Condo Unit Coverage Details: What Your Policy Actually Covers

Condo ownership comes with a unique insurance puzzle. Your personal policy and your building’s master policy cover different things, and most condo owners don’t realize where the gaps are.

At Direct Insurance Services, we’ve seen firsthand how confusion about condo unit coverage details leads to expensive surprises when claims happen. This guide breaks down exactly what you’re protected for and what you need to add.

What Your HO-6 Policy Actually Covers

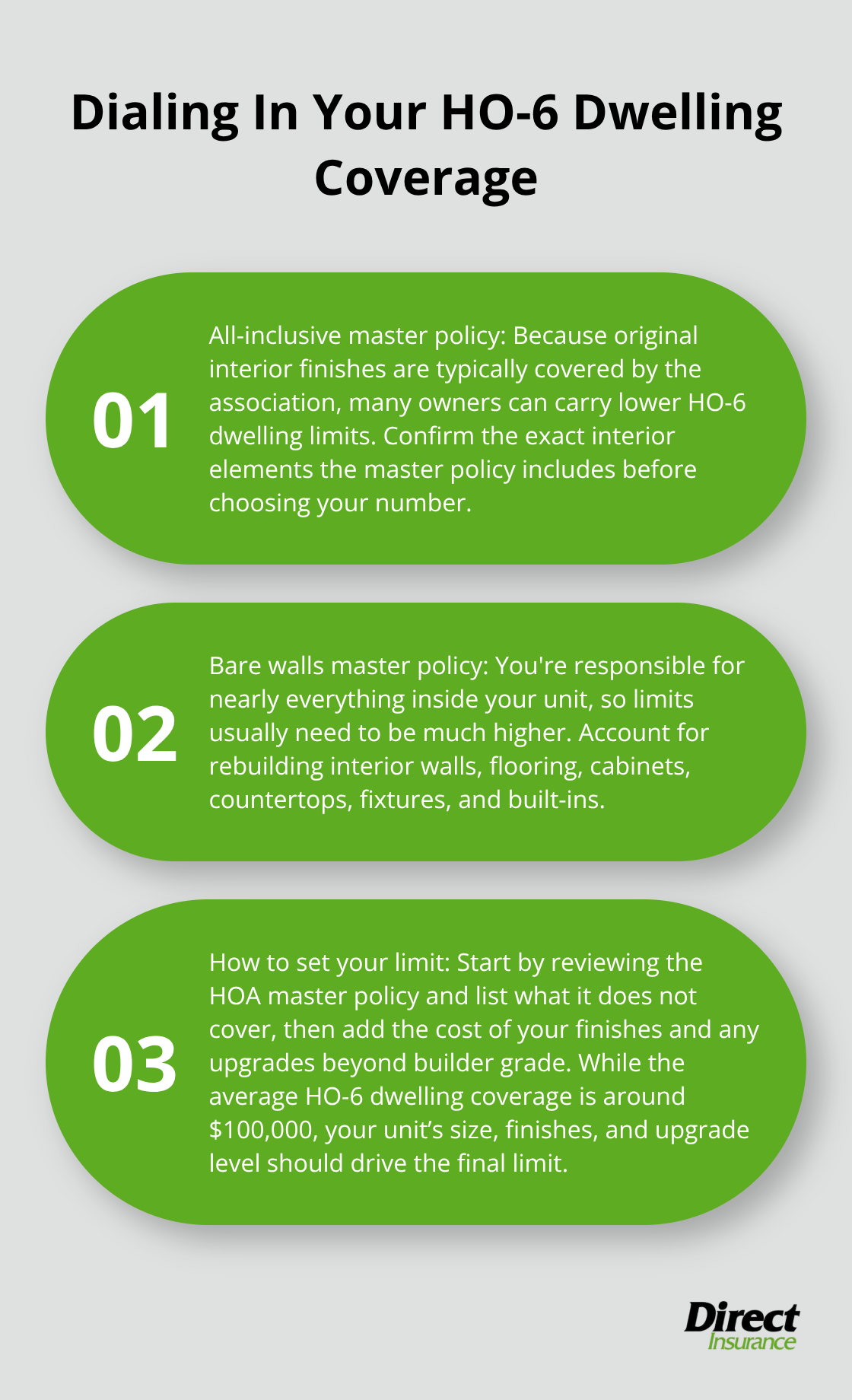

Your HO-6 condo policy covers the interior of your unit starting from the drywall inward, which means you own and maintain structural elements inside your space. This includes interior walls, flooring, cabinets, countertops, built-in appliances, and fixtures that are permanently attached to your unit. The exact scope depends on your HOA’s master policy type. If your association has an all-inclusive master policy, you may need less dwelling coverage since they handle more interior elements. If they have a bare walls policy, you’ll need substantially higher dwelling coverage because you’re responsible for nearly everything inside. A practical starting point is to review your HOA master policy and work backward from what they don’t cover.

Many condo owners underestimate this coverage and end up short when damage occurs. The average HO-6 dwelling coverage sits around $100,000, but your unit’s size, condition, and your HOA’s policy type should drive your actual limit. If you’ve upgraded your kitchen or flooring beyond builder-grade finishes, those improvements are your responsibility to insure since the master policy typically covers only original fixtures.

Your Personal Belongings Are Fully Protected

Your HO-6 policy covers personal belongings like furniture, electronics, clothing, and other items not attached to the building. Standard personal property coverage averages around $100,000 nationally, but you should conduct a home inventory to determine what you actually need. Add up the replacement cost of major items: a decent sofa runs $1,500 to $3,000, a TV might be $800 to $2,000, and a bedroom set could be $2,000 to $5,000. If your total belongings exceed your policy limit, you’re underinsured. You can choose replacement cost coverage, which pays to buy new items, or actual cash value, which pays depreciated amounts. Replacement cost costs more but protects you fully when claims happen. Covered perils typically include fire, theft, vandalism, lightning, wind damage, and some water damage, though water from outside your unit or from sewer backups is often excluded. For high-value items like jewelry, art, or collectibles, standard limits usually cap out at $1,500 to $2,500 per item. You’ll need a scheduled personal property endorsement to cover these items at full replacement value, and this requires an appraisal. The cost for this endorsement is modest, often $50 to $200 annually depending on item values.

Liability Coverage Protects You When Someone Gets Hurt

Your HO-6 policy includes personal liability coverage that pays if you’re legally responsible for someone else’s injuries or property damage. Standard limits typically start at $100,000 to $300,000, though the average HO-6 includes around $300,000 in liability protection. This covers medical bills, legal defense costs, and settlements if a guest slips on your floor, your guest’s phone gets damaged in your unit, or someone claims you caused them harm. Liability also covers damage you cause to others’ property, like accidentally breaking a neighbor’s window from your balcony. However, liability claims can exceed these limits quickly. A serious injury lawsuit can easily reach $500,000 or more, which is why umbrella insurance makes sense for condo owners. Umbrella policies add an extra $1 million in liability coverage for around $150 to $300 per year. Without it, you’re personally liable for anything above your HO-6 limit. Most mortgage lenders require a minimum of $100,000 in liability, but this is the bare minimum. Try at least $300,000, and umbrella coverage if your net worth exceeds $250,000. Your liability coverage doesn’t apply to intentional acts or business activities, so if you run a home-based business, you’ll need separate business liability coverage.

What Happens When Coverage Limits Fall Short

Your HO-6 policy has specific dollar limits on what it pays, and these limits matter more than most condo owners realize. Personal property coverage caps at your chosen limit, meaning a $100,000 limit won’t cover $150,000 in belongings. Liability limits work the same way-once you hit your policy maximum, your personal assets are at risk. This is where the gaps between your HO-6 and your HOA’s master policy create real exposure. If your master policy covers only the building shell and you haven’t insured your interior upgrades, a major fire leaves you responsible for rebuilding costs that exceed your dwelling limit. The next section explains what your association’s master policy actually covers and where your responsibilities begin.

What Your HOA Master Policy Actually Covers

The Building Structure and Common Areas Your Association Insures

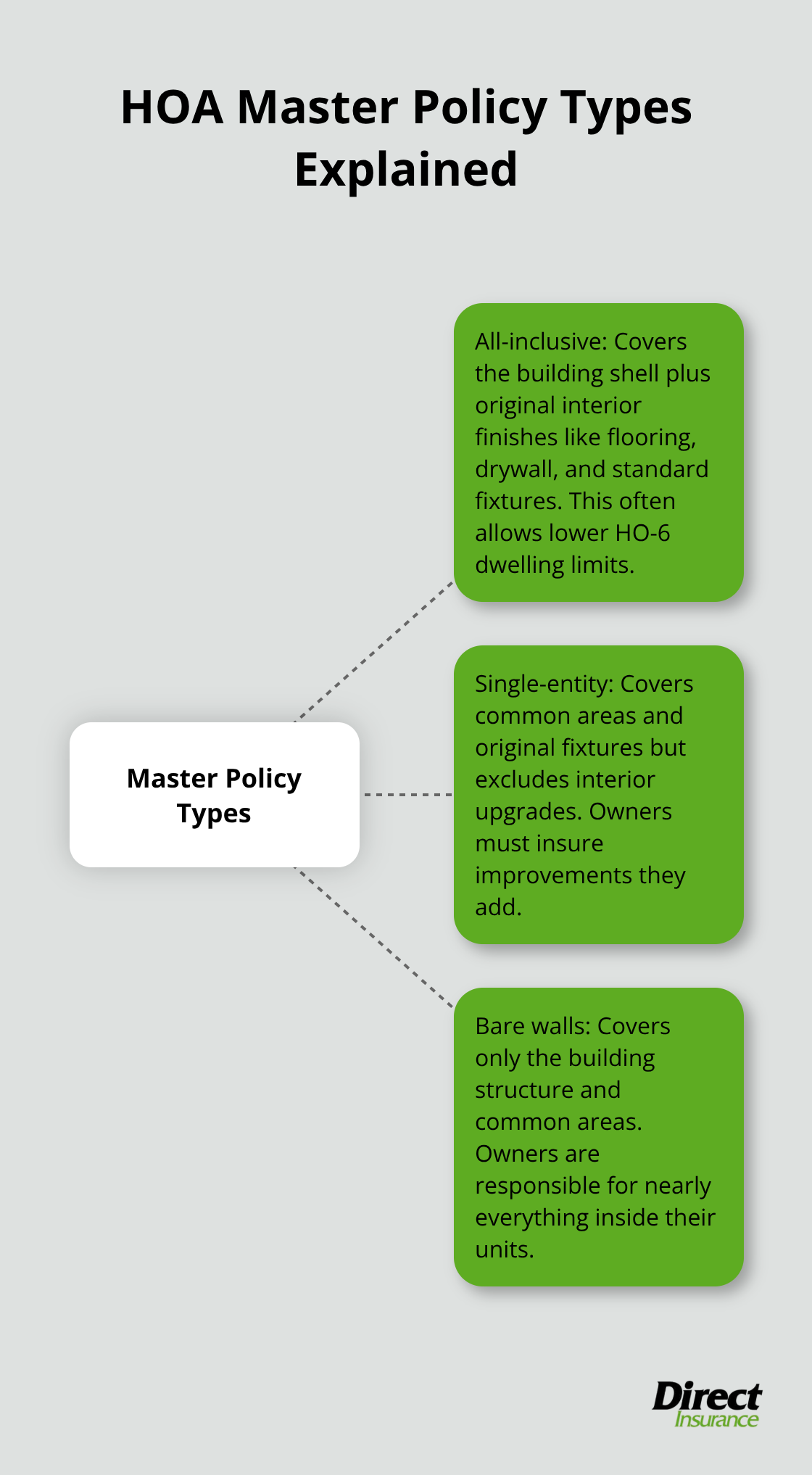

Your HOA master policy covers what the association owns-not what you own. The master policy protects the building structure from the outside in, including exterior walls, the roof, common hallways, lobbies, parking areas, and shared amenities like pools or fitness centers. The exact coverage depends on which of three master policy types your association selected: all-inclusive, single-entity, or bare walls.

An all-inclusive policy covers the building shell plus original interior finishes like flooring, drywall, and standard fixtures, which means your HO-6 dwelling coverage can stay lower. A single-entity policy covers common areas and original fixtures but not interior upgrades, so you’re responsible for any improvements you make. A bare walls policy covers only the building structure and common areas, leaving you responsible for nearly everything inside your unit.

This distinction matters enormously.

How Master Policy Types Affect Your Coverage Needs

A condo owner in a bare walls building needs $150,000 to $200,000 in dwelling coverage, while someone in an all-inclusive building might only need $50,000 to $75,000. You must obtain a copy of your HOA master policy and review it with your insurance agent before deciding on coverage limits. Most condo associations require owners to carry HO-6 insurance, and your lender will too, but the master policy is where gaps emerge.

Deductibles and Assessment Risk

HOA master policy deductibles often have high deductibles, and those deductibles come out of the association’s pocket first. When a major loss occurs-like a roof collapse or fire affecting multiple units-the association pays its deductible before insurance kicks in. That deductible often ranges from $5,000 to $25,000 or higher for large buildings.

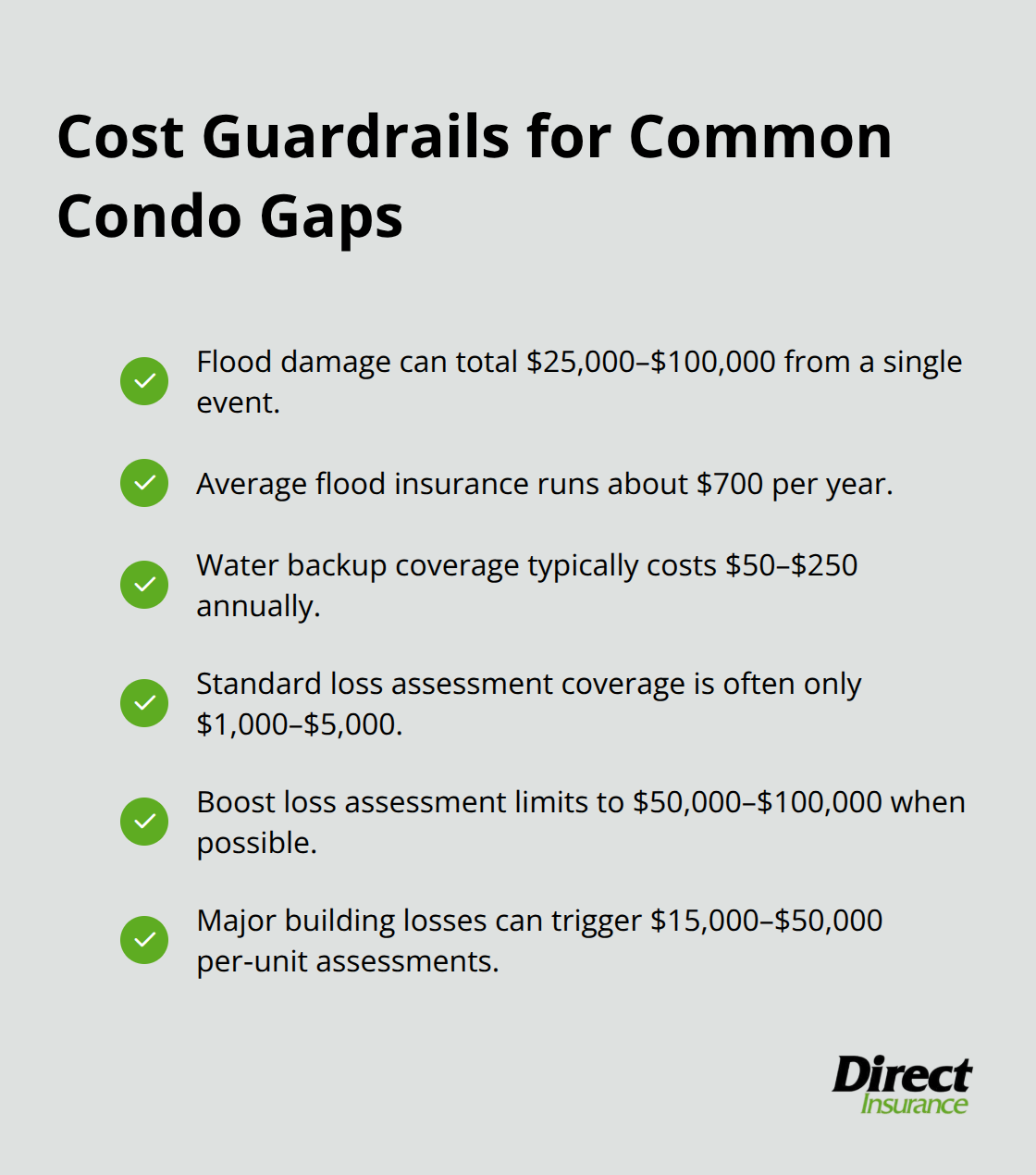

If the damage costs $500,000 but exceeds the master policy limit or if the association’s insurer denies part of the claim, the HOA can assess unit owners for the shortfall. This is where loss assessment coverage on your HO-6 becomes critical. Standard loss assessment coverage might only protect you for $1,000 to $5,000 in assessments, which is dangerously low. You should boost loss assessment coverage to $50,000 or $100,000, which costs only $20 to $50 more per year. A single major loss could trigger an assessment of $10,000 to $50,000 per unit, and without adequate loss assessment coverage, you pay that out of pocket.

Evaluating Your Building’s Risk Profile

Review your HOA’s master policy limits, deductible amounts, and recent financial statements showing reserve funds. Buildings with strong reserve funds and higher master policy limits create fewer assessment situations. Buildings with low reserves and bare walls policies create serious risk for owners. Your HO-6 and the master policy work together, but they’re not the same thing-and the gaps between them determine whether you face unexpected costs when disaster strikes.

Common Coverage Gaps Most Condo Owners Miss

Flood and Water Damage Leave You Exposed

Standard HO-6 policies exclude flood damage entirely, and this matters far more than most condo owners realize. The National Flood Insurance Program provides flood insurance to property owners, renters and businesses, and having this coverage helps them recover faster when floodwaters recede. If you live anywhere near a flood zone, a heavy rain event can cost $25,000 to $100,000 in water damage to your unit and belongings. FEMA estimates the average flood insurance policy costs about $700 per year, which sounds expensive until you face a $50,000 claim out of pocket. Check your property’s flood zone through FEMA’s flood map tool, and if you’re in a high-risk area, don’t skip flood coverage.

Water backup coverage is equally important and often overlooked. This covers damage from sewer backups, drain overflows, or failed sump pumps-situations that happen more often than you’d think during heavy rain. Standard HO-6 policies exclude this, but adding water backup coverage costs only $50 to $250 annually and can save you thousands.

Personal Possessions in Common Areas Aren’t Protected

Personal possessions stored in common areas-like a bike in the hallway, holiday decorations in shared storage, or furniture in a common area locker-typically aren’t covered by your HO-6 or the master policy. Your personal property coverage applies to items inside your unit, not shared spaces. If someone steals your bike from the hallway or a flood damages items in the building’s storage room, you’re responsible for the loss. The solution is straightforward: keep valuable items inside your unit whenever possible, and if you must use common storage, photograph everything and document the value.

Liability Limits Create Major Exposure

For liability protection, standard HO-6 limits of $300,000 often aren’t enough. A serious injury claim can easily exceed $500,000, and once you hit your policy limit, your personal assets are exposed. Umbrella insurance adds $1 million in liability coverage for $150 to $300 per year-a small cost relative to the protection it provides. If your net worth exceeds $250,000 or you frequently host guests, umbrella coverage isn’t optional.

Loss Assessment Coverage Protects Against Surprise Bills

Loss assessment coverage deserves serious attention. Many condo owners carry only $1,000 to $5,000 in loss assessment protection, which is dangerously low. A single major loss affecting the building can trigger assessments of $15,000 to $50,000 per unit, and without adequate coverage, you pay the difference yourself. Increasing loss assessment coverage to $50,000 or $100,000 costs only $20 to $50 more annually. This single endorsement protects you from the most expensive surprise condo owners face.

Final Thoughts

Condo unit coverage details determine whether you face financial disaster or stay protected when loss strikes. Your HO-6 policy covers your unit’s interior and belongings, while your HOA’s master policy covers the building structure and common areas-but neither covers everything. We at Direct Insurance Services have worked with condo owners who discovered too late that gaps between these policies left them exposed, and most of those situations were preventable with proper planning.

Your dwelling coverage, personal property limits, liability protection, and loss assessment endorsement all work together to fill those gaps. Flood insurance, water backup coverage, umbrella liability, and higher loss assessment limits ($50,000 to $100,000) cost modest amounts annually but protect you from tens of thousands in unexpected expenses. These additions aren’t luxuries-they’re practical safeguards against the most expensive situations condo owners face.

Contact your HOA for a copy of the master policy and review it with an insurance professional who understands condo coverage. Check your flood zone through FEMA’s mapping tool, document your belongings and their replacement cost, and then contact Direct Insurance Services to review your HO-6 limits and add missing endorsements. This process takes a few hours but prevents thousands in unexpected costs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation