What Is the Average Cost of Homeowners Insurance?

Homeowners insurance is one of your biggest housing expenses, yet most people have no idea what they should actually be paying. The average cost of homeowners insurance varies wildly depending on where you live and the specifics of your home.

At Direct Insurance Services, we’ve helped thousands of homeowners understand their insurance costs and find better rates. This guide breaks down exactly what affects your premiums and shows you concrete ways to save money.

What Really Drives Your Homeowners Insurance Premium

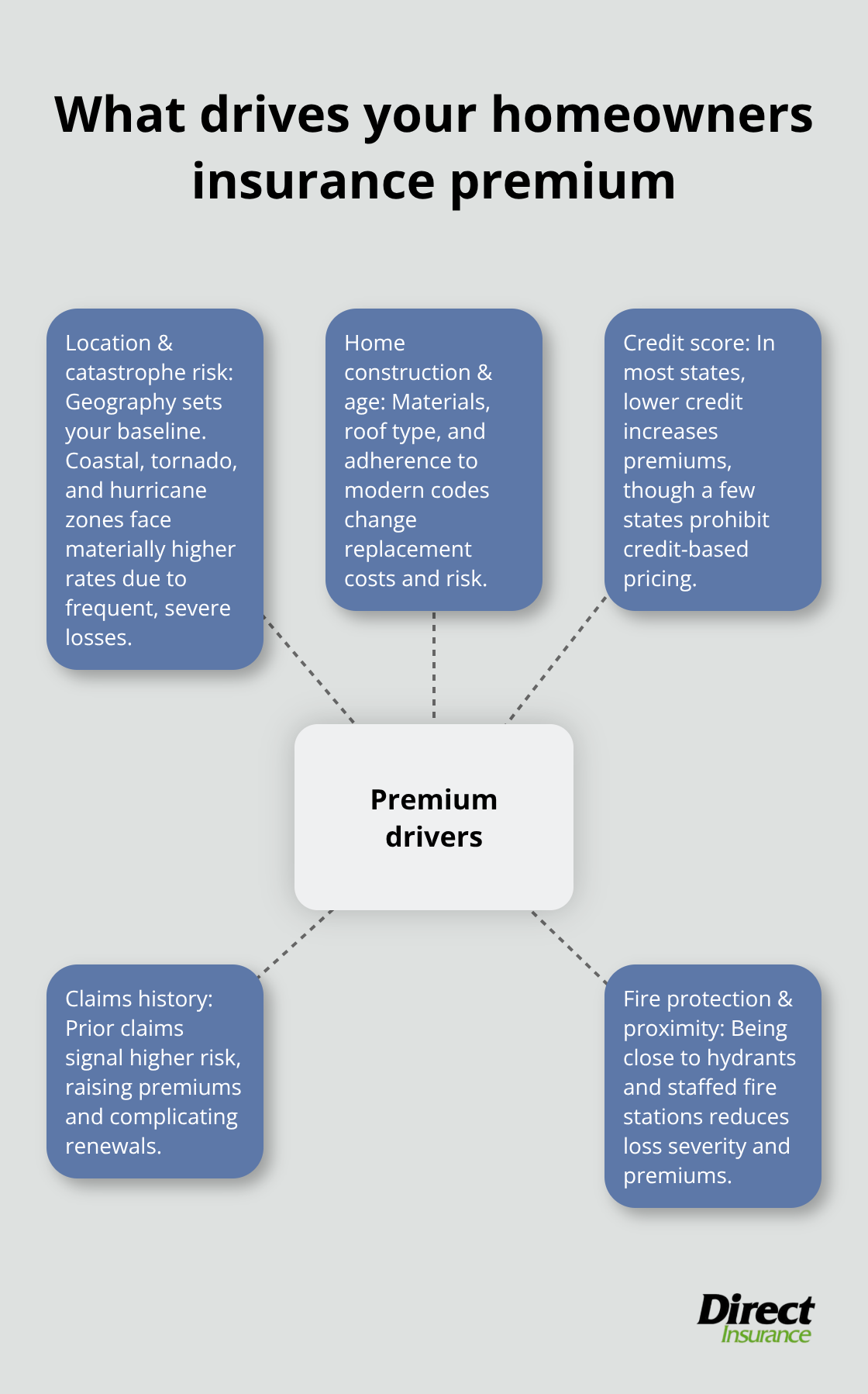

Location and Natural Disaster Risk Set the Baseline

Your location is the single most important factor determining what you pay for homeowners insurance, and it’s not even close. If you live in Nebraska, you pay about $6,587 per year for $300,000 in dwelling coverage according to Bankrate’s 2025 analysis. Move to Vermont and that same coverage costs just $827 annually. That’s an 88% difference purely because of geography.

Natural disaster risk is the culprit. States like Louisiana, Florida, and Oklahoma face constant threats from hurricanes, tornadoes, and severe weather. The U.S. property and casualty industry logged over $100 billion in natural-disaster losses in 2024 alone, and insurers pass those costs directly to policyholders in high-risk areas. NOAA documented more than 25 billion-dollar weather and climate disasters in 2024, making premium increases unavoidable in vulnerable regions.

Even within states, ZIP code matters dramatically. Oklahoma City averages around $5,554 yearly while Portland, Oregon sits at just $1,051 for identical coverage. Proximity to fire departments and hydrants lowers your premium because faster response times reduce claim severity. Living near woods or brush increases wildfire risk and raises costs.

Coastal properties face hurricane exposure premiums that inland homes never see.

Home Construction and Age Impact Your Rate

Your home’s replacement cost and construction materials directly impact your premium because they determine what the insurer would need to pay if total loss occurs. A brick or concrete block home typically costs less to insure than wood-frame construction due to fire risk differences. Roof type matters too-hip roofs resist wind better than gable roofs and can lower your premium.

Older homes built before modern building codes generally cost more to insure. A home built in 1959 might cost $3,285 annually while a 2020 build runs $2,182 for the same $300,000 coverage. Insurers view older construction as riskier due to outdated materials and systems.

Credit Score and Claims History Affect Your Bottom Line

Your credit score influences premiums in most states significantly. Poor credit can push your annual premium to $5,122 while excellent credit drops it to $2,160 for identical coverage-a 137% difference. Some states like California, Maryland, and Massachusetts prohibit credit-based pricing, but most don’t.

Prior claims are permanent marks against you. One wind damage claim raises premiums about 9% compared to a clean history. Multiple claims signal higher future risk and can make renewal difficult or expensive. Understanding these factors helps you identify which elements you can control and which ones require strategic planning when shopping for coverage.

How Much You’ll Pay by State

The Most Expensive States for Homeowners Insurance

Nebraska residents pay the most for dwelling coverage cost by state, according to Bankrate’s analysis. Louisiana, Florida, Oklahoma, and Kansas round out the top five most expensive states. These states face relentless tornado, hurricane, and severe weather exposure that drives claims costs through the roof. If you live in one of these states, accept that your baseline premium will be significantly higher than the national average-and shop aggressively to avoid overpaying on top of that reality.

The Most Affordable States for Homeowners Insurance

Vermont, Delaware, Alaska, New Hampshire, and West Virginia offer the most affordable homeowners insurance rates. These states enjoy lower disaster risk and lower reconstruction costs, which directly translates to savings. The difference between the most and least expensive states can be substantial for the same dwelling coverage amount. Even within single states, ZIP code variation can be dramatic, with some areas costing significantly more than others for identical coverage.

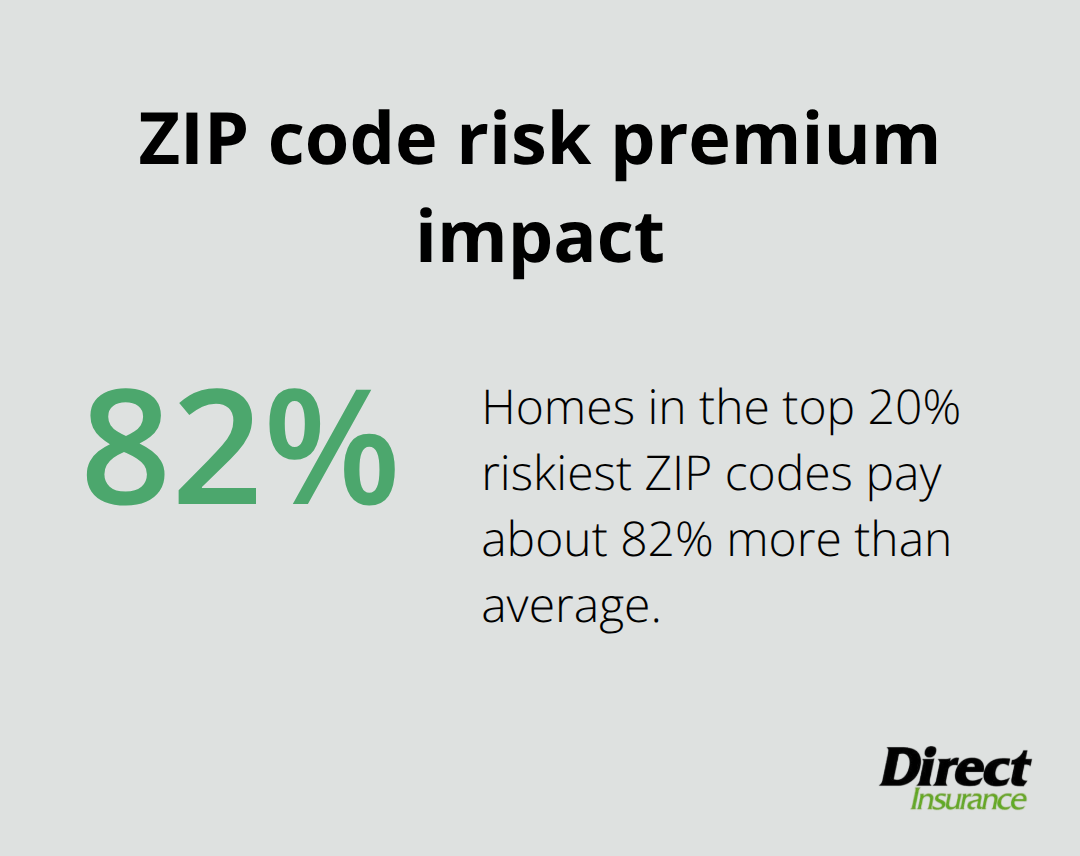

Why Your Specific Address Matters More Than Your State

Your specific location within your state drives your rate far more than broad regional assumptions. Different regions within states face wildly different tornado, wildfire, flood, and hurricane risks depending on geography. Properties in the top 20% riskiest ZIP codes pay about 82% more than average, meaning your specific address matters enormously.

Regional Risk Patterns That Shape Your Premium

The Great Plains and Southeast face tornado and hurricane exposure that makes insurers nervous. Coastal properties trigger automatic premium increases due to hurricane and storm surge risk. Mountain and forest regions face wildfire exposure that raises rates significantly. Meanwhile, northern states with stable weather patterns and lower natural disaster frequency enjoy dramatically lower premiums. If you’re shopping for a home or considering a move, factor in that a house in a high-risk ZIP code will cost thousands more annually to insure-this isn’t negotiable with your carrier, only avoidable through location choice. Understanding these regional patterns helps you anticipate what your premium will look like before you commit to a property.

How to Actually Lower Your Homeowners Insurance Premium

Increase Your Deductible to Cut Costs Fast

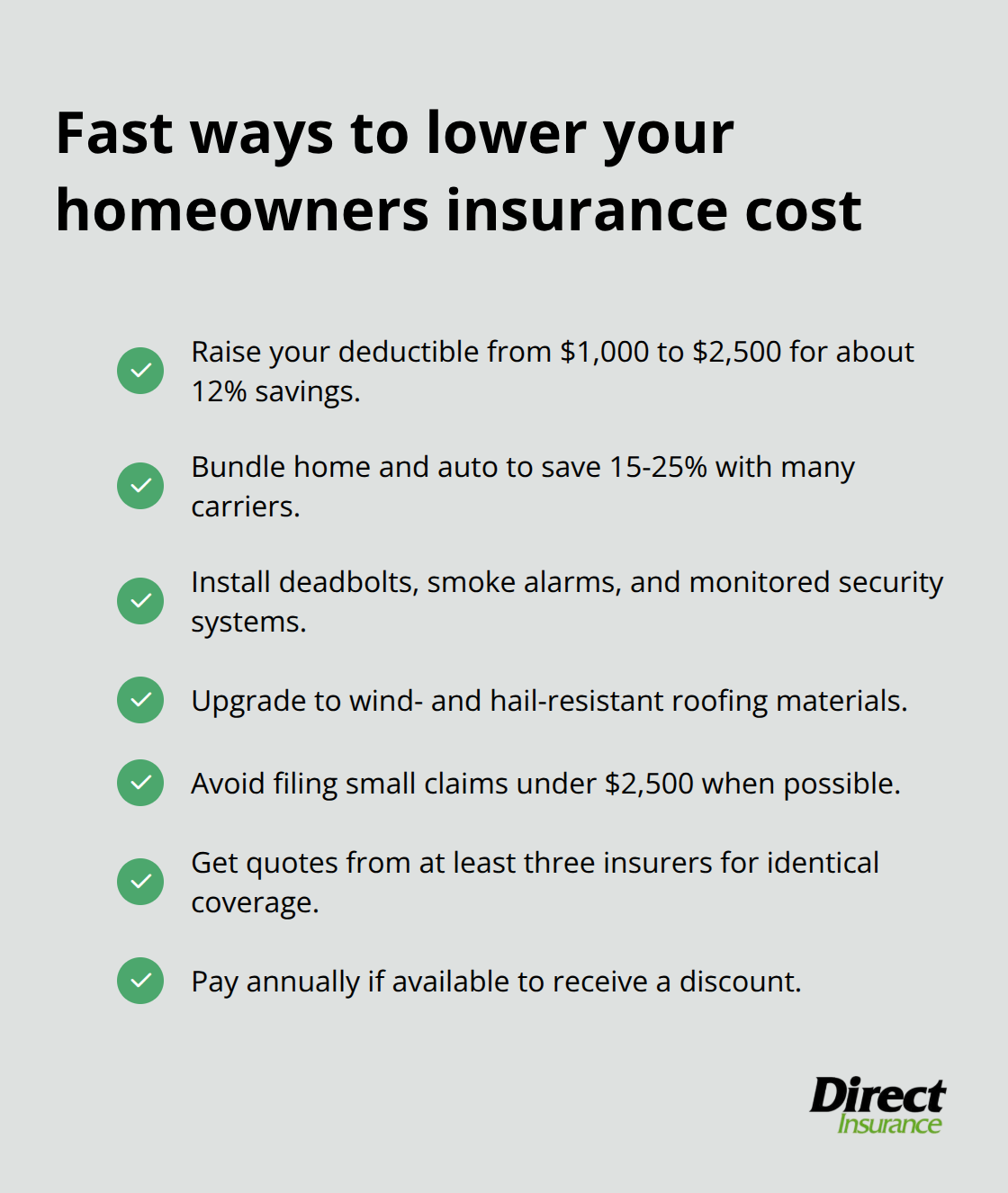

The most effective way to lower your premium is increasing your deductible from $1,000 to $2,500, which reduces your annual cost by about 12% according to NerdWallet analysis. This works because you absorb more risk yourself, and insurers reward that trade-off with meaningful discounts. The key is choosing a deductible you can actually afford to pay out-of-pocket if a claim happens-don’t stretch beyond your emergency fund.

Stack Discounts Through Bundling and Home Upgrades

Bundling your homeowners policy with auto insurance from the same carrier typically saves 15-25% on your combined premiums, making this one of the easiest wins available. Many insurers require you to ask for this discount explicitly, so don’t assume it applies automatically. Home security upgrades deliver concrete savings too. Deadbolt locks, smoke alarms, fire extinguishers, and monitored security systems all qualify for discounts that can stack together.

If you live in a hurricane-prone area, installing hurricane shutters or hurricane-resistant laminated glass to industry standards often triggers mandatory discounts that insurers must offer. Roof upgrades matter significantly-replacing old asphalt shingles with wind and hail-resistant materials can lower your premium while protecting your actual home.

Leverage Your Credit Score and Claims History

Your credit score influences rates substantially in most states, with poor credit potentially costing you 137% more than excellent credit for identical coverage. If your credit has improved, notify your insurer and request a re-evaluation; some carriers will reduce your premium or issue refunds if your score has climbed. However, don’t obsess over credit-based pricing alone since three states prohibit it entirely, and other factors drive your rate higher anyway.

Avoid filing small claims under $2,500 since one claim raises your premium about 9% and stays on your record for years, making that small payout cost you thousands more long-term. If you’ve had claims in the past, ask your insurer about claims-free discounts or ask when your record will age off their system. The industry standard is three to five years, so understanding your timeline helps you plan when to shop again for better rates.

Shop Multiple Carriers and Pay Strategically

Shopping around for quotes from at least three different insurers is non-negotiable if you want the best price. Premiums vary wildly between carriers for identical coverage-comparing quotes takes two hours and can save you $500-1,000 annually. Progressive’s network shows policies ranging from $1,090 to $3,354 yearly for the same coverage level, proving that carrier choice matters enormously. When you shop, get quotes with identical dwelling coverage amounts, deductibles, and liability limits so you’re comparing apples to apples.

Some of the cheapest carriers include USAA (restricted to military families), Auto-Owners, American Family, Nationwide, and Erie, but availability varies by state and your specific situation. Don’t pay your premium monthly if you can pay annually-some insurers offer discounts for upfront annual payment. This simple payment choice can reduce your total cost without sacrificing coverage.

Final Thoughts

Your homeowners insurance premium reflects factors you cannot control-location, home age, natural disaster risk-and factors you absolutely can control through deliberate action. The average cost of homeowners insurance ranges from $827 yearly in Vermont to $6,587 in Nebraska for identical $300,000 dwelling coverage, yet your specific ZIP code matters far more than your state. Within that reality, you hold real leverage to reduce what you pay through strategic choices.

The most effective moves deliver immediate results without sacrificing protection. Raising your deductible cuts costs by 12% instantly, while bundling auto and homeowners policies saves 15-25% on your combined premiums. Installing security systems or upgrading your roof qualifies you for stacked discounts that compound together, and shopping quotes from at least three carriers typically reveals $500-1,000 in annual savings because premiums vary wildly between insurers for identical coverage. These actions work together-combining a higher deductible with bundling and home upgrades can easily reduce your premium by 30-40%.

We at Direct Insurance Services help Utah homeowners navigate these decisions and find coverage that fits your needs and budget without pressure. Contact Direct Insurance Services to get personalized quotes and expert guidance on protecting your home affordably.