Average Monthly Auto Insurance Costs: What to Expect

Auto insurance premiums hit $1,895 annually in 2024, according to the National Association of Insurance Commissioners. That translates to roughly $158 for the average auto insurance cost per month.

We at Direct Insurance Services know these numbers can feel overwhelming when you’re shopping for coverage. The reality is that your actual premium depends on dozens of factors, from your zip code to your credit score.

Understanding what drives these costs helps you make smarter decisions about your coverage and budget.

How Much Does Coverage Type Really Cost

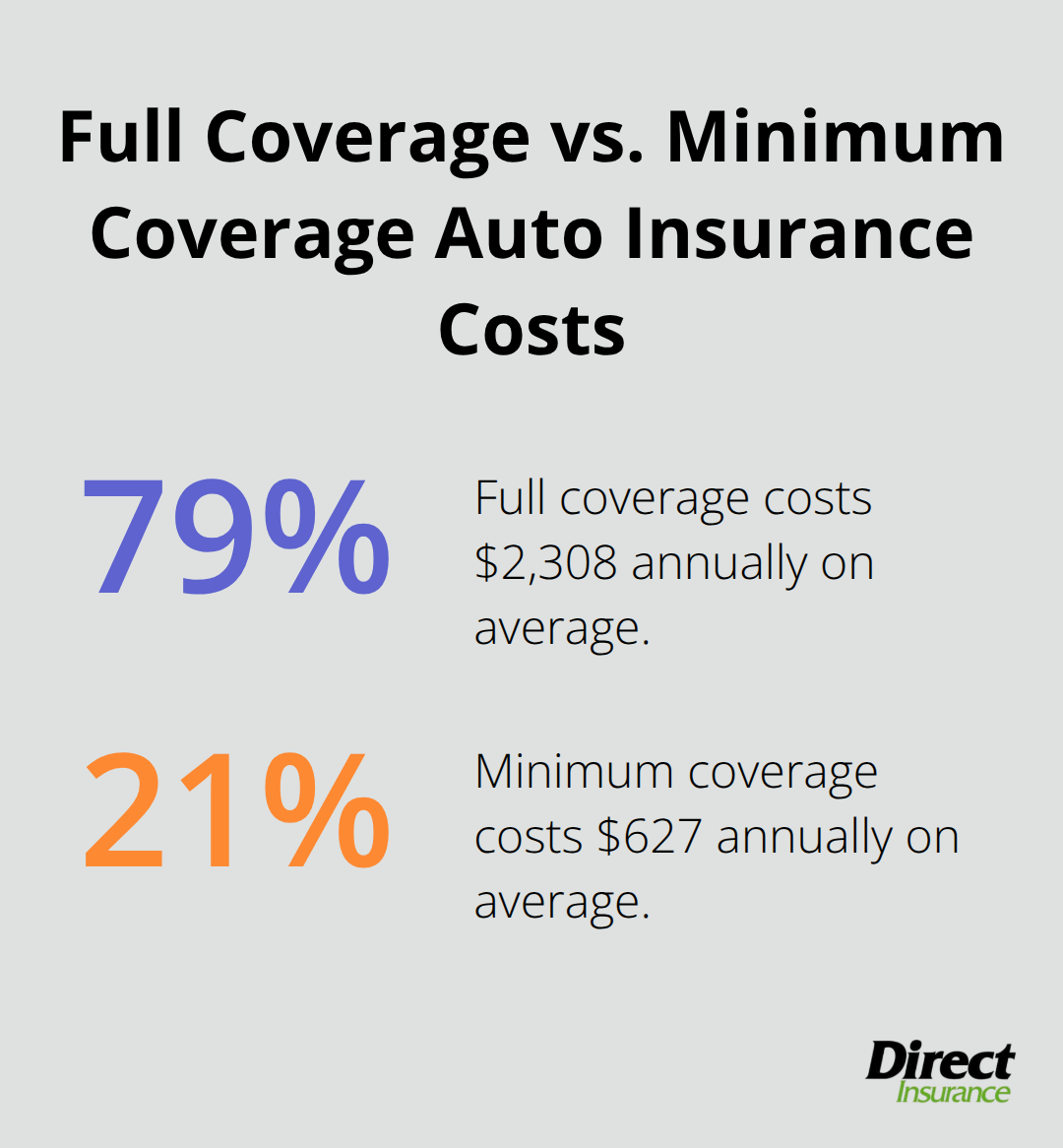

Full coverage auto insurance averages $2,308 annually nationwide, while minimum coverage costs just $627 per year according to NerdWallet data. You pay $192 monthly for comprehensive protection versus $52 for bare-bones coverage. The price difference reflects what you receive: full coverage includes collision and comprehensive protection that minimum coverage lacks entirely.

State Differences Change Everything

Your location determines your premium more than any other factor. Louisiana drivers face the highest costs at $4,299 yearly for full coverage, while Wyoming residents pay only $1,108. Florida ranks second highest at $4,011 annually, and New Jersey third at $3,387. New Hampshire drivers pay $1,474 and Vermont residents $1,480 for the same coverage (representing the most affordable options). These gaps exist because states have different fraud rates, weather patterns, and legal requirements that directly impact claim costs.

Payment Frequency Affects Your Wallet

Monthly payments cost more than annual premiums due to processing fees and interest charges. Insurance companies prefer annual payments because they receive cash upfront and avoid collection risks. Most carriers add $3 to $10 monthly for installment fees (which adds $36 to $120 yearly to your total cost). The math favors annual payments if your budget allows it, saving you roughly 5% compared to monthly arrangements.

Age Groups Face Different Rate Structures

Young drivers aged 20 pay an average of $4,686 for full coverage insurance, reflecting the higher risks associated with less experience. Drivers with clean records and good credit pay an average of $2,308, while those with a DUI face costs of $4,274. Poor credit generally results in higher premiums, with average full coverage costs reaching $3,852 yearly compared to $2,308 for those with good credit.

These cost variations show how personal factors stack up to create your final premium, which leads us to examine the specific elements that insurance companies evaluate when they calculate your rates.

What Drives Your Premium Up or Down

Insurance companies evaluate specific risk factors when they calculate your premium, and these elements give you power to influence your costs. Your age creates the biggest rate swing, with significant differences between younger and older drivers. The Insurance Information Institute reports that male drivers face 63% higher fatal accident rates than females, which explains premium differences. However, 18-year-old males cost 8 percent less to insure than their female counterparts, and as drivers age, the difference in premium between genders narrows. Experience matters more than age alone – rates drop at 25 when drivers typically show five years of history without major incidents.

Vehicle Choice Creates Immediate Cost Impact

Your car determines risk levels that insurance companies price accordingly. High-performance vehicles and frequently stolen models trigger higher premiums because they create more expensive claims. Anti-theft features reduce rates when they lower theft risk, while safety features and strong crash-test ratings qualify for discounts. The Insurance Information Institute notes that where you park matters too – garage spaces cost less than street spots because they reduce theft and vandalism exposure.

Credit and Records Shape Long-Term Costs

Poor credit increases full coverage costs to $3,852 yearly versus $2,308 for good credit according to NerdWallet research. Young drivers with poor credit face brutal combinations, with costs around $7,623 annually (according to the Consumer Financial Protection Bureau). Traffic violations create permanent premium increases: TheZebra.com shows at-fault accidents raise rates by 42% and stay on your record for three years.

A single ticket pushes average rates from $2,308 to $2,933, while at-fault crashes increase costs to $3,415. DUI convictions create the steepest penalties, with average costs that jump to $4,274 annually.

These rate factors stack up quickly, but smart shoppers know how to work the system in their favor through strategic choices and active comparison tactics.

How to Cut Your Insurance Costs

Multiple carrier comparison delivers the most effective premium reduction strategy. Rate differences between insurers can be substantial – different companies may charge significantly different amounts for identical protection. Company choice creates meaningful savings opportunities. Annual comparison or comparison after major life events like marriage, home purchases, or job changes typically uncovers potential savings according to industry research.

Smart Discount Combinations Reduce Monthly Bills

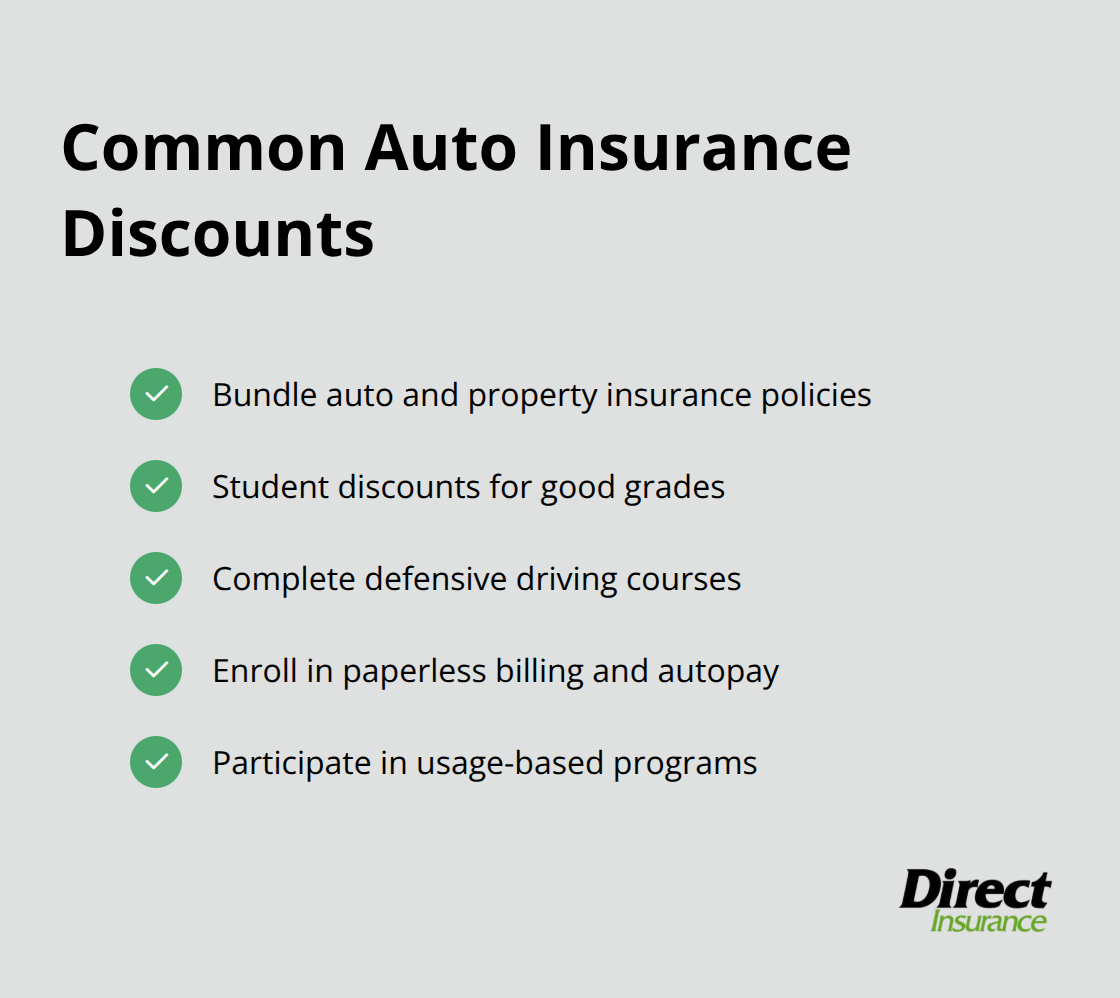

Major carriers offer substantial discounts for auto and property insurance bundles, often providing savings on combined premiums. Student discounts are available for high school and college students with good grades. Defensive driving courses qualify for additional reductions, while paperless billing and autopay setups cut costs through eliminated processing fees. Usage-based programs reward safe drivers with potential discounts for drivers who avoid hard braking and late-night trips.

Anti-theft devices reduce premiums when they lower theft risk, and garage parking beats street spots for rate calculations.

Strategic Coverage Adjustments Create Immediate Relief

Higher deductibles from $500 to $1,000 typically reduce monthly premiums, though you accept higher out-of-pocket costs during claims. Dropped comprehensive and collision coverage on vehicles worth less than a certain threshold eliminates expensive protection that may exceed potential payouts. However, liability limits above state minimums protect your assets better than bare-bones coverage. Young drivers with poor credit face higher costs annually, which makes these adjustments particularly valuable for budget-conscious households.

Final Thoughts

Auto insurance costs average $158 monthly nationwide, but your actual premium depends on your specific situation. Full coverage runs $192 per month while minimum coverage costs $52. Young drivers pay significantly more, with 20-year-olds who face $390 monthly premiums.

Smart shoppers reduce costs through annual comparison tactics, discount combinations, and strategic coverage adjustments. Bundling policies, clean records, and higher deductibles cut monthly expenses. The average auto insurance cost per month drops when you actively manage these factors.

Review your policy annually or after major life changes like marriage, home purchases, or job transitions (rate changes happen frequently, and your circumstances evolve). We at Direct Insurance Services work with multiple carriers to help Utah residents find personalized coverage solutions that fit their budgets and protection needs. Independent agencies provide access to competitive rates without single-company limitations.