Condo Insurance Deductibles Utah: How to Choose Yours

Your condo deductible is one of the most important decisions you’ll make when buying insurance. It directly affects both your monthly premium and what you’ll pay out of pocket if something goes wrong.

At Direct Insurance Services, we’ve helped hundreds of Utah condo owners find the right balance between affordability and protection. The right deductible depends on your finances, your building’s condition, and how much risk you’re willing to take on.

What a Deductible Actually Costs You

A deductible is the amount you pay out of your own pocket before your insurance covers the rest of a claim. If your condo suffers water damage that costs $5,000 to repair and you have a $1,000 deductible, you pay $1,000 and your insurer covers $4,000. This straightforward concept has enormous practical implications for your finances.

The Utah Department of Insurance emphasizes that understanding how your deductible interacts with your condo association’s master policy matters because gaps between these two policies can leave you exposed. Your personal condo policy (HO-6) typically covers your personal belongings, interior walls, and liability, while the association’s master policy covers the building exterior and common areas. If the association’s policy has a $5,000 deductible and a shared plumbing failure causes $8,000 in damage to common areas, the association might assess residents for that $5,000 gap. This is why loss-assessment coverage exists-it protects you from unexpected bills when the association’s deductible exceeds claim costs.

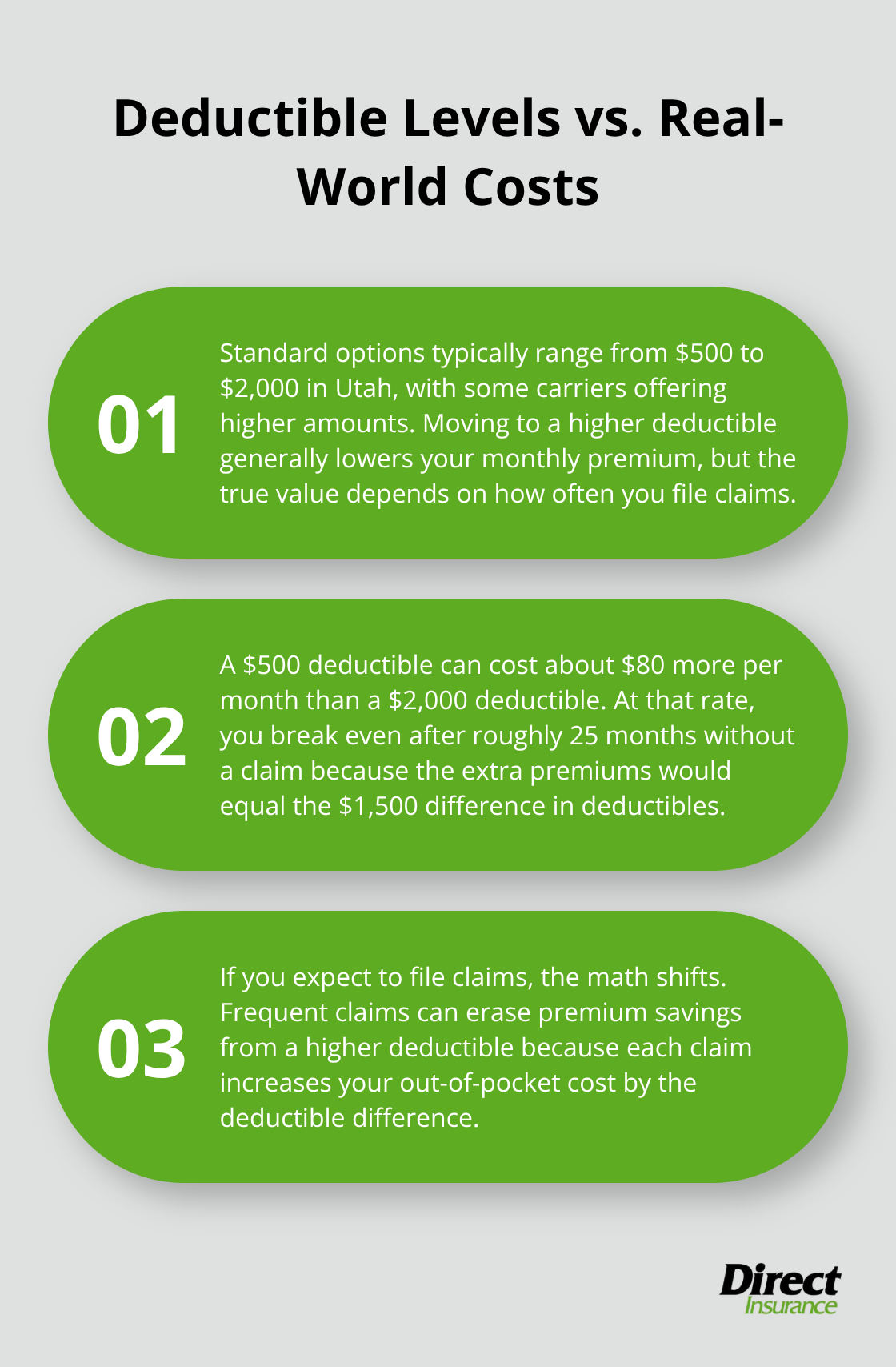

Standard Deductible Options and Premium Savings

Standard deductible options in Utah range from $500 to $2,000, though some insurers offer higher amounts. Higher deductibles reduce your monthly premium significantly; requesting side-by-side quotes at different deductible levels shows the real savings. A $500 deductible might cost $80 more per month than a $2,000 deductible, meaning you’d break even after 25 months of claims-free insurance. This math changes if you actually file claims. If you file two claims in five years, the higher deductible saves you money overall despite larger out-of-pocket costs per claim.

Your Emergency Fund Determines What You Can Actually Afford

The deductible you choose must match what you can realistically pay when a loss occurs. The Consumer Financial Protection Bureau recommends maintaining three to six months of essential expenses as an emergency fund, which gives you a foundation to cover deductibles without financial stress. If your emergency fund holds $8,000, choosing a $2,000 deductible is manageable; choosing a $5,000 deductible leaves you vulnerable.

Utah’s weather patterns-winter storms, hail, and wildfire risk in certain areas-mean condo claims aren’t hypothetical. Hail damage claims spike in spring and early summer across Utah’s Front Row communities. If you live in a hail-prone area and lack adequate emergency savings, a lower deductible protects you from being forced into debt after a claim. Conversely, if you have $25,000 in liquid savings and stable income, a $2,500 or higher deductible makes financial sense because the premium savings compound over years without claims.

How HOA Communication Failures Affect Your Deductible Strategy

One Utah condo community faced a sewage backup that caused $27,000 in mitigation costs and $67,000 in rebuilding expenses. The association’s deductible had risen from $25,000 to $50,000 without notifying residents. Owners discovered the higher deductible only when the claim was filed, suddenly owing far more than expected.

The Utah Code Title 57 establishes requirements for how associations handle insurance, but notification practices vary. Some associations notify owners of deductible increases; others do not. Request a copy of your association’s master insurance policy and any recent correspondence about coverage changes. Ask specifically about the deductible amount and whether any recent increases occurred. Understanding whether your association’s deductible is $10,000, $25,000, or $50,000 fundamentally changes your personal policy strategy. If the association carries high deductibles, you might choose loss-assessment coverage rather than a higher personal deductible, shifting risk management to where it matters most for your building’s specific situation.

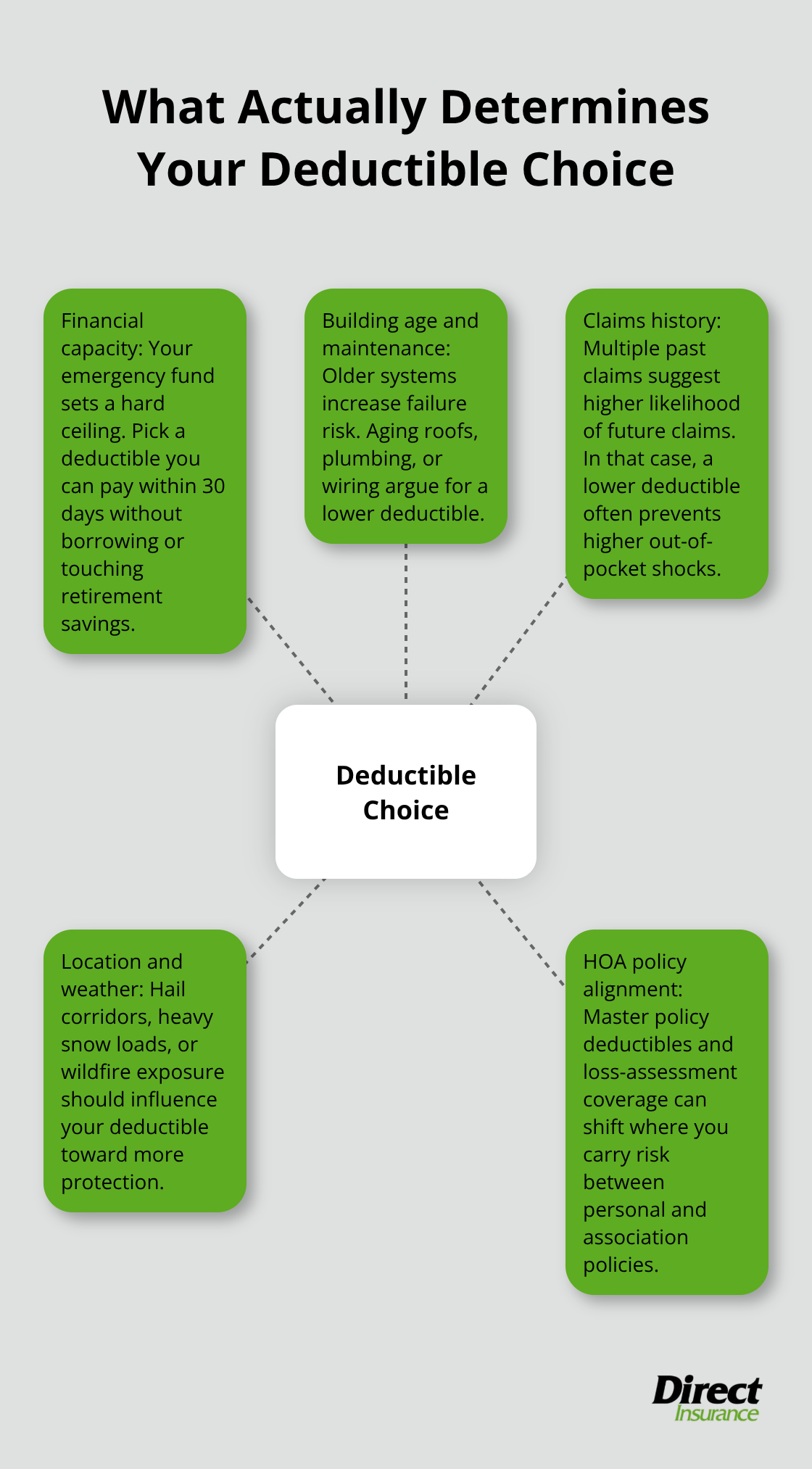

What Actually Determines Your Deductible Choice

Financial Capacity Sets Your Real Limit

Your ability to pay a deductible out of pocket determines what you can actually afford, and this isn’t theoretical. An emergency fund is a cash reserve that’s specifically set aside for unplanned expenses or financial emergencies. If you have $6,000 in emergency savings, a $2,000 deductible works; a $5,000 deductible leaves you one moderate claim away from financial stress. We see this mismatch constantly-owners select deductibles based on premium savings alone, then panic when a claim arrives. Calculate what you can actually pay within 30 days without borrowing or depleting retirement funds, then set your deductible at or below that amount. Anything higher risks your financial stability.

Building Age and Maintenance History Shape Your Risk

A condo built in 1985 carries different risk than one built in 2015, and your deductible should reflect that reality. Older buildings have aging plumbing, electrical systems, and roofing that fail more frequently. Utah’s dry climate means older metal roofs corrode, and freeze-thaw cycles damage pipes in units with poor insulation. If your building’s roof exceeds 20 years or the plumbing hasn’t been upgraded since the 1990s, expect more claims-a lower deductible protects you better financially over time. A newer condo with recent system replacements and modern construction justifies a higher deductible because major failures occur less often. Ask your HOA about the last major capital improvements and condition reports from inspections. Recent roof replacement, plumbing upgrades, or improved drainage systems support a $2,000 deductible. Original systems in a 30-year-old building warrant $1,000 or lower.

Your Claims History Predicts Future Behavior

Insurance companies track claims patterns because they predict future behavior. If you filed three claims in the past five years, insurers view you as higher risk, and your premiums reflect that reality. In this situation, choosing a higher deductible to save on premiums backfires because you’ll likely file another claim soon. The math works against you: if you save $50 monthly by choosing a $2,000 instead of a $1,000 deductible, but you file a claim within 18 months, you’ve saved $900 but paid an extra $1,000 out of pocket. If you haven’t filed a claim in ten years and your building has solid maintenance records, a higher deductible genuinely saves money because the probability of needing it remains low. Utah’s weather patterns matter here-hail storms concentrate in certain regions and strike repeatedly in the same areas. If you live in a hail-prone zone near the Wasatch Front and your building filed two hail claims in four years, a lower deductible protects your finances despite higher premiums. Check your personal claims history through the Comprehensive Loss Underwriting Exchange database, which most insurers access when pricing your policy.

Location and Weather Exposure Demand Attention

Where you live in Utah determines your exposure to specific perils. The Wasatch Front experiences frequent hail damage in spring and early summer, while southern Utah faces wildfire risk. Northern Utah communities deal with heavy snow loads and freeze-thaw damage. Your deductible strategy should account for these regional patterns. If your building sits in a hail corridor and has filed multiple claims for hail damage, a $1,000 deductible makes more financial sense than a $2,000 deductible, even if premiums cost more. Conversely, if your condo sits in a low-risk area with minimal weather exposure and no recent claims, premium savings from a higher deductible accumulate faster. Request your building’s claims history from the HOA-this data reveals what actually happens in your specific location and building, not what happens statewide. Your deductible choice should match your building’s actual loss experience, not theoretical risk.

Coordinating With Your HOA’s Coverage Strategy

Your personal deductible decision connects directly to your association’s master policy deductible. If your HOA carries a $50,000 deductible on the master policy and a shared plumbing failure causes $60,000 in damage to common areas, the association assesses residents for that $50,000 gap. Loss-assessment coverage protects you from these unexpected bills when the association’s deductible exceeds claim costs. If your HOA carries high deductibles, you might prioritize loss-assessment coverage rather than selecting a higher personal deductible. This shifts your risk management strategy to where it matters most for your building’s specific situation. Request a copy of your association’s master insurance policy and ask about recent deductible changes. Understanding whether your association’s deductible is $10,000, $25,000, or $50,000 fundamentally changes your personal policy strategy and helps you coordinate coverage across both policies.

What Deductibles Actually Cost in Utah

In Utah, condo deductibles typically range from $500 to $2,000, with some insurers offering higher amounts depending on your building’s age and claims history. The difference between these options translates directly to your wallet. A $500 deductible costs you $80 to $100 more per month than a $2,000 deductible, which means you’d break even after 25 months of claims-free insurance. However, this math flips if you file claims regularly. If your building experiences two claims within five years-a realistic scenario in Utah given our weather patterns-the higher deductible actually costs you more money overall despite the lower monthly premium. The Utah Department of Insurance emphasizes that this calculation must account for your specific building’s loss history, not statewide averages. Request your HOA’s claims history for the past five years and compare that against your personal finances to find the actual break-even point for your situation.

Hail and Winter Storms Drive Deductible Strategy in Utah

Utah’s Wasatch Front experiences frequent hail damage in April through July, with some years seeing multiple hail events in the same neighborhoods. Buildings in hail-prone zones near Salt Lake City, Provo, and Ogden filed significantly more claims over the past decade than buildings in southern Utah or the Uinta Basin. If your condo sits in a hail corridor and your building’s records show two or more hail claims in the past seven years, a $1,000 deductible provides better financial protection than a $2,000 deductible, even if premiums cost more monthly. The premium difference compounds into savings only if you avoid claims, but buildings with established hail damage patterns shouldn’t bank on avoiding future claims. Winter storms create similar patterns in northern Utah communities where freeze-thaw cycles damage aging plumbing and snow load failures occur. Southern Utah faces wildfire risk instead, though this typically affects homeowners more than condos since associations usually maintain defensible space around buildings. Your deductible choice should match your building’s actual loss experience in your specific location, not theoretical risk. Ask your HOA whether they filed claims in the past five years, what perils caused those claims, and whether your insurance agent flagged any specific risks during the most recent policy review.

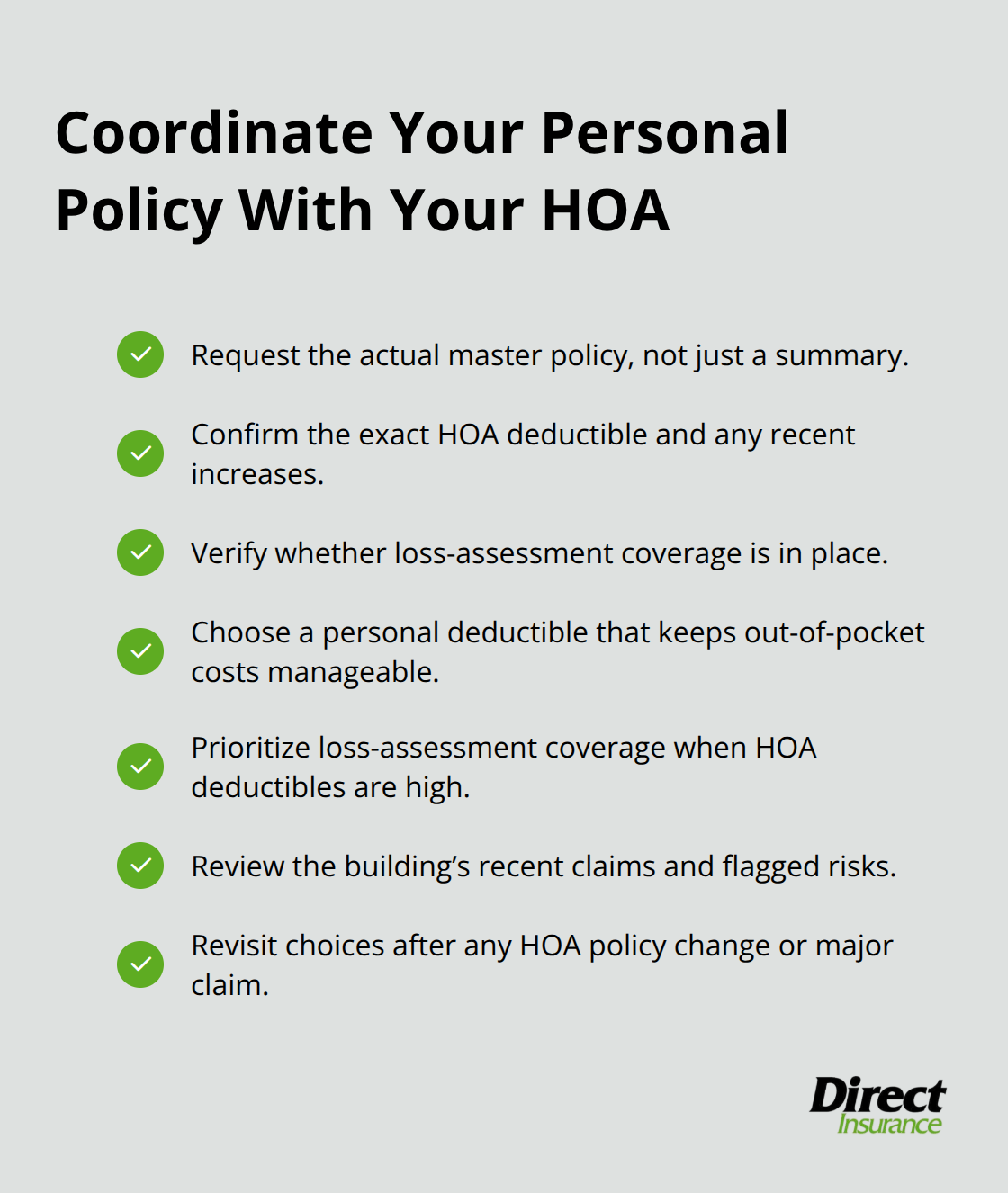

Coordinating Deductibles Across Your Personal and HOA Policies

Your personal condo deductible interacts with your association’s master policy deductible in ways that create real financial exposure. If your HOA carries a $50,000 deductible on the master policy and a shared plumbing failure causes $60,000 in damage to common areas, the association legally assesses residents for that $50,000 shortfall unless loss-assessment coverage protects you. Many Utah condo owners discover this gap only after a major claim hits their building. Rather than selecting a high personal deductible to save on premiums, you might instead prioritize loss-assessment coverage and maintain a moderate personal deductible like $1,000 or $1,500. This strategy protects you from surprise HOA assessments while keeping your out-of-pocket claim costs reasonable. Request a copy of your association’s actual master insurance policy from your HOA board, not just a summary. Confirm the exact deductible amount, any recent increases, and whether loss-assessment coverage exists. Buildings that recently increased their master deductible without notifying residents-a practice that occurs more often than it should-create financial traps for owners who didn’t adjust their personal coverage strategy accordingly.

Final Thoughts

Selecting the right condo insurance deductible in Utah requires you to balance your monthly budget against your ability to pay out of pocket when a claim strikes. Your emergency fund sets the real boundary for what deductible makes sense-if you have $8,000 in liquid savings, a $2,000 deductible works; if you have $3,000, it doesn’t. Request your HOA’s claims history for the past five years and compare that against your building’s age and condition, because older buildings with aging systems justify lower deductibles while newer buildings with recent upgrades support higher deductibles.

Utah’s weather patterns matter significantly to your deductible strategy. If your condo sits in a hail corridor on the Wasatch Front or faces wildfire risk in southern Utah, your deductible choice should account for regional loss patterns rather than statewide averages. Don’t overlook your association’s master policy deductible either, since a $50,000 HOA deductible creates financial exposure that loss-assessment coverage addresses effectively.

Contact an independent insurance agent who can compare quotes at different deductible levels and explain how your personal policy coordinates with your HOA’s coverage. We at Direct Insurance Services work with top-rated carriers to find condo insurance deductibles in Utah that match your actual financial situation and your building’s specific risks, and we’re ready to help you understand what makes sense for your circumstances.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation