Landlord vs Home Insurance: Understanding the Distinctions

Are you a homeowner or a landlord? Understanding the difference between landlord insurance and home insurance is vital for protecting your property investment.

At Direct Insurance Services, we often encounter confusion about these two types of coverage. This blog post will clarify the key distinctions between landlord insurance vs home insurance, helping you make an informed decision about your property protection needs.

What Sets Landlord and Home Insurance Apart?

When it comes to protecting your property, the type of insurance you need depends on how you use it. The wrong policy can leave property owners exposed to significant risks.

Property Coverage: Beyond Bricks and Mortar

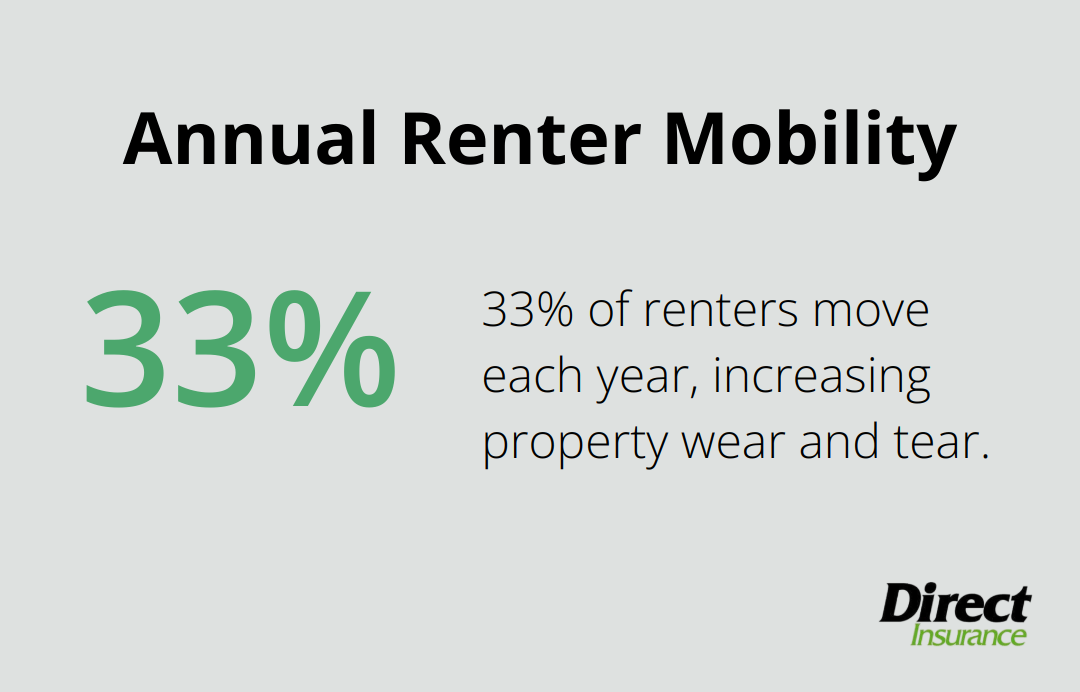

Landlord insurance typically offers broader property coverage than standard home insurance. This is because rental properties face unique risks. A study by the National Multifamily Housing Council found that 33% of renters move each year, which increases wear and tear on properties.

Landlord policies often cover things like malicious damage by tenants or their guests (which home insurance doesn’t usually include).

Liability: Shielding Against Tenant-Related Risks

Liability protection in landlord insurance is tailored to the specific risks of renting out property. According to the Insurance Information Institute, about one in 1,100 homeowners policies has a liability claim related to the cost of lawsuits for bodily injury or property damage. This is why landlord policies often have higher liability limits than home insurance. They also cover scenarios like a tenant slipping on an icy walkway (a situation not covered under a standard homeowners policy if you’re renting out the property).

Income Protection: Securing Your Rental Revenue

One of the most significant differences is loss of income coverage. If your rental property becomes uninhabitable due to a covered event, landlord insurance can reimburse you for lost rent. The National Association of Realtors reports that the average monthly rent in the U.S. is $1,702. Without this coverage, a few months of repairs could mean a substantial financial hit.

Home insurance doesn’t offer this protection because it’s designed for owner-occupied properties. If you consider renting out your home, even temporarily, it’s important to switch to a landlord policy to avoid gaps in coverage.

Personal Property: Coverage Differences

Homeowners insurance typically includes extensive coverage for personal belongings, such as furniture, clothing, and electronics. Landlord insurance, on the other hand, provides limited coverage for personal property. It usually only covers items that the landlord keeps on the property for maintenance or tenant use, like appliances or landscaping equipment.

Policy Costs: Understanding the Price Difference

Landlord insurance generally costs more than homeowners insurance. This price difference reflects the increased risks associated with rental properties. Factors that influence the cost include the property’s location, age, and condition, as well as the extent of coverage selected.

The distinctions between landlord and home insurance highlight the importance of choosing the right policy for your specific situation. In the next section, we’ll take a closer look at the key components of landlord insurance to help you understand what this type of coverage entails.

What Does Landlord Insurance Cover?

Comprehensive Property Protection

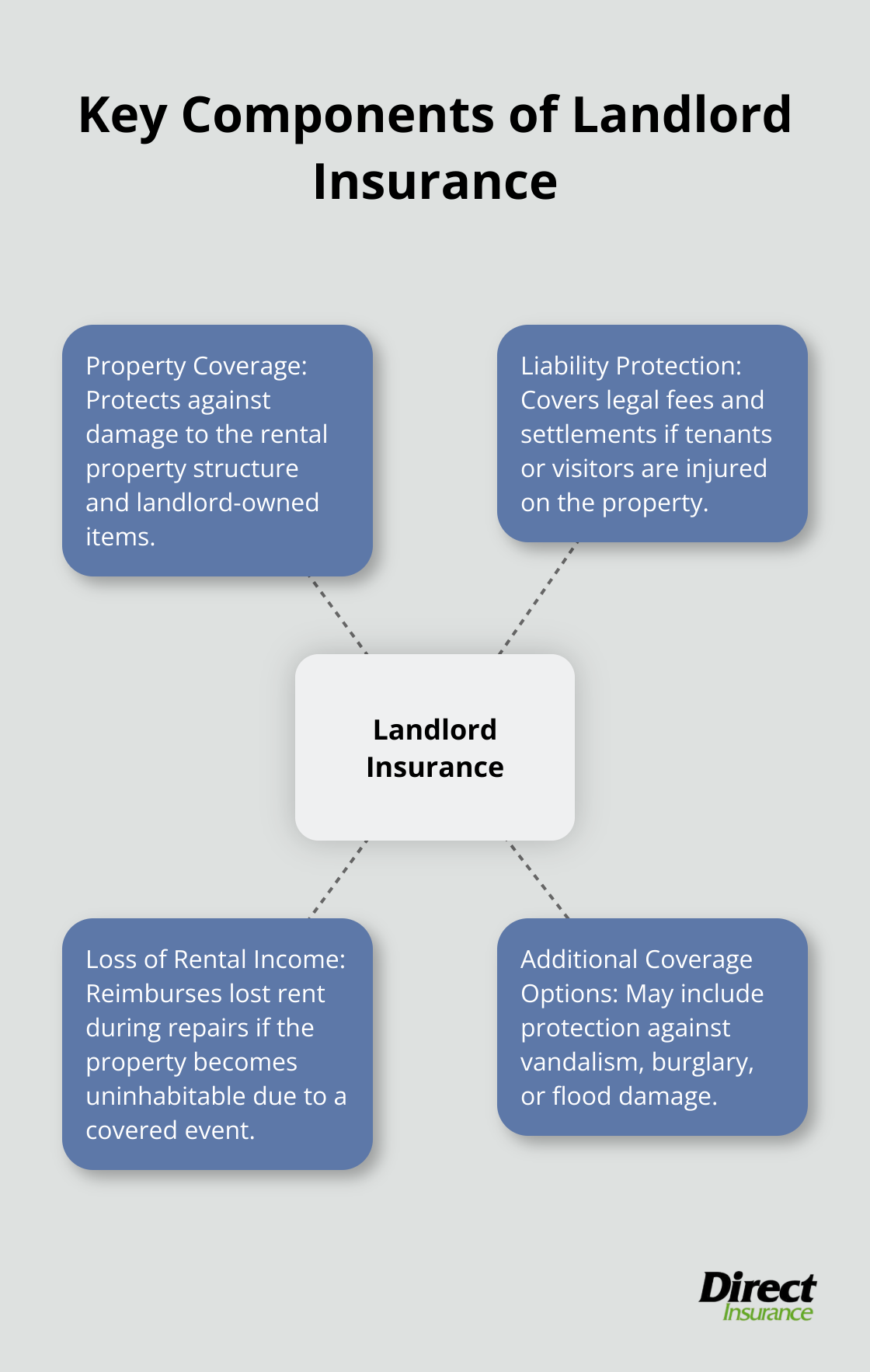

Landlord insurance offers more extensive property coverage than standard home insurance. This type of policy addresses the unique risks rental properties face. Landlord policies typically cover the building structure, other structures on the property (like garages or sheds), and often include coverage for landlord-owned appliances and furniture.

Robust Liability Safeguards

Liability protection forms a critical component of landlord insurance. A strong landlord policy provides coverage for legal fees and settlements if a tenant or visitor sustains an injury on your property. This protection extends to various scenarios, such as a tenant’s dog biting a neighbor or a delivery person slipping on an icy walkway.

Rental Income Protection

One of the most valuable features of landlord insurance is loss of rental income coverage. This coverage reimburses you for lost rent during repairs if your property becomes uninhabitable due to a covered event (like a fire or severe storm). Without this coverage, landlords could face significant financial strain during extended repair periods.

Customizable Coverage Options

Many landlord policies offer additional coverage options to address specific risks. You might consider adding flood insurance if your property sits in a flood-prone area. Other options might include coverage for vandalism, burglary, or even rent guarantee insurance to protect against tenant default.

The Importance of Proper Coverage

Selecting the right landlord insurance plays a vital role in protecting your investment and financial well-being. The right coverage can mean the difference between a minor setback and a major financial loss. As we move forward, let’s explore the essential components of home insurance to understand how it differs from landlord coverage.

What Does Home Insurance Cover?

Home insurance serves as a vital shield for homeowners, protecting their most valuable asset. At Direct Insurance Services, we’ve witnessed how the right home insurance policy provides peace of mind and financial security. Let’s explore the key components of a typical home insurance policy.

Dwelling Coverage: The Core of Home Protection

Dwelling coverage forms the foundation of any home insurance policy. It protects the physical structure of your home, including walls, roof, floors, and built-in appliances. According to recent data, 6% of insured homes filed at least one claim in 2020, with the average property damage claim amount from 2016 to 2020 being $13,962. This underscores the importance of adequate coverage to rebuild or repair your home in case of disaster.

When you determine your dwelling coverage amount, consider the cost to rebuild your home, not its market value. Construction costs can vary widely by region. In Utah, for example, the average cost to build a home is $150 per square foot (according to HomeAdvisor’s 2023 data).

Personal Property Protection: Guarding Your Belongings

Home insurance doesn’t just cover the structure; it also protects your personal belongings. This includes furniture, clothing, electronics, and other items. Most policies cover personal property at about 50-70% of your dwelling coverage amount. However, high-value items like jewelry or art may need additional coverage.

A home inventory is essential for maximizing this coverage. The National Association of Insurance Commissioners reports that only 50% of homeowners have a home inventory. Creating one can help ensure you have enough coverage and simplify the claims process if you ever need to use your insurance.

Liability Coverage: Defending Your Assets

Liability coverage is often overlooked but is a vital part of home insurance. It protects you if someone is injured on your property or if you accidentally damage someone else’s property. The Insurance Information Institute reports that the average liability claim for bodily injury or property damage to others is about $23,000.

We recommend you consider an umbrella policy for additional liability protection, especially if you have significant assets or engage in high-risk activities (like owning a pool or trampoline).

Additional Living Expenses: Maintaining Your Lifestyle

If your home becomes uninhabitable due to a covered loss, Additional Living Expenses (ALE) coverage helps pay for temporary housing and other necessary costs. This can include hotel bills, restaurant meals, and other expenses above your normal living costs.

The amount of ALE coverage varies, but it’s typically about 20% of your dwelling coverage. However, some insurers offer higher limits.

Home insurance is a complex product with many variables. While this overview covers the basics, every homeowner’s situation is unique.

Final Thoughts

Landlord insurance vs home insurance presents distinct coverage options for property owners. Landlord insurance protects rental properties with broader coverage, higher liability limits, and rental income protection. Home insurance focuses on owner-occupied residences, offering extensive personal property coverage and additional living expenses protection.

Property owners must select the right policy to safeguard their financial future. The wrong coverage can expose you to significant risks and potential losses. Regular reviews of your insurance needs are essential as your property situation changes.

At Direct Insurance Services, we help property owners navigate insurance complexities. Our experienced professionals guide you through our comprehensive insurance offerings to ensure you have the right coverage. Contact us today to review your current coverage or explore new policy options (we work with top-rated carriers to provide tailored solutions).