Small Business Contractor Insurance Demystified: What Utah Contractors Need to Know

Running a contracting business in Utah means managing real risks-from job site injuries to equipment damage. Small business contractor insurance protects you from financial losses that could shut down your operation.

At Direct Insurance Services, we’ve helped countless Utah contractors find coverage that actually fits their needs. This guide breaks down what you need to know to make the right choice.

What Contractor Insurance Actually Covers

The Core Protections Your Business Needs

Contractor insurance isn’t one policy-it’s a collection of protections designed to cover the specific threats your business faces. General liability insurance protects you when someone gets hurt on your job site or you damage a client’s property, with Utah law requiring a minimum of $100,000 per incident for licensed contractors. Workers’ compensation insurance becomes mandatory the moment you hire your first employee, covering medical costs and lost wages if someone gets injured while working for you. Commercial auto insurance covers vehicles used for business purposes, which your personal auto policy explicitly excludes. Beyond these core three, many Utah contractors also carry builder’s risk insurance for materials and structures under construction, tools and equipment coverage for theft or damage, and professional liability for design or engineering errors.

How Your Trade and Location Shape Coverage Needs

The specific combination of coverage depends entirely on your trade, project type, and client requirements. A residential remodeler in Salt Lake City faces different exposures than a solar installer in St. George, so your coverage should reflect that reality. Utah’s construction industry is booming, but that growth comes with elevated risk. The Bureau of Labor Statistics reported 31,700 non-fatal workplace injuries across Utah in 2022, with 87 percent occurring in the private sector, making injury protection a financial necessity rather than an option.

Premium Costs and Risk Factors

Higher-risk trades like roofing and electrical work command significantly higher insurance premiums than lower-risk work like painting or finishing. Your location within Utah matters too-insurance costs differ between Salt Lake City and St. George based on local risk exposure, theft rates, and weather patterns. If you operate as a sole proprietor with no employees, you might think you can skip workers’ compensation coverage, but that exemption doesn’t eliminate your need for general liability insurance, which remains essential to meet licensing requirements and satisfy client contracts.

Coverage Limits That Protect Your Bottom Line

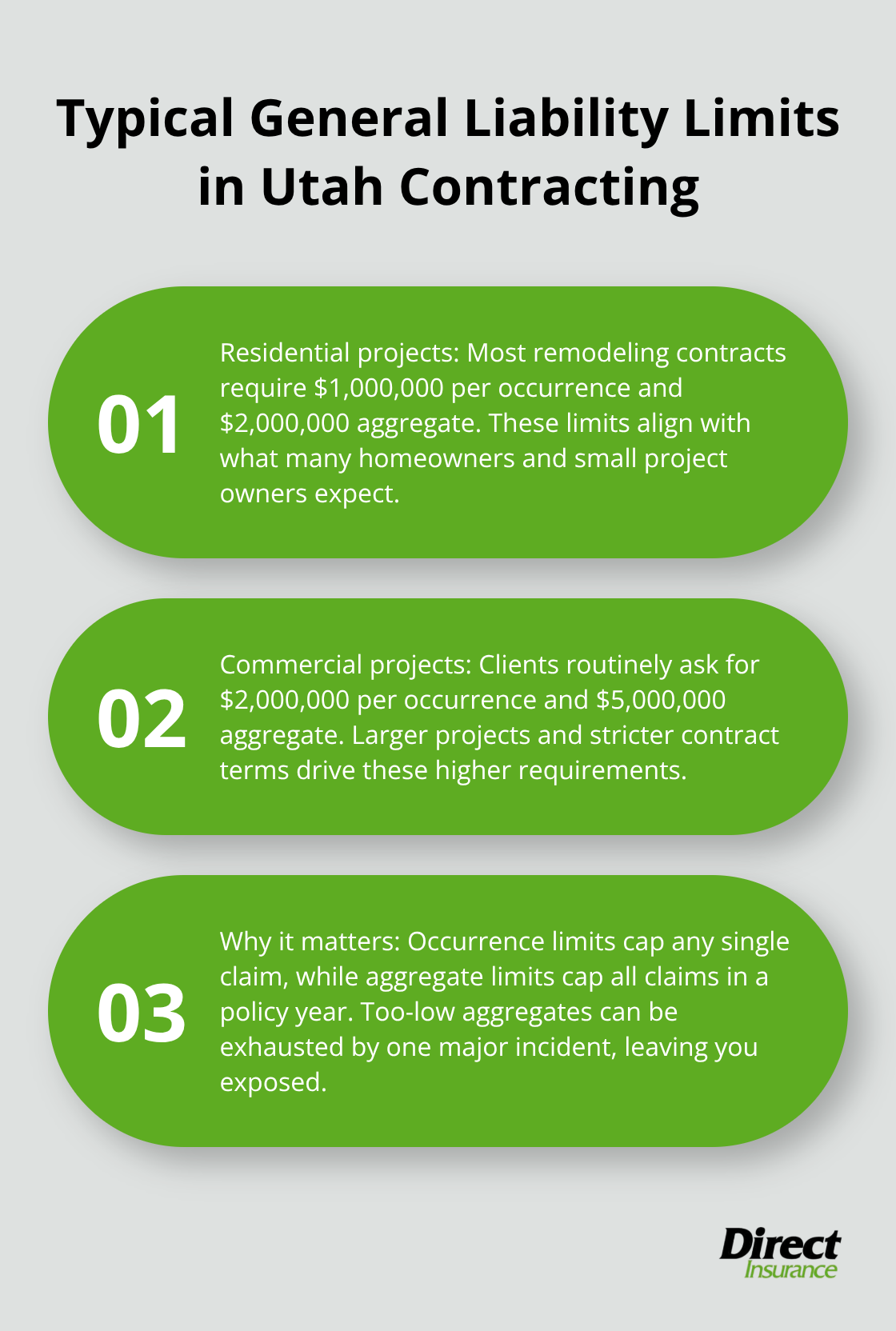

Most contractors should try general liability at $1,000,000 per occurrence and $2,000,000 aggregate for residential work, while commercial projects typically demand $2,000,000 per occurrence and $5,000,000 aggregate. Project owners and general contractors will require you to provide a certificate of insurance naming them as additional insureds before you step on site, making coverage verification a standard business requirement rather than a paperwork burden. This requirement applies across Utah’s construction landscape and reflects how seriously clients take risk management on their projects.

Types of Contractor Insurance Coverage Explained

General Liability: Your First Line of Defense

General liability insurance forms the non-negotiable foundation of contractor protection in Utah. This coverage pays for medical bills, legal defense, and settlements when someone gets injured on your job site or you damage a client’s property. Utah’s Division of Professional Licensing requires a minimum of $1,000,000 per incident for licensed contractors, but that baseline often falls short of what project owners actually demand. Most residential remodeling contracts require $1,000,000 per occurrence and $2,000,000 aggregate, while commercial clients routinely ask for $2,000,000 per occurrence and $5,000,000 aggregate. The distinction matters because aggregate limits cap your total protection across all claims in a year, so a single major incident on a commercial job can exhaust inadequate limits before the year ends.

Coverage includes third-party bodily injury, property damage, and personal advertising injury, with occurrence-based policies protecting you from claims filed years after work is completed. Your policy must name project owners and general contractors as additional insureds before you show up on site, a requirement that applies across Utah’s construction landscape regardless of project size.

Workers’ Compensation: Protecting Your Team

Workers’ compensation insurance shifts from optional to mandatory the instant you hire your first employee, covering medical expenses and lost wages for job site injuries. Utah law requires this coverage if you have employees, and a lapse in coverage triggers disciplinary action from the Division of Professional Licensing, including possible license suspension. If you operate solo with no employees, you can apply for a Workers’ Compensation Coverage Waiver through the Utah Labor Commission for a $50 processing fee, but this exemption only eliminates workers’ comp requirements-general liability remains legally required.

Commercial Auto: Don’t Overlook This Gap

Commercial auto insurance protects vehicles used for business purposes, which your personal auto policy explicitly excludes from coverage, making this coverage mandatory for any vehicle used on jobs or client visits. Many Utah contractors overlook this gap until they face a denied claim after a business-related accident, discovering too late that personal policies contain business-use exclusions.

Builder’s Risk and Equipment Protection

Builder’s risk insurance covers materials and structures under construction from fire, theft, vandalism, or weather damage, protecting your investment in materials and work-in-progress. Tools and equipment coverage protects your trade-specific assets from damage, theft, or loss on-site or in transit, with coverage limits tied directly to your equipment inventory value.

Professional Liability for Design and Engineering Work

Professional liability insurance becomes important for contractors who offer design or engineering services, covering claims of professional negligence and associated defense costs that general liability doesn’t touch. Understanding which coverage types apply to your specific trade and project scope determines whether you have adequate protection or dangerous gaps. The next section walks you through how to assess your actual business needs and match them to the right combination of policies.

How to Choose the Right Contractor Insurance Plan

Assess Your Actual Business Profile

Selecting contractor insurance means stepping past generic quotes and matching protection to what your operation actually does. List every vehicle, tool, and service your business touches. A plumbing contractor who handles both residential repairs and commercial installations faces different exposures than a painter who works solo on residential jobs, so your coverage must reflect those specifics. Document your annual payroll, number of employees, typical project values, and whether clients demand specific coverage limits before requesting quotes. This groundwork prevents you from overpaying for coverage you don’t need or discovering mid-project that you lack critical protection. Many Utah contractors skip this step and end up with either gaps that cost them thousands or premiums 30 to 40 percent higher than necessary because they didn’t clearly communicate their actual business profile to insurers.

Compare Quotes Across Multiple Carriers

Once you understand your business profile, request quotes from multiple carriers rather than accepting the first offer. Market position doesn’t automatically translate to the best rates for your specific trade and location. Bundling multiple coverages typically saves approximately 20 percent on combined premiums compared to purchasing policies separately, and many carriers offer same-day certificates of insurance so you can secure permits or start jobs immediately. Higher-risk trades like roofing naturally cost more than lower-risk work, but within your trade category, factors like your claims history, crew size, and equipment inventory drive the actual premium. A contractor with zero claims over five years might qualify for rates 20 to 30 percent lower than someone with recent incidents. Ask insurers directly about discounts for safety certifications, completed safety training, or established business longevity, as these reduce their perceived risk and your costs. Start coverage with as little as 20 percent down rather than paying full annual premiums upfront, which improves cash flow for growing operations.

Work with an Independent Agent to Customize Coverage

An independent agent represents multiple carriers and can match your specific trade, location, and project profile to insurers who specialize in contractors like you. Direct Insurance Services operates as an independent agency throughout Utah, which means we work with top-rated carriers to find options tailored to your actual needs rather than pushing a single company’s standard package. An independent agent reviews whether your current limits align with what clients actually demand on your typical projects, ensures your certificate of insurance names the right parties before you show up on site, and adjusts coverage as your business grows or shifts into new service areas. This relationship prevents the common mistake of contractors who carry the same policy for five years without updates, only to discover their limits fall short when they land a larger commercial project. Schedule annual reviews with your agent to evaluate whether equipment additions, new service lines, or payroll growth warrant coverage adjustments, since your policy should evolve with your business rather than remaining static while your exposures change.

Final Thoughts

Contractor insurance in Utah protects your operation from the financial devastation that a single injury, property damage claim, or equipment loss can trigger. General liability, workers’ compensation, and commercial auto coverage form the non-negotiable core of small business contractor insurance, with additional protections layered in based on your specific trade and project profile. Document your business profile-your vehicles, equipment, employees, typical project values, and client requirements-then request quotes from multiple carriers to see where your actual costs land.

Many Utah contractors discover that bundling coverages saves them 20 percent or more compared to purchasing policies separately, and same-day certificates mean you can secure permits and start jobs without delays. Your claims history, crew size, location within Utah, and safety certifications all influence what you’ll actually pay, and these factors vary dramatically between insurers. Don’t accept the first quote or assume that the largest national carrier offers the best rates for your trade.

An independent agency makes the real difference by matching your small business contractor insurance needs to insurers who specialize in contractors like you, rather than pushing a generic package. We review whether your current limits align with what clients demand, verify that your certificate of insurance names the right parties before you show up on site, and adjust your coverage as your business grows. Get a quote today and take control of your contractor insurance.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation