Vacant Rental Property Insurance: Protecting An Idle Asset

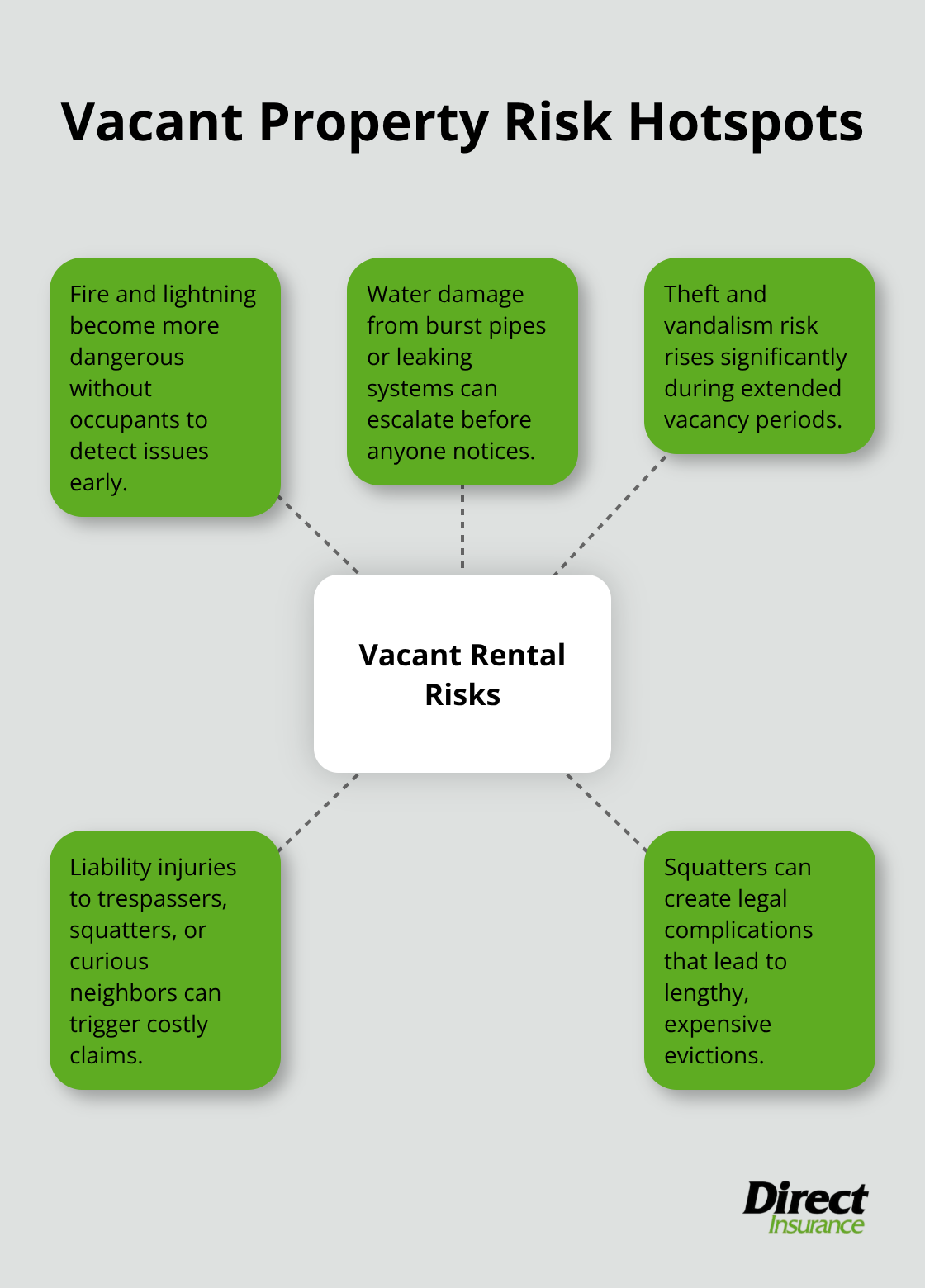

Vacant rental properties sit idle, but the financial risks don’t. Without proper vacant rental property insurance, you’re exposed to theft, vandalism, and liability claims that standard homeowners policies won’t cover.

At Direct Insurance Services, we’ve seen property owners lose thousands because they didn’t understand their coverage gaps. The good news is that protecting your investment doesn’t have to be complicated.

What Vacant Property Insurance Actually Covers

Vacant property insurance protects the structure of an unoccupied rental home against specific perils like fire, lightning, wind, hail, and water damage from burst pipes or leaking systems. The coverage focuses on the building itself, not the land or personal property inside. This distinction matters because standard homeowners policies typically include a vacancy clause that voids or reduces coverage after 30 to 90 days of vacancy. Once your property sits empty beyond that threshold, you lack protection against the very risks that spike when no one is living there.

Theft and vandalism become real threats, yet most standard policies exclude these losses during extended vacancy periods.

Why Your Standard Policy Fails When the Property Is Empty

Standard homeowners policies assume someone lives in the home, which reduces risk in measurable ways. An occupied property receives regular inspections, immediate leak detection, and active security. An empty property deteriorates differently. Fire risk escalates dramatically-structural fire risk in vacant buildings is a serious concern that standard policies don’t adequately address.

Standard policies don’t account for this elevated danger. Vacant property insurance is specifically priced and designed for unoccupied conditions, offering named-peril coverage that addresses the real hazards of an idle asset. The coverage typically includes optional add-ons for theft and vandalism, but only if you meet specific criteria like maintaining an active security system or keeping the property in excellent condition.

The Real Financial Cost of Going Uninsured

A vacant rental property bleeds money in ways many owners underestimate. Monthly carrying costs typically range from $1,500 to $3,000 depending on location and property size, covering property taxes, maintenance, utilities, and mortgage payments. A single month of unexpected damage-say, a burst pipe or roof leak-can easily exceed $5,000 to $15,000 in repairs. Without proper coverage, you absorb these costs entirely.

The financial pressure intensifies if squatters occupy the property, which creates legal complications that can lead to lengthy and costly eviction processes varying by jurisdiction. Some areas allow squatters to establish legal rights after specific periods, potentially costing tens of thousands in legal fees and lost rent. Vacant property insurance fills these gaps directly. Coverage limits up to $5 million in property protection and up to $1 million in general liability are available through carriers, subject to underwriting approval.

Understanding Coverage Limits and What They Mean for Your Investment

The cost of specialized vacant property coverage is higher than standard homeowners insurance due to elevated risk, but it remains far lower than the financial devastation of an uninsured loss or extended legal battle with unauthorized occupants. When you compare the monthly premium against potential repair costs (which often reach five figures for water damage or fire), the protection becomes economically obvious. Different carriers offer varying limits and conditions, so the specific coverage you obtain depends on your property’s characteristics, location, and underwriting approval.

Your next step involves understanding which types of coverage actually apply to your rental property and how they work together to create a complete protection strategy.

Types of Coverage That Protect Your Vacant Rental

Vacant rental property insurance comes in distinct coverage types, each addressing specific risks that emerge when a property sits empty. Understanding what each type covers prevents costly gaps in protection and ensures your investment stays genuinely secure. The three primary coverage components work together to create comprehensive protection, though not every policy includes all three automatically.

Dwelling Fire Insurance: Your Foundation

Dwelling fire insurance forms the foundation of vacant property protection, covering structural damage from fire, lightning, wind, hail, and water intrusion from burst pipes or malfunctioning sprinkler systems. This coverage focuses exclusively on the building structure itself, excluding land and contents. The critical distinction from standard homeowners policies is that dwelling fire coverage for vacant properties uses named-peril language, meaning it explicitly lists which risks are covered rather than covering all risks except exclusions. This approach makes sense for unoccupied buildings because insurers can price the coverage accurately for the specific hazards that spike during vacancy.

When you select this coverage, verify that your policy includes water damage protection, since frozen pipes represent one of the costliest claims on vacant properties during winter months. Some carriers require that you maintain the property at a minimum temperature of 40°F to qualify for water damage coverage, so confirming these conditions upfront prevents claim denials later.

Liability Protection: Addressing Trespasser and Injury Risks

Liability coverage for vacant buildings covers legal expenses and damages if someone is injured on your property and you’re found legally responsible. This coverage matters more than many landlords realize because vacant properties attract trespassers, squatters, and curious neighbors who may suffer injuries while on the premises. General liability limits up to $1 million are available through specialized carriers, though availability varies by insurer and property characteristics.

Properties with hazards like swimming pools, trampolines, or nearby bodies of water typically face stricter underwriting or higher premiums because these features increase injury risk substantially. Understanding your property’s specific hazards helps you anticipate coverage restrictions before you apply.

Loss of Rents Coverage: Protecting Your Cash Flow

Loss of rents coverage compensates you for income lost during periods when the property cannot be rented due to covered damage. If a fire damages the rental unit and repairs take three months to complete, loss of rents coverage reimburses the rent you would have collected during that period, protecting your rental income protection when you need it most. This coverage typically applies only to damage from named perils covered under the dwelling fire portion of the policy, so confirming the connection between these two components is essential when reviewing your quote.

Each coverage type addresses a different dimension of vacant property risk. The next section walks you through how to actually obtain these protections in Utah and what to expect when you work with an insurance agent.

How to Secure Vacant Property Insurance in Utah

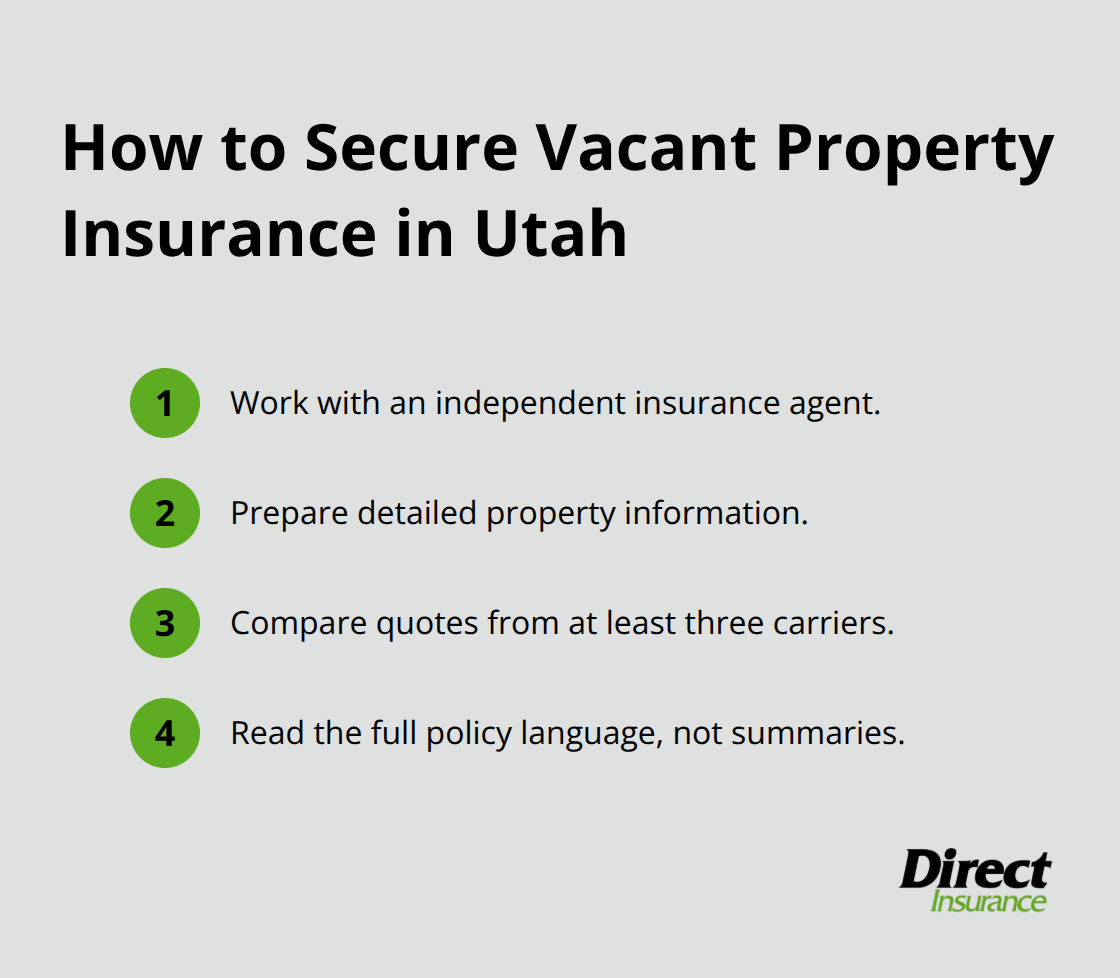

Work with an Independent Insurance Agent

Securing vacant property insurance in Utah requires working with an agent who understands both the coverage mechanics and the specific risks your property faces. Independent insurance agents hold a significant advantage over direct online quotes because they can access multiple carriers simultaneously and identify which ones actually specialize in vacant rental properties. Many national carriers either decline vacant property applications outright or impose such restrictive conditions that coverage becomes impractical.

Working with an independent insurance agent gives you access to carriers that specialize in unoccupied rental homes, cutting through the complexity that makes this process frustrating for most property owners.

Prepare Your Property Information

When you contact an agent, come prepared with specific property details: the property’s age, its condition, whether security systems are installed, proximity to fire stations, any prior claims history, and how long you expect the vacancy to last. Carriers underwrite vacant properties differently than occupied homes, and this information directly affects your eligibility and premium rates. Some carriers require properties to be under 40 years old with no prior losses to qualify for their special form coverage, while others accept older structures if they’ve undergone full renovation within the past 30 years. Understanding these thresholds upfront prevents wasted time pursuing quotes from carriers with strict eligibility requirements your property cannot meet.

Compare Rates Across Multiple Carriers

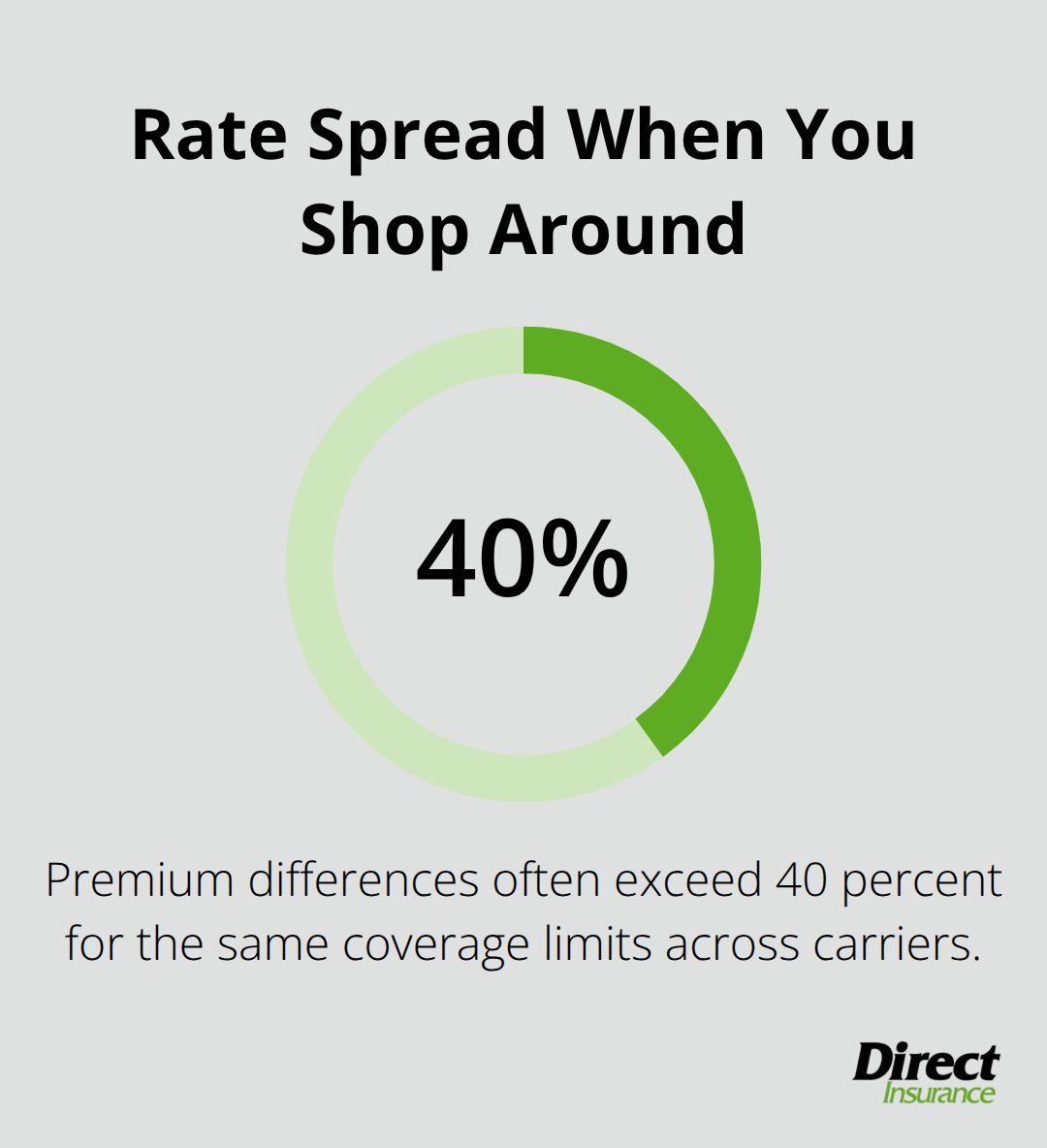

Comparing rates across multiple carriers is essential because vacant property premiums vary dramatically based on underwriting approach and risk tolerance. Request quotes using identical property specifications from at least three different carriers so you’re comparing apples to apples-premium differences often exceed 40 percent for the same coverage limits.

When reviewing quotes, examine the specific perils covered, whether theft and vandalism are included, what general liability limits are offered, and whether loss of rents coverage is available. Pay close attention to any special conditions, such as minimum temperature requirements during winter or mandatory alarm system installation for theft coverage.

Review Policy Language, Not Just Summaries

A quote that appears cheaper upfront often carries exclusions that leave you underprotected, so read the actual policy language rather than relying on the quote summary. The policy itself is the contract and fully describes coverage, while brochure descriptions remain general. An independent insurance agent can walk you through what each quote actually covers and identify which option provides the strongest protection for your specific property and situation, helping you understand exactly what you’re purchasing before you commit to a policy.

Final Thoughts

Vacant rental property insurance protects your investment when standard policies leave you exposed. The financial stakes are real: monthly carrying costs between $1,500 and $3,000, potential repair bills exceeding $15,000, and legal battles with squatters that drain resources for months. Dwelling fire coverage, liability protection, and loss of rents compensation work together to address the specific risks that emerge when a property sits empty.

Contact an independent insurance agent who specializes in vacant rental properties and request quotes from multiple carriers using identical property specifications. Comparing rates across at least three providers reveals significant premium differences, often exceeding 40 percent for the same coverage. Review the actual policy language rather than summaries, since brochure descriptions remain general while the policy itself defines exactly what you’re purchasing.

Professional guidance matters because vacant rental property insurance involves underwriting rules that vary dramatically between carriers (some require properties under 40 years old with no prior losses, while others accept older structures if fully renovated within 30 years). An experienced agent navigates these requirements and identifies which carriers actually specialize in unoccupied rental homes. Contact Direct Insurance Services today to discuss your vacant property situation and get a quote that protects your investment properly.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation