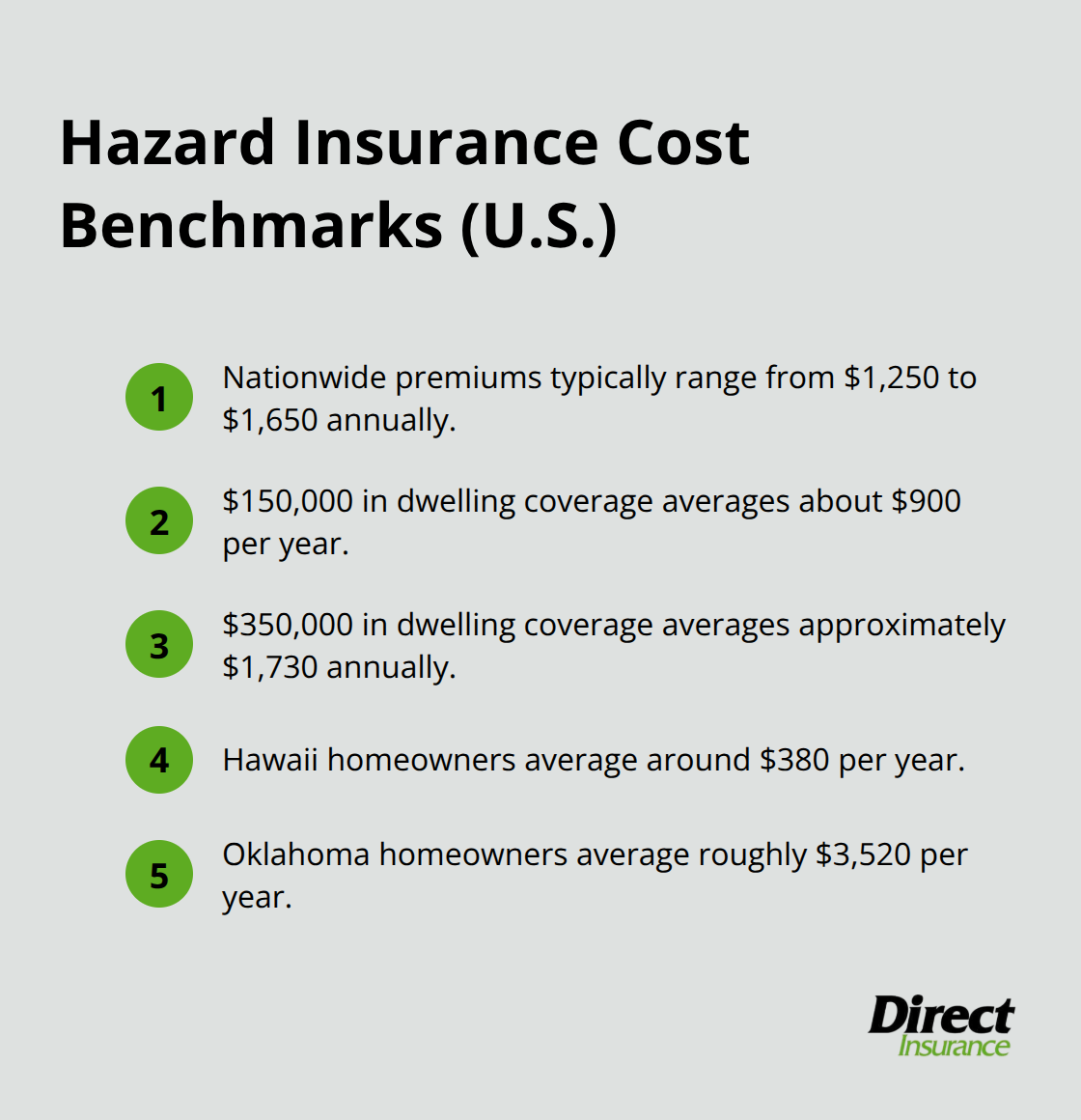

Hazard insurance premiums nationwide typically range from about $1,250 to $1,650 annually, though this varies dramatically by location and home value. A home with $150,000 in dwelling coverage averages around $900 per year, while $350,000 in coverage averages approximately $1,730 annually. Your location drives much of this cost-Hawaii homeowners pay around $380 per year on average, while Oklahoma residents pay roughly $3,520, according to Angi’s analysis. This massive difference reflects regional exposure to wildfires, high winds, tornadoes, hurricanes, hail, and freezing temperatures.

Critical Coverage Gaps You Must Know

What hazard insurance explicitly does not cover matters just as much as what it does: standard policies exclude flood damage and earthquake damage, requiring separate insurance if you live in at-risk areas. You cannot rely on your hazard coverage to protect against these perils, no matter how severe the damage becomes.

Why Your Lender Won’t Let You Skip It

Your mortgage lender mandates hazard insurance because they have a financial interest in protecting the property securing their loan. Most lenders require proof of coverage before finalizing the mortgage and often place your insurance premium into an escrow account, spreading the annual cost across your monthly mortgage payments. This requirement remains in place for as long as you carry the mortgage-you cannot remove hazard coverage while still owing money on the home. The lender will typically specify a minimum coverage amount, usually tied to your home’s replacement cost or loan amount, whichever is greater.

What Happens After You Pay Off Your Mortgage

After you pay off your mortgage entirely, the lender’s requirement ends, though keeping hazard coverage remains wise to protect your asset from fire, theft, and weather-related damage. At this point, you control your coverage decisions and can adjust limits or deductibles to match your actual needs. Understanding how your lender calculates minimum coverage requirements helps you shop effectively and avoid both underinsurance and overpaying for unnecessary protection-which brings us to how you actually shop for the right policy.

Shopping for Hazard Insurance Without Overpaying

Calculate Your Home’s True Replacement Cost

Getting an accurate dwelling coverage amount starts with understanding your home’s actual replacement cost, not its market value. These are two completely different numbers. A home might sell for $400,000 but cost $550,000 to rebuild from the ground up because reconstruction labor and materials differ from what buyers pay on the open market. Contact local contractors or use the National Association of Home Builders’ cost data for your region to estimate realistic rebuild expenses. This number becomes your target for dwelling coverage and directly determines your premium.

Request Multiple Quotes to Understand Regional Pricing

Once you know your replacement cost figure, request quotes specifying that exact coverage amount from at least three carriers. The reason you need multiple quotes isn’t to find the absolute cheapest option-it’s to understand how different insurers price risk in your specific location. Two carriers might quote $1,200 and $1,650 for identical coverage on the same home simply because they weight regional hazards differently. One insurer may view your area’s tornado exposure as high-risk while another focuses more on fire danger. Getting three to five quotes reveals these variations and prevents you from accidentally choosing an insurer that underprices your actual risk profile, which could lead to claim denials down the road.

Match Your Deductible to Your Financial Reality

Your deductible choice directly impacts your monthly escrow payment and out-of-pocket costs after a loss, so this decision deserves serious thought. A higher deductible results in a lower premium, which are your known out-of-pocket expenses. However, you’ll pay that deductible difference yourself if you file a claim. The math only works in your favor if you can comfortably absorb that amount without financial strain. Many homeowners make the mistake of choosing a high deductible to save money on their premium, then face hardship when a significant loss occurs. Work backward from your emergency fund-if you have $5,000 saved, a $1,000 deductible makes sense. If you have $1,500 saved, stick with $500.

Verify Your Lender’s Specific Coverage Requirements

Also verify that your lender has no minimum coverage requirements beyond what state law or your loan terms specify. Some lenders require dwelling coverage equal to 80 percent of your home’s replacement cost; others demand 100 percent. Knowing this requirement prevents you from shopping for less coverage than your lender will actually accept, which wastes time and delays your closing. These lender-specific rules vary significantly, so contact your loan officer directly rather than making assumptions based on what you’ve heard from friends or family. Once you align your deductible with your financial capacity and confirm your lender’s exact requirements, you’re ready to identify which mistakes most homeowners make during this process-and how to sidestep them entirely.

Common Mistakes That Cost Homeowners Thousands

Underinsuring Your Property to Save on Monthly Payments

The biggest mistake homeowners make is underinsuring their property to save money on premiums. You calculate your home’s replacement cost at $450,000, but then you buy only $350,000 in dwelling coverage to keep the monthly escrow payment lower. This creates a catastrophic gap. When a major fire destroys your home, your insurer pays up to $350,000, leaving you responsible for the remaining $100,000 out of pocket. Worse, some policies include coinsurance clauses that penalize you for being underinsured-if you carry only 80 percent of your home’s replacement cost, the insurer may pay only a percentage of your claim rather than the full amount.

According to Angi’s analysis, homes with $150,000 in coverage average $900 annually, while $350,000 in coverage averages $1,730. That $830 yearly difference sounds significant until you face a $100,000 shortfall after a loss. The math doesn’t work. You need dwelling coverage that matches your actual replacement cost, period. Skipping this step because you want lower monthly payments is false economy that destroys your financial security the moment a covered peril strikes.

Ignoring Your Location’s Specific Natural Hazards

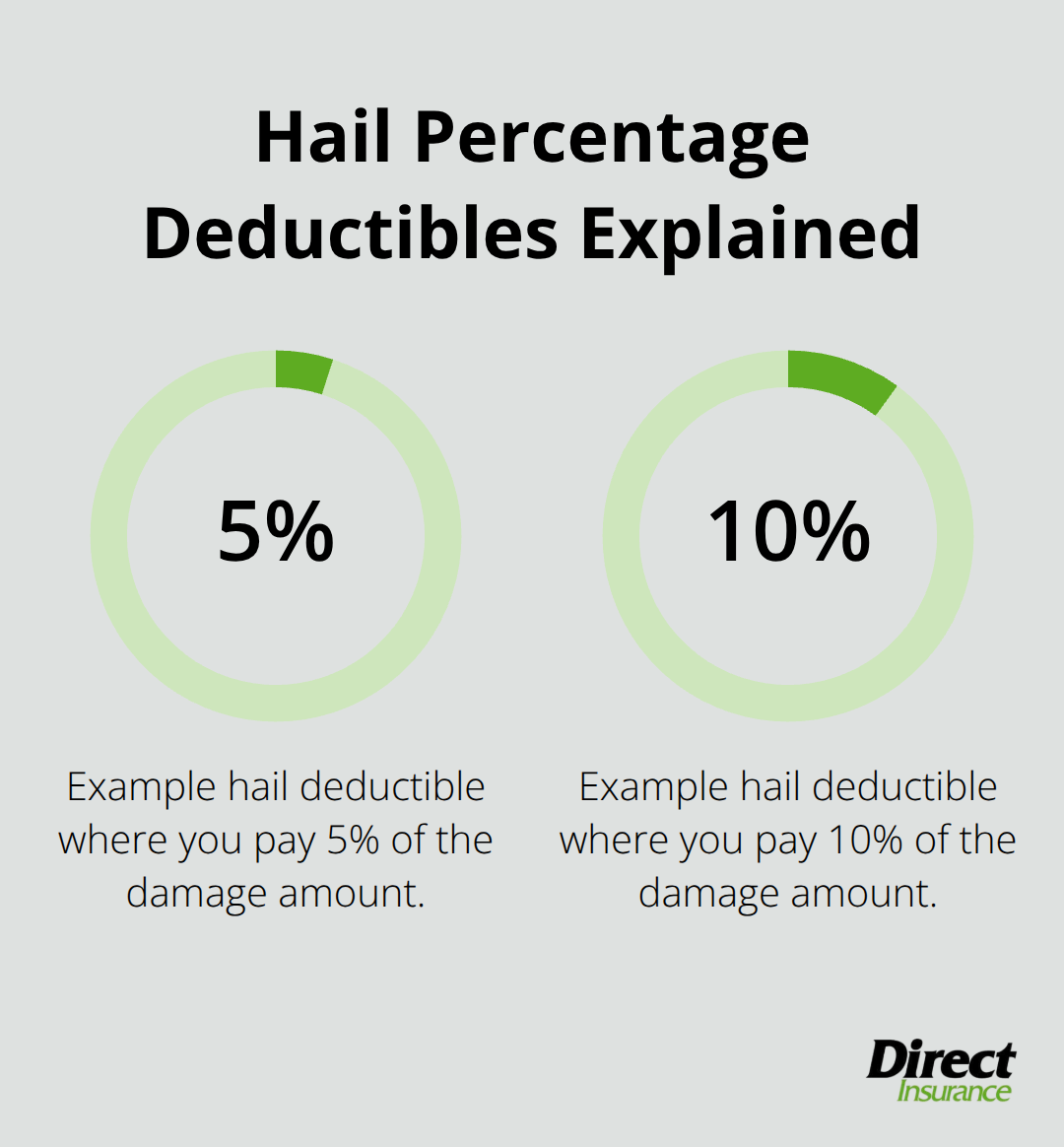

Your second critical error is ignoring the specific natural hazards your location faces. You live in a region where hail damage costs homeowners an average of $11,000 per claim, yet you never verified whether your policy actually covers hail at full limits or applies a separate deductible for hail damage. Some carriers impose percentage deductibles for hail-meaning you pay 5 or 10 percent of the damage amount rather than a flat deductible-which can cost thousands more than a standard deductible.

Similarly, if you live in a wildfire-prone area and your home sits near vegetation, some insurers restrict or exclude coverage for fire damage, or they charge significantly higher premiums. You must request quotes that specifically address your area’s dominant hazards, then ask each carrier how they handle those perils. Don’t assume standard coverage applies uniformly across all insurers or all regions.

Skipping Annual Policy Reviews

Hazard insurance isn’t a set-it-and-forget-it product. Your home’s value increases as you make improvements, your area’s risk profile changes as development occurs, and your financial situation evolves. You should review your policy annually-at minimum when you refinance your mortgage or complete major renovations. If you added a deck, new roof, or finished basement, your replacement cost increased, but your coverage limit probably didn’t adjust automatically.

Contact your insurance agent each year to verify your dwelling coverage still reflects your home’s current replacement cost. Most homeowners skip this step and discover mid-claim that they’re underinsured by tens of thousands of dollars. An annual review conversation with your agent should be standard practice, not an afterthought.

Final Thoughts

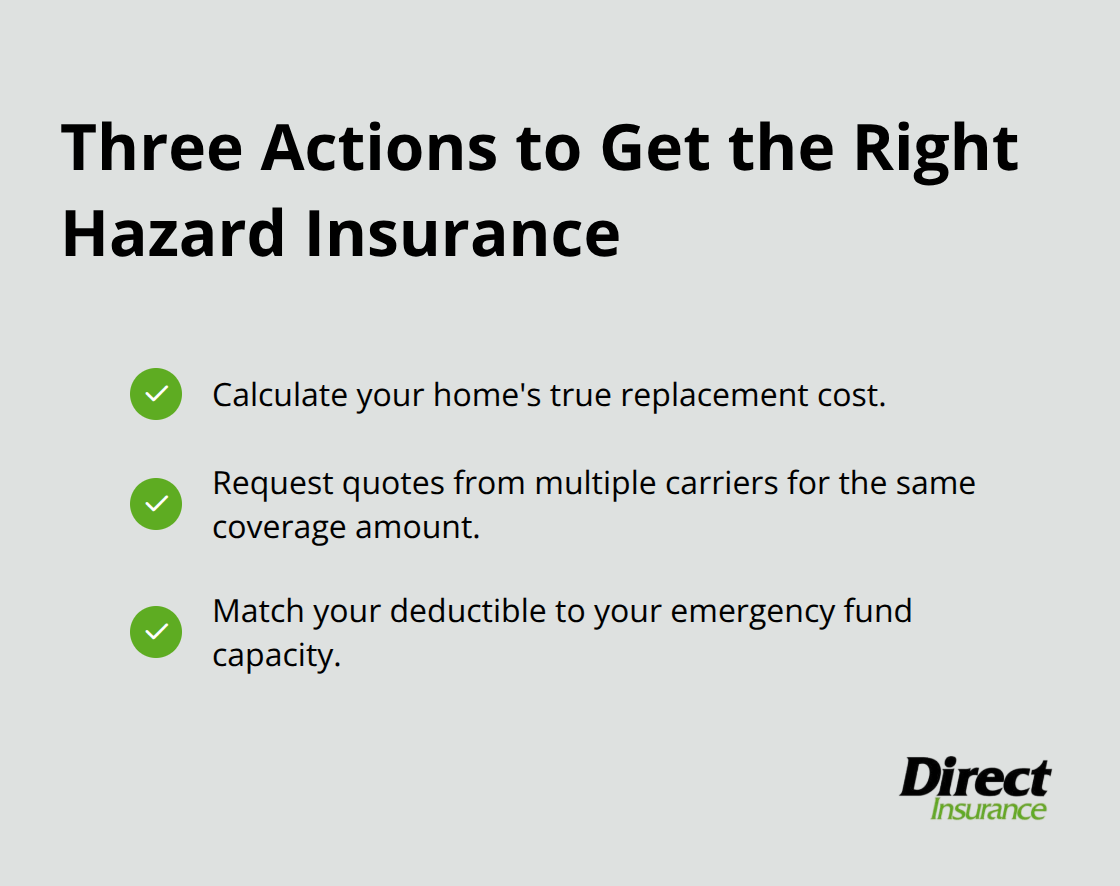

Getting hazard insurance for your home loan requires three concrete actions: calculate your home’s actual replacement cost, request quotes from multiple carriers, and match your deductible to your emergency fund. Your lender mandates this coverage to protect their investment, and you benefit equally by shielding yourself against fire, theft, windstorms, and other covered perils.

The mistakes that cost homeowners thousands-underinsuring to lower monthly payments, ignoring your location’s specific natural hazards, and skipping annual policy reviews-are entirely preventable if you take these steps seriously.

The difference between adequate protection and financial disaster often comes down to whether you spent an hour calculating your true replacement cost and requesting three quotes. Underinsuring by $100,000 to save $830 annually destroys your financial security the moment a major loss occurs. Your location’s dominant hazards (whether hail, wildfire, or wind damage) demand specific attention when you shop, not generic assumptions about what standard coverage includes.

At Direct Insurance Services, we help Utah homeowners navigate hazard insurance for their home loans by connecting you with carriers that match your actual needs. Visit us to get started with a quote that reflects your home’s replacement cost and your area’s specific hazards.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation