How to Get Flood Coverage for Your Home Insurance

Floods cause more damage to U.S. homes than any other natural disaster, yet most homeowners don’t realize their standard insurance won’t cover it. We at Direct Insurance Services know that Utah residents face real flood risks, and understanding your options for flood coverage home insurance is the first step toward protecting your property.

This guide walks you through everything you need to know about securing the right protection.

Why Your Homeowners Policy Won’t Protect You from Floods

Standard Policies Exclude Flood Damage

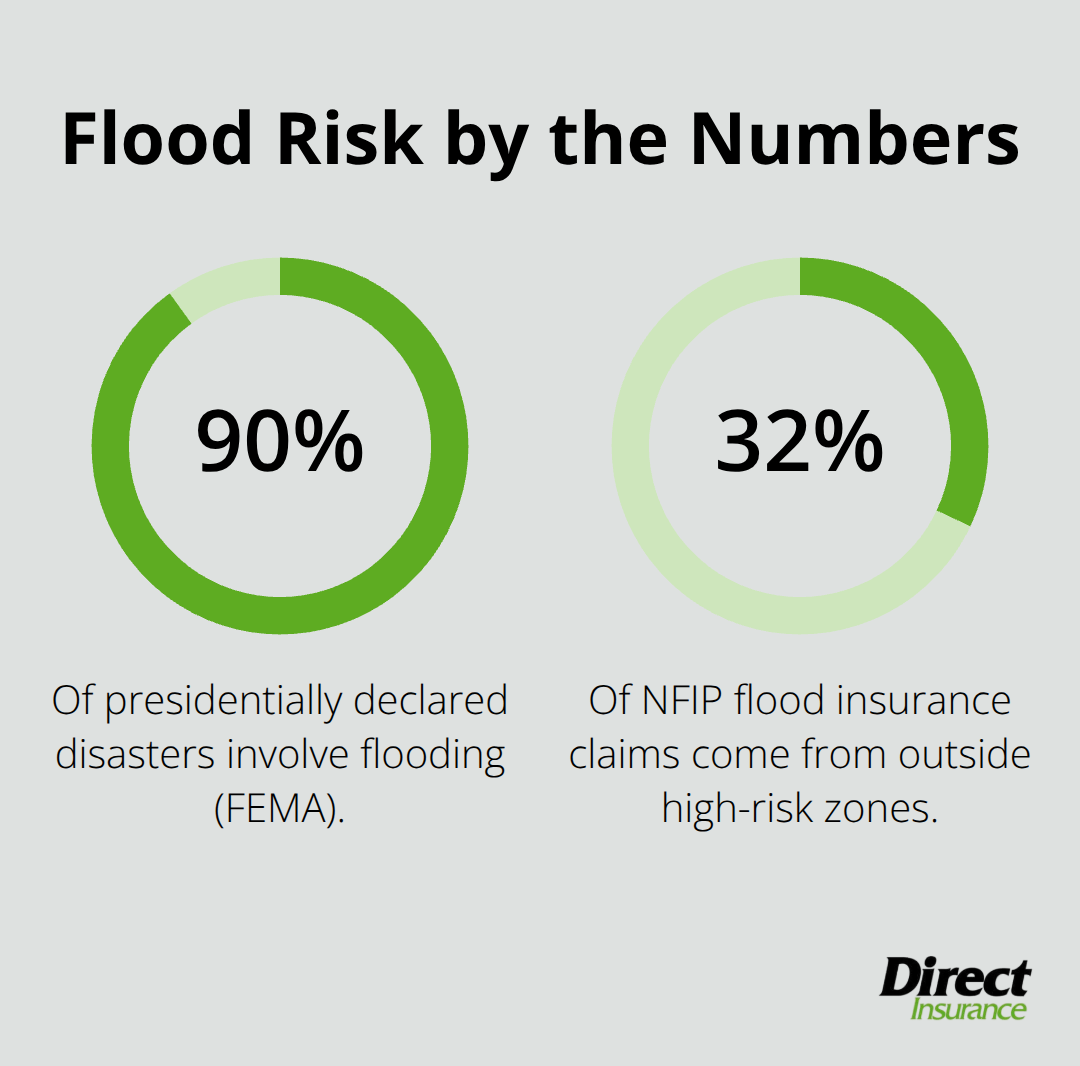

Standard homeowners insurance policies contain explicit exclusions for flood damage, which means your typical coverage won’t pay a single dollar when water from heavy rainfall, overflowing rivers, or storm surge damages your home. Insurance companies treat floods separately because the risk is too widespread and unpredictable for traditional homeowners policies to absorb. According to FEMA, 90% of presidentially declared disasters involve flooding, yet most homeowners remain uninsured for this specific peril. The gap exists because flood risk varies dramatically by location and requires specialized underwriting that standard policies don’t provide. Your homeowners insurance will cover wind damage from a hurricane, but not the flooding that follows the same storm.

Why This Matters in Utah

This distinction matters enormously in Utah, where flash flooding in canyons and along rivers has caused significant property damage in recent years. To get flood protection, you need a separate flood insurance policy, either through the National Flood Insurance Program administered by FEMA or through private flood insurance carriers.

Assess Your Actual Flood Exposure

Utah homeowners in high-risk flood zones must understand their actual exposure before choosing coverage. Start by checking your property on the Flood Map Service Center to determine your flood zone and base flood elevation, which directly affects your insurance costs and requirements. If your mortgage comes from a government-backed lender and your home sits in a high-risk area, your lender will require you to purchase flood insurance before closing.

Flooding Occurs Outside High-Risk Zones Too

Even if you’re not in a designated high-risk zone, flooding can still occur. The true cost of flood damage extends beyond structural repairs; it includes displacement from your home, lost personal belongings, and recovery expenses that standard insurance won’t cover. A single inch of water can cause thousands in damage, while several feet can total your home.

Take Action Before Flood Season

Every Utah homeowner should assess their flood risk and secure appropriate coverage, whether through the NFIP or private options, because waiting until flood season arrives leaves you exposed and uninsured. Understanding which flood insurance option fits your situation requires comparing what the NFIP offers against private flood insurance alternatives-a comparison we’ll explore in the next section.

NFIP vs. Private Flood Insurance

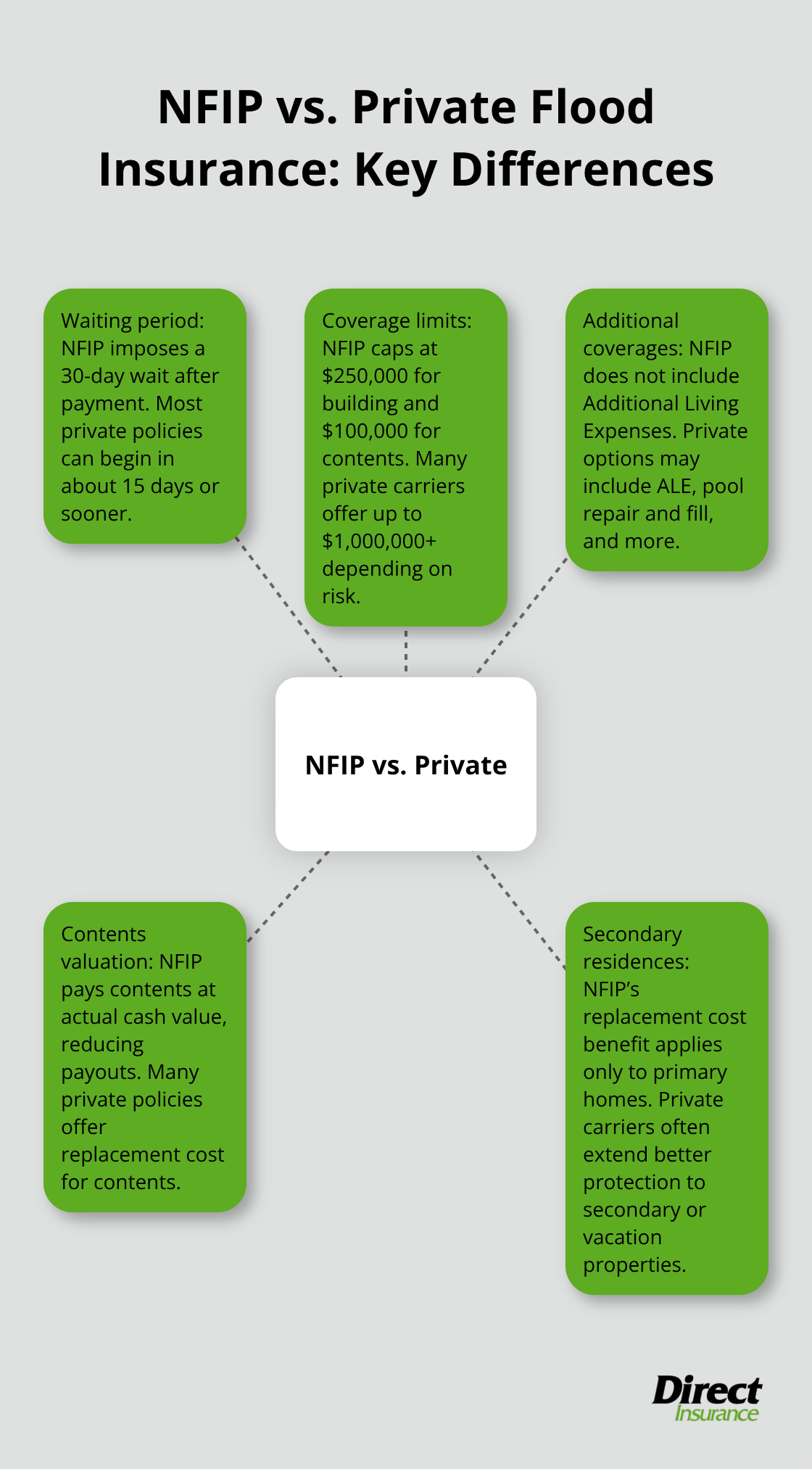

The National Flood Insurance Program, administered by FEMA, has served as the primary flood insurance option since 1968, but it no longer stands as your only choice. About 47 private insurance carriers now sell flood policies through the Write Your Own program, where these companies handle sales and service while FEMA underwrites the risk. This competition matters because it gives Utah homeowners real options with different coverage limits, waiting periods, and pricing structures. The NFIP covers approximately 4.7 million policyholders nationwide with nearly $1.3 trillion in coverage, making it the nation’s largest single-line insurance program. However, the NFIP has strict limits: building coverage maxes out at $250,000 for homeowners and contents coverage at $100,000. If your home’s replacement cost exceeds these limits-which happens frequently in Utah’s competitive real estate market-you’ll need either private flood insurance or an excess policy to close the gap. Private carriers commonly offer building coverage up to $1,000,000 or more, depending on your property’s risk level and the carrier’s appetite.

Coverage Flexibility and Timing Differences

The practical difference between NFIP and private options comes down to coverage flexibility and timing. NFIP policies impose a mandatory 30-day waiting period from payment before coverage begins, with exceptions only for mortgage closings or when flood maps change. Private flood policies typically start coverage within 15 days or sooner, which matters if you purchase coverage as flood season approaches. Private carriers also offer coverages the NFIP doesn’t provide, including Additional Living Expenses if displacement from your home occurs, pool repair and fill coverage, and replacement cost protection for contents and secondary residences.

How Claims Payments Differ

The NFIP pays contents claims at actual cash value rather than replacement cost, meaning you’ll recover less than what it costs to replace your belongings today. For secondary residences or rental properties, private flood insurance provides significantly better protection because the NFIP’s replacement cost benefit applies only to primary residences. This distinction matters substantially if you own investment properties or vacation homes in Utah.

Pricing and Risk Assessment

Pricing varies based on your home’s elevation, proximity to water, flood risk zone, and chosen limits, but private carriers’ advanced computer modeling and AI-driven risk assessment often produce more competitive rates than NFIP’s standardized approach. As private flood insurers gain experience with property-specific data, their rates may decrease over time thanks to more accurate risk evaluations. This means shopping around could save you hundreds annually compared to accepting NFIP’s fixed pricing structure.

How to Compare Your Options

When you shop for coverage, compare quotes from both the NFIP and at least two private carriers to see which option delivers the coverage limits and features your Utah home actually needs. Direct Insurance Services, as a locally trusted independent agency, works with top-rated carriers to help you access the best coverage options without pressure for a one-size-fits-all approach. Understanding which flood insurance option fits your situation requires knowing your specific property details and flood risk-information you’ll gather in the next section.

Getting Your Flood Coverage in Place

Identify Your Flood Zone and Risk Level

Start with the Flood Map Service Center to identify your exact flood zone and base flood elevation. Enter your Utah address and you’ll see whether you’re in a high-risk area designated as Special Flood Hazard Area, moderate-to-low risk, or unshaded risk zone. This single step determines everything that follows: your insurance requirements, your premium costs, and which coverage options make sense for your situation. If your lender is government-backed and your home sits in a high-risk zone, flood insurance isn’t optional-it’s a loan requirement. Even if you’re in a lower-risk area, knowing your base flood elevation helps you understand whether your property sits above or below the expected water level during a 100-year flood event.

Gather Your Property Documentation

Collect your property deed, mortgage documents, and home inspection reports before contacting insurers. These documents show your home’s age, construction type, square footage, and replacement cost-all factors that directly affect your premium and available coverage limits. If you’ve made recent renovations or upgrades, have that documentation ready because updated construction details can lower your rates. An elevation certificate proves your home’s elevation relative to the base flood elevation and can reduce your premium significantly. If your home has been elevated or you’ve made flood-resistant improvements like moving electrical panels above flood level, get those documented.

Request Quotes from Multiple Carriers

Contact at least two private flood insurance carriers and request a quote from the NFIP to compare your options. The NFIP Quote Tool takes just a few minutes to complete online and gives you a baseline rate. Private carriers like Progressive offer quotes by phone (1-866-749-7436), and each carrier’s pricing reflects their specific risk assessment models.

Request quotes with identical coverage limits so you can compare apples to apples-try building coverage at $250,000, $350,000, and $500,000 to see how limits affect your premium. Note the waiting period each carrier imposes: the NFIP’s mandatory 30 days versus private carriers’ typical 15 days or less. If you’re approaching flood season, faster coverage activation matters.

Compare Coverage Details and Discounts

Ask each carrier about available discounts for mitigation measures you’ve already completed, such as elevating utilities or obtaining an elevation certificate. This information becomes essential when you request quotes because insurers use it to calculate your premium. Private carriers’ advanced computer modeling and AI-driven risk assessment often produce more competitive rates than NFIP’s standardized approach. As private flood insurers gain experience with property-specific data, their rates may decrease over time thanks to more accurate risk evaluations. This means shopping around could save you hundreds annually compared to accepting NFIP’s fixed pricing structure.

Make Your Selection and Purchase Coverage

Once you’ve compared quotes from multiple carriers, select the coverage that protects your Utah home rather than what a single carrier pushes. Verify that your chosen policy includes the coverage limits and endorsements (such as Additional Living Expenses or replacement cost for contents) that match your actual needs. Private flood policies typically start coverage within 15 days or sooner, while the NFIP imposes a mandatory 30-day waiting period from payment before coverage begins. If you own investment properties or vacation homes in Utah, private flood insurance provides significantly better protection because the NFIP’s replacement cost benefit applies only to primary residences. Complete your application with your selected carrier and confirm your coverage effective date to ensure protection before flood season arrives.

Final Thoughts

Securing flood coverage for your home insurance shouldn’t wait until storm clouds gather on the horizon. Utah homeowners who delay until flood season arrives often find themselves unable to obtain coverage quickly enough, or worse, facing uninsured losses that devastate their finances. The reality is straightforward: standard homeowners policies won’t protect you, and 32% of NFIP flood insurance claims come from properties outside high-risk zones, meaning flood risk exists where many Utah residents don’t expect it.

Your action plan requires three concrete steps. Check your property on the Flood Map Service Center to understand your actual flood zone and base flood elevation, gather your property documentation including your deed and any elevation certificates, and request quotes from at least two private flood insurance carriers and the NFIP using identical coverage limits so you can compare pricing and coverage features directly. Pay attention to waiting periods, coverage limits, and available endorsements like Additional Living Expenses or replacement cost protection for contents, because these details determine whether your flood coverage home insurance actually protects your home and budget.

We at Direct Insurance Services understand Utah’s unique flood risks and work with top-rated carriers to help you access the best coverage options without pressure for a one-size-fits-all approach. Contact us to discuss your flood insurance needs and secure the protection your Utah home deserves before the next flood season arrives.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation